What Is The Full Form of GST?

The full form of GST is Goods and Service Tax, which islevied on goods and services consumption. It is a destination-based tax, i.e., the tax paid where the goods or services are consumed. This tax combines and replaces other indirect taxes, including Value Added Tax (VAT), Central Saes Tax, etc.

It is levied at all stages of production, and taxes paid in the previous stage of the manufacturing cycle is available as credit which can be utilized to pay net GST liability. Thus, the final consumer bears the whole burden of a tax.

Key Takeaways

- GST(Goods and Service Tax) is a tax on consuming goods and services. GST is based on the user location and is charged at every production level.

- Earlier stage credits can be used for the final payment. Consumers are ultimately responsible for paying the total tax.

- India has a GST regime with three types of taxes: CGST, SGST, and IGST, collected by the Central and State governments.

- India has introduced GST to simplify tax laws, boost “Make in India,” and create more jobs, leading to a brighter future.

Full Form of GST Explained

The full form of GST refers to the tax that is levied on the consumption of good and services that reaches customers. This is what makes it known as the Goods and Services Tax. As soon as a consumer buys a product or service from a brand, they have to pay GST on it.

With an increase in global competition, India has been into introducing new ways to increase opportunities to become Global Power. The introduction of GST is one such step as it aims to implement unified single taxation in the form of GST. This tax has been fuelling the “Make in India” initiative of the Indian Government by encouraging producers to keep on adding value to the products and services while applying the required charges and ultimately helping increase the quality of life of the Indian citizens.

Entities with an annual turnover of over INR 20 lakhs are eligible to undergo GSt registration. The tax is calculated and levied at every stage of value addition and is paid by the receiver at the destination point. For example, the processing of the raw materials, the production of the finished product, the packaging of the product, and the shipment of the final item, each of them constitute the stages where value is added to the items.

Hence, when the customer receives the product, they have to pay the amount, inclusive of the monetary charges added and applied to the product at each stage of production. This is how GST works.

History

When all the foreign countries were generally moving into GST’s regime, i.e., One Nation-One tax, India first thought about it almost 16 years back when Mr. Atal Bihari Vajpayee was Prime Minister of India. On 28th February 2006, the proposed Budget for 2006-07 hinted at GST’s introduction from 1st April 2010. Preparing the draft Act was given to the Empowered Committee of State Finance Ministers (EC). This is the same committee that had formulated the design of State VAT. After that, many discussions were held between the committee, the Central Government, and various State Governments, and the first draft of the Act was released in November 2009.

Implementing GST required two major things: amending the Constitution (to make an entry for GST in it) and introducing the GST Act(s). The Constitutional amendment (the 122nd) was introduced in the 16th Lok Sabha in December 2014. Lok Sabha passed it in May 2015, and after that, it was sent to Rajya Sabha. Rajya Sabha passed it with certain amendments which required re-approval of Lok Sabha. On 8th September 2016, the President signed the Constitutional Amendment after the required number of states ratified it. On 16th September 2016, it was enacted as Constitution 101st Amendment Act 2016.

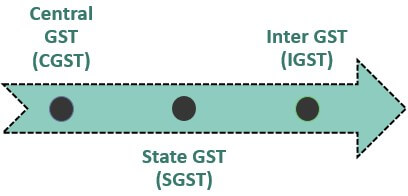

Types

In India, both Central and State governments have the power to levy taxes. Under the GST regime, too, both Center and State have the power to levy and collect GST. Therefore, GST in India is divided into three broad categories:

- Central GST (CGST): GST is levied by the Central Government during Intra State.

- State GST (SGST) / Union Territory GST (UGST): GST levied by State and Union Territory with the legislature, on Intra State.

- Inter GST (IGST): GST is levied by the Central Government on Inter-State supplies of goods and services so that credit of taxes paid in one state can be taken for GST liability in another.

(Remember, GST is a destination-based tax). Further, it applies to goods imported into India along with Applicable Custom Duty.

