What is Window Dressing in Accounting?

Window Dressing in Accounting refers to the manipulation done by the company’s management intentionally in the financial statements to present a more favorable picture of the company in front of the users of the financial statement before the same is released to the public.

Window dressing in accounting means an effort made by the management to improve the appearance of a company’s financial statements before it is publicly released. It is a manipulation of financial statements to show more favorable results for the business. It is done to mislead the investors. Companies and mutual funds can use it.

- It is done when a company/business has many shareholders, and the management wants to project to the investors/ shareholders that the business is doing well and wants their financial information to look appealing to them.

- It is done as the company’s financial position is one of the critical parameters, and it plays a crucial role in bringing in new business opportunities, investors, and shareholders.

- Window dressing can mislead the investors and other stakeholders who do not have the proper operational knowledge of the business.

- In closely-held business, it is not done as the owners are aware of the company’s performance.

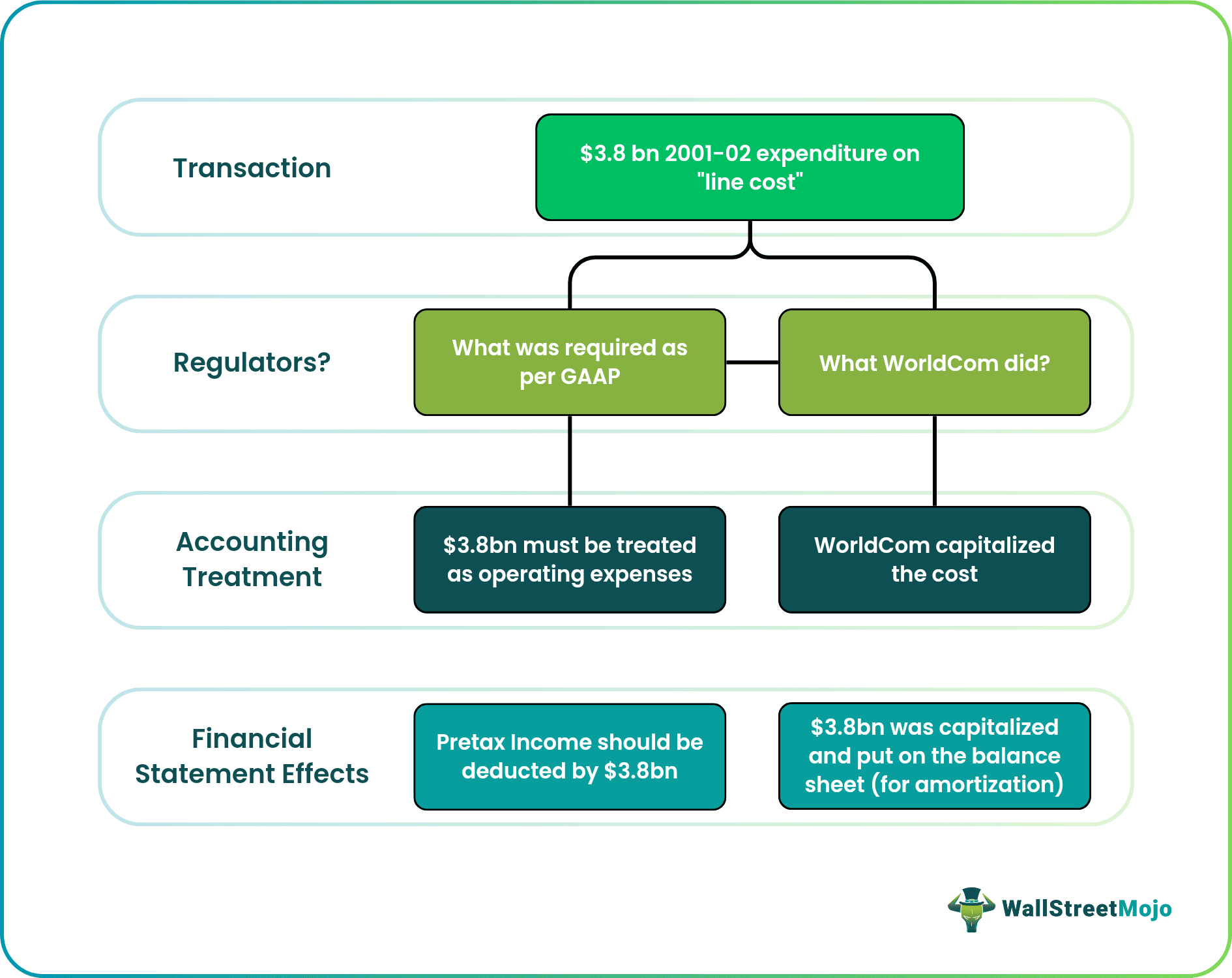

Example of Window Dressing (WorldCom)

The Worldcom case is one of the most infamous examples of window dressing, which was done by inflating earnings through improper capitalization of expenses. As a result, WorldCom declared bankruptcy in July 2002. Chief Accounting and finance executives charged with securities fraud.

Purpose of Window Dressing in Accounting

- Shareholders and Potential shareholders will be interested in investing in the company if the financial look is good.

- It is useful to seek funds from investors or to obtain any loan.

- The company’s stock price will shoot up if the financial performance is good.

- Tax avoidance can be done by showing poor financial results.

- To cover up the poor management decisions taken.

- It improves the liquidity position of the business;

- To show a stable profit and results for the company.

- It is done to reassure the company’s financial stability to money lenders.

- It is done to achieve targeted financial results.

- It is done to showcase a good return on investment.

- To increase the performance bonus to the management team based on the overstated profits

- To cover up the actual state of business if the business is nearing insolvency.

