Part of our Banking Services and Operations guide

Mobile Banking Meaning

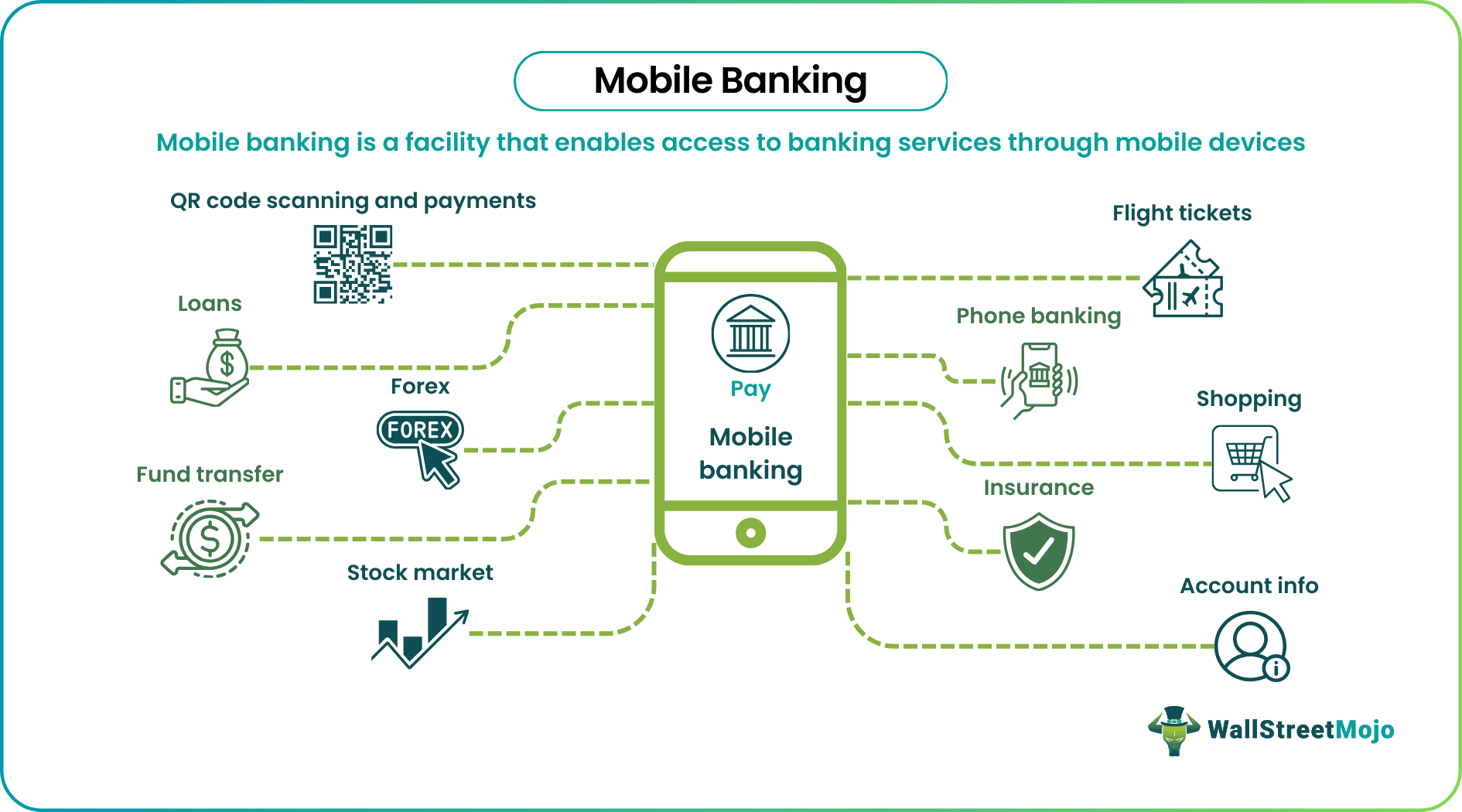

Mobile banking (m-banking) refers to the use of a mobile device to access banking and financial services offered by banks. It enables customers to check their bank account balance, conduct online transactions, transfer funds, pay bills, etc., without visiting banks.