Reasons for Implementation

GST was implemented with the main aim of reducing the cascading effect. Earlier credit of taxes paid on goods was allowed only against the supply of goods and that too, with too many limitations. Further, the credit of one tax paid cannot be utilized to pay other taxes. Thus a need to have only one tax on goods and services so that credit and payment can be made easier and simpler arose. This was the primary reason for implementing GST. Thus, it has a combined Service tax, Central excise duty, additional excise duty, State VAT entertainment tax, etc.

Advantages

The Goods and Services Tax refrain from paying multiple taxes for products and services they buy, and pay only one tax. It, undoubtedly, has a lot of benefits, some of which have been listed below:

- Subsumed various Central and State taxes, thus making it “ONE NATION, ONE TAX.”

- The principle of origin-based taxes changed to consumption-based taxes. This benefited the States which use resources to consume goods and services. For this, the GST Act 2017 introduced POS (Place of Supply).

- GST law also provides a clear picture of the transaction to be treated as Either Supply of Goods or Services by clearly specifying the transaction list in Schedule II of the GST Act 2017. Most importantly, “Work Contract Services,” which was debatable from the beginning, is now totally clear that it is to be treated as Supply of Services only.

- GST came up with schemes for Small taxpayers, such as exemption from registration for those taxpayers whose total turnover during the previous FY is less than Rupees 40 Lakh (For Supplier of Goods only) / Rupees 20 lakh for other categories of Suppliers (As amended, However for special category states it is 10 Lakh). Composition scheme for Supplier of Goods (Turnover up to Rupees 1.5 Cr) and Supplier of Services (Turnover up to Rupees 50 Lakh).

- GST clarified the procedure for the E-Commerce operator, which was a pain point in VAT/ Service tax Law.

- Higher threshold limit as compared to erstwhile VAT/Service tax.

- All the GST processes, from registration to filing returns and paying taxes, are made online, which benefits start-ups and reduces infrastructure costs.

- Earlier, there was VAT and service tax, each of which had its compliances and returns. Under GST, there is just one return to be filed, which has reduced the number of returns.

- Simpler process for Export Refund (RFD-01).

Disadvantages

Though there are a myriad of advantages to paying GST, a few flaws are there that cannot be ignored as well.

- Being a new tax requires a lot of brainstorming for a business person. They have to identify its effect on their business. Further, the GSTIN council frequently changes the law through Notifications, which is difficult to monitor and follow.

- It increases the business’s operational cost since the business has to hire a GST professional.

- With the recent notification, the GSTIN council came up with E-Invoicing, which is actually a critical aspect for most Indian taxpayers (Small businessmen) due to a lack of Digital Literacy.

- The restriction of CAP of (2A ITC +20% EXTRA) on ITC to be taken in GSTR-3B as eligible ITC creates a hectic situation for the small taxpayer (less than Rupees 1.5 Cr turnover- Return Filing Quarterly) who get supplies majorly from small taxpayer only. So that means they have to pay Output taxes for two months in a quarter without ITC.

Frequently Asked Questions (FAQs)

What is the new GST limit?

According to GTRI, companies that make less than ₹1.5 crores in annual turnover makeup 84% of total registrations but only contribute less than 7% of the overall tax collected. The proposed new limit will reduce the number of taxpayers under the GST system from 1.4 crores to less than 23 lakhs. It will help ease the burden on the GST system.

Does insurance have GST?

In India, the Goods and Services Tax (GST) has replaced many indirect taxes on goods and services, including insurance. GST will be applied to the premium payment when purchasing an insurance product.

Should GST be charged on reimbursement of expenses?

When calculating the value of a supply, reimbursements will be included, but expenses claimed as pure agents will not be included. It means that any amount charged as a pure agent will be excluded from the taxable supply for GST purposes.

Recommended Articles

This has been a guide to what is the Full Form of GST. Here, we explain its history, types, reasons for implementation, advantages, and disadvantages. You may refer to the following articles to learn more about finance –

Recommended Articles

Continue with these closely related articles from the same guide.