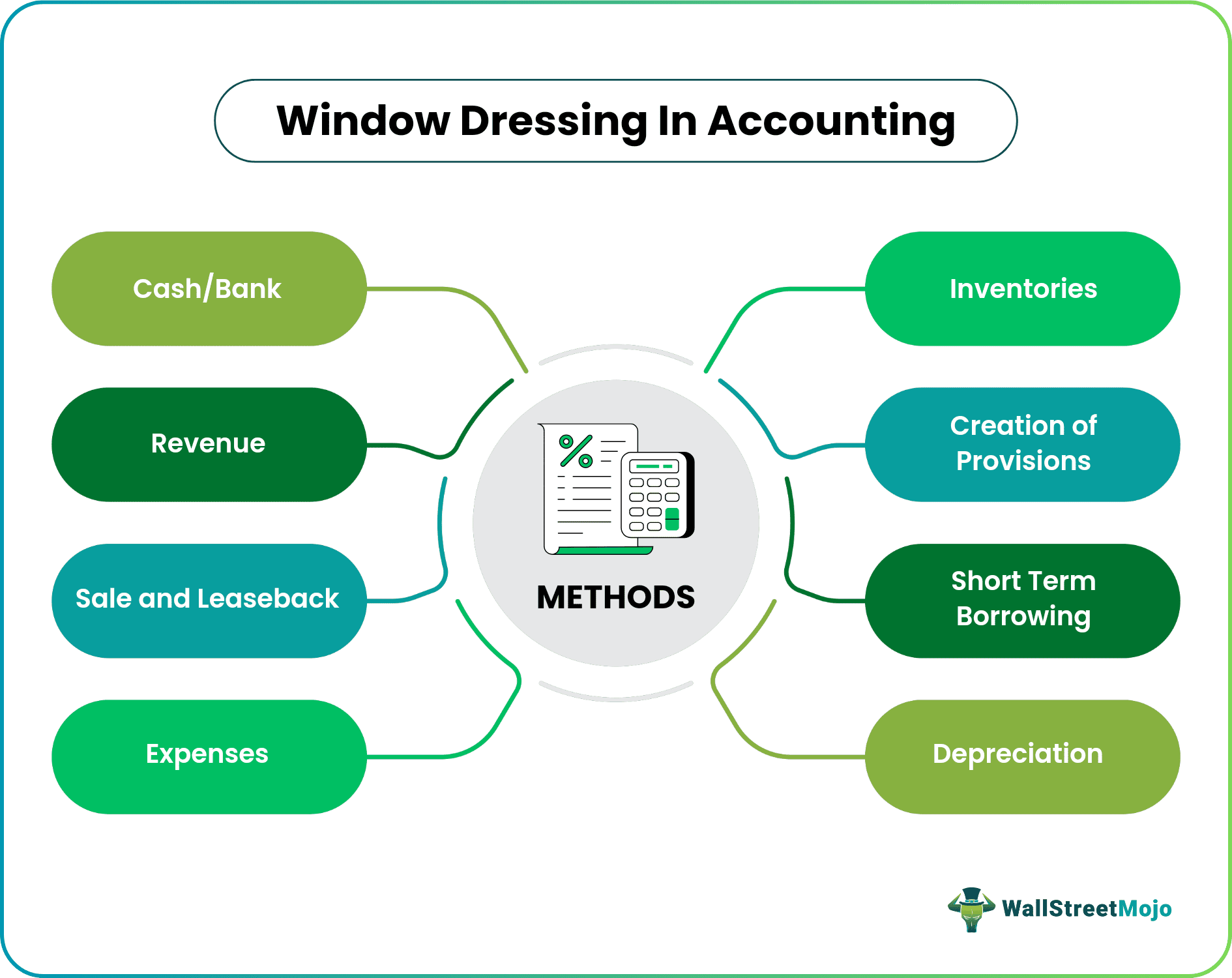

Top Methods of Window Dressing in Accounting

- Cash/Bank: Postponing the payment to suppliers so that the cash/bank balance will be high at the end of the reporting period. Selling off the old assets so that the cash balance will improve and show a better liquidity position. At the same time, the fixed assets balance will not differ much since it is an old asset with more accumulated depreciation.

- Inventories: Changing the valuation of inventories to increase or decrease profits.

- Revenue: Companies sell products at a discounted price or give special offers to boost the sales at the year-end so that the company’s financial performance looks better.

- Depreciation: Changing the depreciation method from accelerated depreciation to the straight-line depreciation method improves the profits.

- Creation of Provisions: As per the concept of prudence in accounting, it requires recording expenses and liabilities as soon as possible but revenue only when it is realized or assured. If an excess provision is created, it can reduce the profits and the corresponding tax payment.

- Short Term Borrowing: Short term borrowing is obtained to maintain the liquidity position of the organization

- Sale and Leaseback: Selling off the assets before the end of the financial year and using the money to fund the business and maintain the liquidity position, and leasing it back for a longer term for the business operations.

- Expenses: Presenting the capital expenditure as revenue expenditure to understate the profits;

The above mentioned are a few ideas for window dressing in accounting; there are many other ways where the financials can be manipulated and presented according to management needs.

Window dressing is predominantly done to boost the stock price and make potential investors interested in the business. This concept is unethical as it is misleading, and it is only a short-term advantage as it merely takes the benefit from the future period.

How to Identify Window Dressing in Accounting?

Window dressing in accounting can be spotted by properly analyzing and comparing the financial statements. In addition, financial parameters and other components should be appropriately reviewed to understand the state of the business.

The following can be looked into the company’s financials to identify window dressing.

- Improvement in cash balance because of short-term borrowings or cash flow from non-operating activities. The proper review should be done on the statement of cash flows to check which activity has resulted in cash inflow.

- Unusual increase or decrease in any of the account balances and the effect of the same in financials

- Change in accounting policy during the year like change in the inventory valuation, depreciation method, etc.

- Improvement in sales due to enormous discounts and an increase in trade payables

Conclusion

Window dressing in accounting is a short-term approach to make financial statements and portfolios look better and more appealing than they genuinely are. It is done to mislead investors from the real performance. It is an unethical practice as it involves deception, and it is done in the management’s interest.

Recommended Articles

This has been a Guide to Window Dressing in Accounting and its meaning. Here we discuss the top methods used in window dressing and examples and ways to identify them. You can learn more about financing from the following articles –