Part of our Risk Management guide

What Is The Fraud Triangle?

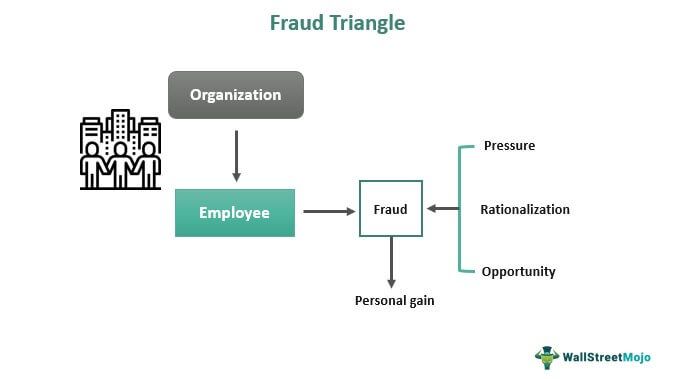

The fraud Triangle is the concept that explains why workers commit fraud at a workplace. It consists of three elements responsible for fraud – pressure, rationalization, and opportunity. It is an intentional deception that causes the personal gain of an employee or an entity.

According to this concept, fraud occurs when conditions for fraud are favorable to the fraud committer, and it is not random. It generates illegal gain or incentive or releases the individual or entity from unwanted pressure. This aggravates the temptation to take such a step and gives a feeling of better control without caring about the consequence.

Key Takeaways

- The fraud triangle notion identifies three factors—pressure, rationalization, and opportunity—as the root causes of employee workplace fraud.

- Most fraud perpetrators don’t view themselves as criminals; instead, they justify their actions. Similarly, management fraud justifies performance and shareholder demand for dividends.

- All personnel must receive appropriate ethical training that instills in them a belief that morality comes first in life. It is unethical to commit fraud or cheat in any circumstance, which helps shift fraudsters’ perspectives.

- To prevent and detect fraud, there must be surprise checks and audits; management audits are also advised, and strong fraud deterrence regulations so that no employee will even consider committing fraud.

Fraud Triangle Explained

The fraud triangle theory explains why and how individuals working in an organization commit fraud. It is the concept that explains the reason behind committing the fraud. The main elements are pressure, opportunity, and rationalization. In addition, there must be strong internal controls, zero tolerance, and a proper code of ethics to prevent fraud, which motivates employees to be ethical.

To prevent and detect fraud, there must be surprise checks and audits, management audits are also encouraged, and there must be strong fraud deterrence policies so that no employee can think of committing fraud.

Elements

Given below are the major elements of fraud triangle model.

#1 – Pressure

The pressure is the motivation behind fraud committing, and that can be either personal financial pressure or pressure from superiors. Both the pressures give the motivation and fraud triangle opportunity. If the pressure remains unsolved by rational & legal means, then individuals might go for irrational ways. Some common examples of personal financial pressure are non-shareable financial problems, revenue shortage, pressure from banks to pay loans, and lifestyle maintenance.

#2 – Opportunity

When pressure is present, the employee looks for an opportunity to commit fraud. For example, if there is no internal control over the inventory room, then the employee finds the chance to pilferage it and sell it in the market. It can be done by abusing the position, for example, pressure by superior to subordinate to show accounts by window dressing.

#3 – Rationalization

It is the last stage in the fraud triangle theory. This stage requires fraudsters to justify fraud acceptably. Most fraud committers do not see themselves as criminals; instead, they explain the situation of committing fraud. Similarly, fraud by management gives reason for performance and pressure from shareholders for dividends and all.

Example

Let us take the example of a situation where there are pressure from superiors or management of the entity for window dressing of accounts, teeming and lading, inventory pilferage and selling, sharing secret information with competitors to earn money, etc. When a person cannot see the apparent path of achieving personal or work goals by honest means, they may adopt dishonest alternatives.

There are also instances like lack of internal control in the accounts department, where an employee gets the chance to take away cash that are kept for office purpose. There should be regular checking, and a secured place to keep cash which should be maintained by a responsible person.

Challenges

The various challenges of the fraud triangle model are given below:

- Strong Internal Control – To Prevent organizations and management from committing fraud, there must be robust internal control and compliance with the law and high penalties for committing fraud to reduce it.

- Favorable Employee Policies – There must be favorable employee policies so that employees in need can get finance from the company instead of committing fraud.

- Strong Fraud Deterrence Policies – There must be strong fraud deterrence policies so that employees do not even think of committing fraud because of its substantial consequences.

- Ethical Training – There must be proper ethical training for all employees, which teaches them that ethics are most important in life. Doing fraud or cheating in any situation is unethical, which helps to change the mindset of fraudsters.

If students want to learn more about Auditing, they may consider taking courses offered by Coursera –

Which Is An Important Element?

The fraud triangle has three elements – Pressure, opportunity, and rationalization, and the most crucial factor is an opportunity. It is so because the opportunities available for committing the fraud motivate the fraudsters to commit the fraud. For example, suppose there are strong organizational controls, rigid policies, and proper and crystal-clear reporting policies. In that case, fraudsters might not get the opportunity to commit the fraud, so that no fraud can occur.

How To Identify?

- The motivation for committing fraud can vary from financial to non-financial. To prevent fraud, companies must implement strong internal controls and fraud triangle accounting. As an organization with strong internal control, experience lower frauds and quickly identify frauds.

- Strong Fraud deterrence policies also help prevent fraud as employees fear its consequences like losing their job and not getting a job anywhere.

- In audits, management audit and operational audits are motivated so that management fraud can be detected.

- In the case of the statutory audit, there is a clause where the auditor has to report whether fraud is committed by employees, management, or a third party.

How To Avoid?

The fraud triangle comprises three components: pressure, opportunity & rationalization. It helps in controlling the fraud triangle opportunity if there are:

- Zero Tolerance – Zero tolerance for errors and mistakes. Many employees pity themselves after committing the fraud, and organizations shouldn’t be kind and have zero tolerance for this.

- Surprise Visits and Audits – Top management must have a system of surprise checks and visits, and auditors should also do fraud triangle accounting and surprise audits to ensure that no frauds are committed by or on the company.

- Code of Ethics – Companies have a robust code of ethics to ensure that they send the right message to employees regarding fraud. And provide that code of ethics to be followed by one and all.

Frequently Asked Questions (FAQs)

What three categories of frauds exist?

Internal fraud, occupational fraud, or employee dishonesty are a few of the names it goes by. However, asset misappropriation, bribery and corruption, and financial statement fraud are the three main categories of fraud.

What traits does the fraud triangle have?

According to the Fraud Triangle theory, if all three elements—unshareable financial need, apparent opportunity, and rationalization—are present, a person will likely engage in fraudulent behavior.

What is the purpose of the fraud triangle in auditing?

The Fraud Triangle is a fantastic tool to use as a cue to make sure internal auditors evaluate anti-fraud internal controls properly and spot crucial measures that might be lacking.

Recommended Articles

This article has been a guide to what is Fraud Triangle. We explain its elements, with example, the most important element, the challenges & how to identify. You may learn more about financing from the following articles –