Part of our Market Analysis guide

What is Implied Volatility?

Implied Volatility refers to the metric used to know the likelihood of changes in the prices of the given security as per the market’s point of view and as per the formula. Implied Volatility is calculated by putting the option’s market price in the Black-Scholes model. It is usually found more in a bullish market than in a bearish market.

An implied volatility chart shows uncertainty and emotions in the market in general. However, the movement in this chart is based purely on prices rather than fundamentals. Supply, demand, and time factors are the pivotal factors orchestrating the movements in this regard. It is usually expressed in percentage terms and standard deviation within a specific time frame.

Implied Volatility Explained

Implied volatility (IV) measures the likelihood of a change in the price of a security. It helps investors where their investment will move in the future by forecasting the supply & demand and the security price movement, which in turn helps to understand the price of options contracts. It is based on certain factors (which include the market expectation of the security’s price) that impact the price of a security and are usually expressed in percentage of the stock price, indicating a standard deviation that relates to a specific period. The symbol used to denote Implied Volatility is σ (sigma).

It relies on market consensus and depicts the outlook of the market. If market expectations increase or demand increases, implied volatility increases, increasing the options premium price component. Inversely, if the market expectations fall or demand for the security drops, implied volatility also decreases and decreases the options premium price component.

It is a measurement of the change in the price of security shortly. In a bearish market, it is high since investors assume that the security price will fall, whereas in a bullish market, it is low since investors assume the price will go up in the future. It plays a major role in deciding the pricing of options.

While calculating Implied Volatility, the determining factors are demand & supply, and time value.

Black – Scholes – Merton model formula can calculate the implied volatility using reverse calculations if all other values are available. It is measured based on the market’s consensus along with certain parameters and can turn out to be an incorrect prediction of the price movement.

Formula

The formula which acts as the basis of implied volatility calculator is discussed below. It shall help us under this concept and related factors in detail.

How To Calculate?

The method most often used by traders and fund managers is to find the market price of the particular option and incorporating it into the Black-Scholes formula.

After incorporating it, they back-solve the equation to find the volatility of the option. A few other options for determining the implied volatility chart include iterative search and trial and error method.

Indicators

The movements in the market are beyond the control of any player. However, the movements are always indicators of what is to follow. Let us understand the indicators of an implied volatility chart through the discussion below.

- Implied volatility does not depict whether the price movement will be positive or negative.

- High implied volatility means that there will be a large price swing. It may either move higher in the upward direction or very low in the downward direction or might swing too much in between both ends.

- Low implied volatility means that the price swing will be minimal.

- It differs from historical volatility, which measures the volatility based on historical data.