Customers use m-banking through SMS, unstructured supplementary service data (USSD), or an application (app) provided by the bank installed on their mobile device. On the one hand, it offers the customers the convenience of using banking services anytime, anywhere. On the other hand, it also cuts banks’ operating expenses and widens their customer base. However, it comes with its share of downsides. It is vulnerable to security threats and is not preferred by less tech-savvy customers.

- Mobile banking (m-banking) refers to the use of a mobile device like a smartphone or tablet to perform banking activities. It is done through a mobile app, USSD, or SMS.

- It enables customers to access banking services easily, quickly, and conveniently anytime, anywhere.

- Customers utilize mobile banking to view and monitor account details, transfer funds, apply or repay a loan, make investments, lodge complaints, deposit checks, etc.

- The key difference between mobile and internet banking is that the former uses a mobile device while the latter employs a desktop or PC.

- M-banking is susceptible to online frauds but safety features like two-step OTP verification, biometric login, and antivirus help to secure transactions.

Mobile Banking Explained

M-banking refers to the use of the internet and mobile technology to bring financial services to customers. Customers use m-banking through a USSD, SMS, or mobile app to access banking services. As a result, it has eliminated the customers’ need to visit the bank branch for every other financial necessity.

Busy lifestyle and, more recently, the COVID pandemic have forced people to opt for mobile banking. Round-the-clock banking services at the fingertips provide customers with an easy, quick, and hassle-free experience. At the same time, banks also benefit from a reduction in operating costs due to savings in time and resources. Additionally, the rise of AI agents in finance has further enhanced the banking experience, enabling more personalized and automated services.

Though beneficial, m-banking is exposed to security threats like hacking that raise safety concerns among customers. In order to secure transactions, banks keep updating the security features of their m-banking app regularly. In addition, they also use a virtual private network (VPN), biometric login, SASE security, and two-step OTP-based verification to ensure safety of customers.

To access m-banking, customers must download the bank’s m-banking app from the app store. Then, proceed to create an online account to register for the same. It involves answering some questions, selecting a username and password, and setting up security preferences. After that, set an MPIN to be used every time a transaction is made.

Once the bank verifies the credentials, the customer becomes the registered user and can perform all the financial transactions using the mobile app. It includes shopping online, paying utility bills, making account information inquiries, transferring funds, using forex-related services, and booking tickets.

Bunq Core offers essential banking services with no monthly fees, including a personal French IBAN, mobile banking, and SEPA transfers. It’s a solid entry-level account for anyone seeking simple, modern banking without unnecessary costs.

History

Let us discuss the m-banking history to know its origin. The earliest form of m-banking was performed using SMS in the 1990s. However, with the introduction of the mobile web and smartphones with wireless access protocol (WAP) in 1999, banks in Europe started offering m-banking platforms to their account holders.

Until 2010, banks were utilizing the mobile web and SMS to offer banking services on the customer’s mobile. But after 2010, the advent of the following factors revolutionized the m-banking completely:

- Development of iOS by Apple and Android by Google for smartphones

- Emergence of web-based technologies (WBT) like CSS3, HTML 5, and JavaScript

WBT enabled the launch of web-based and mobile-based applications for banks on Android and Apple devices. As a result, banks started incorporating advanced features in their apps to attract customers. The enhanced functionality of apps with easy accessibility worked as bait for the customers. Thus, over the years, these m-banking apps emerged as the new normal globally.

Types of Mobile Banking Services

M-banking allows banks to offer a range of financial services to customers. From accessing account information to utilizing transaction, investment, loan, and support services, m-banking has assumed all roles traditionally requiring the help of a bank representative.

