Part of our Accounting Concepts guide

Internal Control Meaning

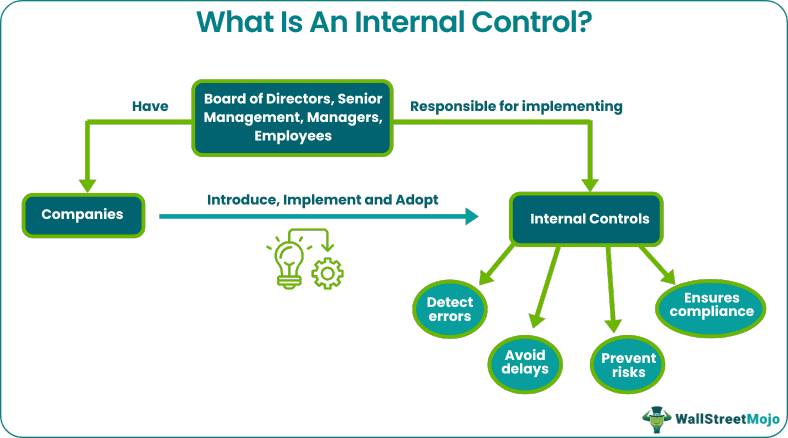

Internal control refers to the set of principles, procedures, and practices companies define to ensure they keep a check on risk-causing factors and rectify the same to avoid losses or frauds. It plays a significant role in guaranteeing accountability of companies, which remain under controlled supervision for correctness and reliability.

Conducting an internal control audit ensures evaluation of these controls, making sure firms are audit-compliant. In short, these controls keep a check on the loopholes that might lead to severe reputational damages to the market players in the long run.

- Internal control refers to the rules, policies, or procedures adopted to ensure the correctness of financial information and prevent financial and reputational damages.

- When proper controls are in place, they lead to the smooth and efficient working of an organization.

- The chances of non-compliances reduce when controls are effectively activated.

- Every company adopts a specific set of rules, policies, or procedures as controls, given the business’s nature, type, and purpose.

How Does Internal Control Work?

Internal control can be an effective measure that companies adopt to guarantee correctness in the information provided. When an organization publishes and presents its annual report, it is the summarized form of how it performs throughout a quarter or year. The data revealed becomes one of the most important factors in setting up corporate collaborations that potential investors and stakeholders seek interest in.

If the information provided is incorrect or misleading, the stakeholders feel cheated, which ultimately affects the organization’s reputation. Internal control locus includes principles, procedures, and policies that specify a set of manual labors or instructions to identify the loopholes and rectify them before it is used for decision making either by stakeholders or the companies themselves.

The objective of including and implementing controls is to ensure an organization’s:

- Efficiency of operations

- Compliance with audit rules, standards, laws, and regulations

- Accuracy and reliability of the financial reporting

From the board of directors to executives working in the companies, each individual is responsible for taking care of the appropriate implementation of these controls to ensure the information is timely provided and is reliable and accurate. They require guaranteeing that the data released comply with standard regulations, legal contracts, and applicable laws. In addition, the organizations must have stricter controls adopted to ensure accurate and reliable financial reporting, which forms the base for the annual reports that corporate players generate.

When the system of internal control adopted and implemented are strict and up to the mark, organizations remain prevented against errors, risks, frauds, irregularities, untimeliness, unreliability, and misleading information.

Types

Internal controls are segregated based on the purpose they are used for and the ways they are used in.

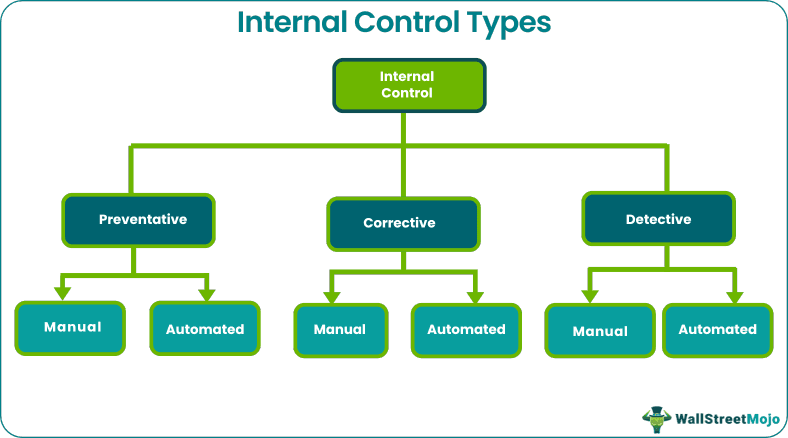

Internal controls can be preventative, detective, and corrective. As the name implies, preventative control is the procedure or measures used to prevent any suspected error or irregularity. Detective control, on the contrary, is the means adopted to identify the loopholes. In contrast, corrective controls are the ones that help rectify the detected shortcomings, which might lead to further financial or reputational issues for organizations.

It could be either manual or automated, no matter which type of control companies use to avoid errors, frauds, and risks. Manual controls are put into action by individuals who keep a check on the controlling measures and procedures. On the other hand, automated controls are the means of control inculcated within the machines and systems, taking care of various business processes.

As a result, the types and examples of these controls could be:

- Manual preventative control – hiring security guards, identification verification procedures, etc.

- Automated preventive control – having firewalls, system backup features, etc.

- Manual detective control – carrying out audits, inspections, etc.

- Automated detective control – reconciling information from one system to another, etc.

- Manual corrective control – disciplinary actions, refined policies, etc.