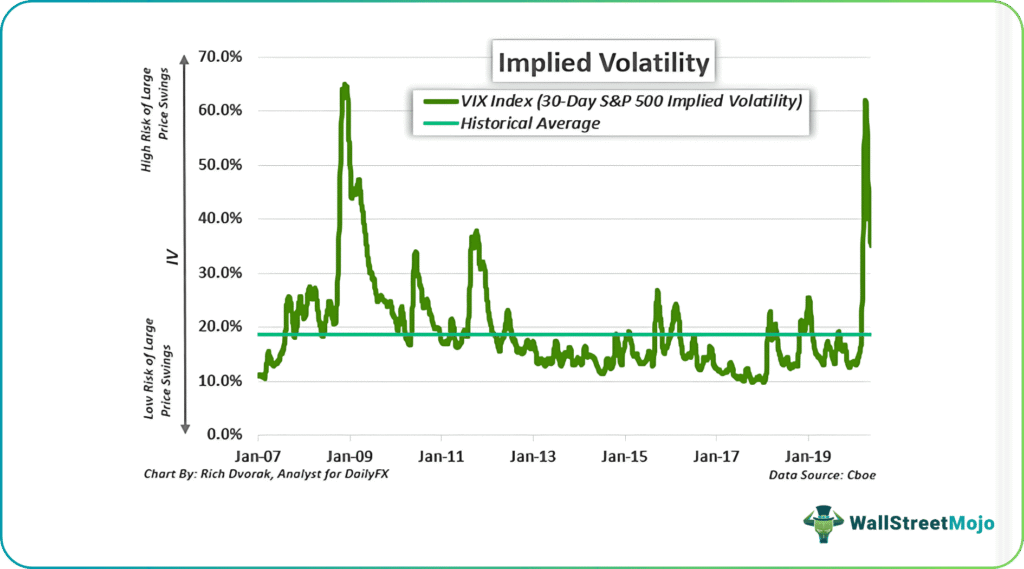

Given below is a chart related to implied volatility. The numerical values given in percentages denote the volatility or the level of risk that traders may have to bear. This shows the variation degree of a particular financial instrument like commodity, stock or index or even a currency pair. It is important for option traders to have a good concept regarding the same because it is applicable to both put option and call option. It also denotes the market sentiments are help identify the resistance and support levels.

Examples

Let us understand the concept of an implied volatility calculator with the help of a couple of examples. These examples will give us insights into the intricacies of the concept.

Example #1

Pixer LLP stocks are currently trading at $50 per share in the market. Suppose the market assumes that the share price will rise, which will result in an increased demand for the shares. Since the demand for the shares increases, there will be an increase in implied volatility, which will make the premium for the option much higher.

Let’s assume that the implied volatility for this stock is 20%. The lowest price in one year was $32, and the highest in the same year was $64. The market predicts the price to move within 20%.

- 20% of $50 upwards is $60

- 20% of $50 downwards is $40

The market assumes that the stock’s price by the end of the year will be between $40 and $60. As per the theory, 68% of the market assumes that the price will be within the range mentioned above, whereas the remaining 32% think that the price will fall below $40 or go above $60.

As an investor, looking at the numbers, the most appropriate strategy can be adopted for the investor to reap maximum profits from their investment. Although, these calculations are based on market consensus and are not foolproof, and might result in a loss of investment for the investor. But looking at the figures, one can decide what strategy needs to be adopted for a particular security. The market might not move as expected by the market consensus, as seen in many past incidents where the market behaves purely differently from what the market participants expect it to do.

Example #2

Full House Resorts, Inc. is a casino operator and developer based out of Nevada. They operated five casinos in 2023. In July 2023, experts warned the investors in this stock as the stock price reached $5 per share.

It had one of the highest implied volatility among all equity options in the period. It also showed a ‘SELL’ tag for the gaming industry on the whole as prominent traders did not increase their investments in this area and their earnings had been reduced from 14 cents per share to a mere 8 cents per share.

However, the option trends might suggest that there is heavy trading activity being formed. Traders would hope that the share does not move as much as it was originally predicted to move to make significant premiums.

Advantages

Let us understand the advantages of using an implied volatility calculator through the discussion below.

- Option prices are decided based on implied volatility.

- It measures the uncertainty of any change in the security price based on the market sentiment.

- An investor or a trader can formulate their trading strategy by analyzing an option’s implied volatility.

- It helps in understanding whether the price movement will be too high or low, which gives an idea to the investors on how much to invest in security.

Disadvantages

Despite the handful of advantages mentioned above, there are a few factors from the other end of the spectrum that prove to be a hassle for traders. Let us discuss the disadvantages of the movements in an implied volatility chart through the explanation below.

- Implied volatility does not indicate how the security price will move. It only shows whether the move will be high or low.

- Any news relating to security can impact implied volatility, making it sensitive to unforeseen events.

- The fundamentals are not considered when calculating implied volatility based on prices, supply & demand, and time value.

- Highly dependent on market consensus can result in the incorrect decision-making of strategies, resulting in an investment loss.

Recommended Articles

This has been a guide to Implied Volatility and its definition. Here we discuss the meaning of implied volatility with examples, advantages, and disadvantages. You can learn more about derivatives from the following articles –