- Automated corrective control – installing software patches, maintaining password secrecy, etc.

Components of Internal Control

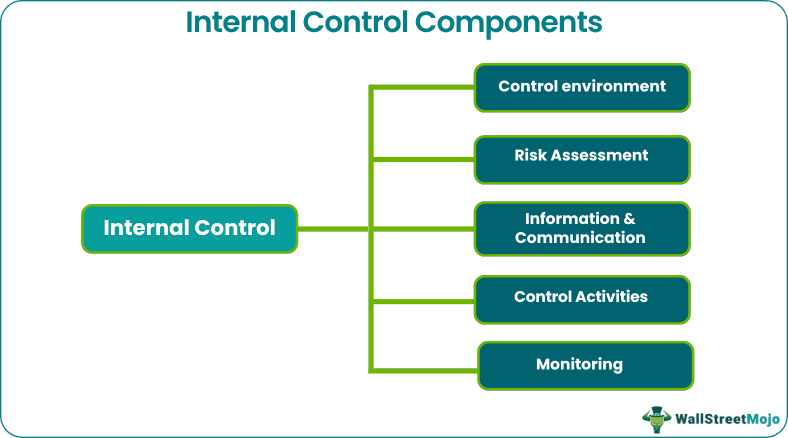

Multiple components comprise the framework. The first thing to ensure that the companies’ controls work perfectly is an appropriate control environment. This is what sets the conscious levels, making everyone from top management to staff members follow and keep a check on the policies, procedures, principles, and technology deployed. In addition, it sets the values, commitment, policies, responsibilities, operating style, participation, structure, and overall tone of the company.

The next component is risk assessment, which involves setting up controls that help organizations prevent possible or unexpected risks. As a result, these components look after the accuracy of recordkeeping to ensure the correctness of financial data and reporting. After that, there is a third component that includes fool-proof methods of collecting, assembling, processing, summarizing, and reporting financial data so that the data revealed do not mislead the decision-makers awaiting reports.

The next element is the control activities, which fall under the corrective form of control. If individuals or machines identify the risk at a prior stage, this fourth component allows controlling the procedures by taking necessary actions. Such steps include performance reviewing, setting up physical controls, delegating tasks, processing of information, etc.

Finally, monitoring all the procedures is the next on the list. This ensures obeying and transforming the policies and practices as and when necessary, according to the modifications that organizations undergo from time to time.

Examples

Let us consider the following examples to see how these controls work:

Example 1

The protection of the company’s cash is a must as it can be tampered and stolen with easily. Hence, applying controls becomes a necessity to protect the company’s cash. Therefore, a company can place different types of controls on the cash department.

To ensure protection, however, it can call for a system of segregation of duties in the cash department. In this, cash received from the customer can be recorded in the accounting system by different people. It means allotting different employees in the cash department for different activities so that the process is monitored by all of them simultaneously against any tampering.

Example 2

Recently, the Committee of Sponsoring Organizations of the Treadway Commission or COSO internal control framework has appeared to be the most widely used automated control system. The framework consists of all the five components and ensures everything from preventing an error/loophole to rectifying it effectively. Furthermore, it integrates the controls into the business activities and makes the procedure transparent and ethically sound.

Advantages & Disadvantages

Here is a list of benefits and limitations of these controls:

| Advantages | Disadvantages |

|---|---|

| Ensures proper accounting of transactions | Chances of human error in the implementation of the controls |

| Prevents financial and reputational issues | Delegation of tasks might be inappropriate, making one staff handle more than one task, affecting their performance |

| Sets the same tone for all from the organization’s top management to staff members | Maybe a costly affair |

| Keeps companies compliant with standard laws, rules, and regulations |

Internal Check vs Internal Control

Though internal check and internal control signify similar functions, their range of operation is what distinguishes them widely.

An internal check refers to the segregation and delegation of tasks to subordinates for the smooth running of a business. Internal control, on the other hand, is implemented to prevent, identify, or correct the loopholes, especially in the financial reports.

Internal checks only deal with the stage-wise functions of separate seniors who look after those activities and processes, while controls are checked and verified by everyone with equal responsibility. This is because the latter directly impacts the efficiency and productivity of the organizations.

For example, employee A may give a green signal to a product launch in the market as soon as the sample items are manufactured or produced. However, manager A could sense the defect in the material and ask the management to transform the process or raw material used for the production. While employee A signifies internal checks conducted by supervisors, manager A indicates implementing controls in the right way to ensure accountability for the loopholes and their rectification.

Frequently Asked Questions (FAQs)

What is internal control?

Internal control refers to the rules, policies, or procedures adopted to ensure the correctness of finance and accounting, protection of business assets, accountability, and preventing errors, risks, frauds, and other possible financial and reputational issues in the company.

Who is responsible for internal controls?

Every individual working in the organization is responsible for properly implementing these controls. Starting from the board of directors, vice-presidents, senior management, managers, and employees, they have to take the responsibility of accessing, adopting, implementing, reviewing, and transforming the controls as and when required.

Why are internal controls important?

Internal controls are important to ensure the companies work effectively and efficiently while complying with the standard rules, laws, and regulations. In addition, they have to provide the financial information being reported from time to time does not mislead investment decision-makers in any manner. In short, correctness, timeliness, and reliability are three factors that guarantee the efficiency of these controls.

Recommended Articles

This is a guide to what is internal control & its meaning. Here we explain its types, components, advantages, examples, limitations, vs internal check. You can learn more about accounting from the following articles –