#1 – Account Information

The account holders can:

- Extract the details related to accounts like bank statements

- Enable or disable SMS alerts of transactions

- Manage the fixed deposits and recurring deposits

- Know the loan details and statements

- Get debit card details

- Obtain credit card statements

- Understand and invest in insurance details

- Perform investment in securities

#2 – Transaction

Customers can transfer funds between self-operated accounts, make payments to third-party bank account holders, and undertake utility bill payments, premium payments, and loan repayment using the mobile-based application. Moreover, many banking apps also integrate online shopping for the ease of customers laced with offers, cash backs, and rewards upon using these services.

#3 – Investments

Many banks offer the facility of managing the investments like deposits, insurance, and equities from their m-banking interface embedded in the app.

#4 – Loans

Banks provide the window of loans management to their customers. Customers can check the status of their loans, pay their EMIs, and even avail small digital loans using the app-based mobile utility.

#5 – Customer Support

All banks provide a dedicated menu in their m-banking app to submit requests for services like cheque book, debit & credit card, and loan applications. The account holders can also check their ATM card and credit card reward points from the banking app.

#6 – Content services

Several banks serve their customers with various loyalty programs, online shopping discounts, recharge offers, and other finance-related news through m-banking.

#7 – Consumer Complaints

Customers can lodge complaints about any forgery or invalid transaction from their accounts using the app.

Mobile Banking Features

M-banking has features that ensure customers can access their accounts and carry out financial transactions on the go. Some key features of m-banking are:

#1 – Accessibility

M-banking offers 24-hour access to all customers. Customers can log in to their app and view and track their account balances anytime. Besides, they can engage in fund transfers even during bank holidays.

#2 – Security

The banks recognize the importance of providing a secure environment to customers for transactions based on the banking app. Hence, m-banking asks for SMS access, location access, biometric access, and application password from the customers to ensure their privacy and security.

#3 – Transferability

Transferring funds from one bank account to another is the most basic m-banking activity. All the banking app-based transfers are now secured using two-step verification via app password and OTP-based transactions. The two-step verification is applicable in fund transfers, utility bill payments, and online shopping for the safety and convenience of customers.

#4 – Investment Management

Many big banks offer the facility of securities trading through their banking app. It makes it easier for the customers to trade hassle-free. Also, m-banking enables customers to track their deposits and other investments from the convenience of their homes.

#5 – Digital Payments

At present, all m-banking apps have a QR code reader for payment at merchant locations. So the customer has to point at the QR code of the merchant at their shops and pay the price of the goods using the account details from the QR code.

#6 – Customer Service

M-banking provides personalized service to customers through live chat, phone, notifications, etc. This helps customers to get the required assistance without visiting the bank directly.

M-banking Advantages and Disadvantages

Like every other technology, m-banking can be advantageous as well as disadvantageous to customers. Therefore, one must know its pros and cons to stay safe.

Advantages

- Offers 24-hour accessibility to banking

- Saves time

- Provides a convenient way of making fund transfers and payments

- Enables easy tracking and monitoring of bank accounts

- Facilitates quick reporting of any illegal transaction or fraudulent activity

- Allows swift redressal of consumer complaints

- Increase request processing speed

- Makes online shopping possible

- Allows trouble-free management of investments

- Sends notification of bill or loan payments

- Encourages customers to stay indoors during a pandemic

- Eliminates the need to carry cash all the time

- Reduces chances of theft

Disadvantages

- Causes inconvenience for less tech-savvy account holders

- Removes human touch from banking

- Raises security concerns and online fraud

- Results in delays or losses in transactions due to mistakes

- Gives rise to comprehension issues due to the complex app interface

- Makes follow up on fraud reports difficult

- Delays service requests in case of internet issues

Mobile Banking vs Internet Banking

M-banking and internet banking both are online modes of conducting banking transactions. Both are beneficial to the customers. Customers can use both methods to perform essential banking services. Nevertheless, there are certain differences as listed below:

| Mobile Banking | Internet Banking |

|---|---|

| It is performed by using a mobile device. | It can be accessed using a desktop or laptop. |

| It is based on an app curated by the bank to be used on mobile devices by the customers. | It does not require any such app. |

| It is conducted using SMS, phone, USSD, or an app. | Customers only need a web browser to access internet or online banking. |

| Account-holders can use mobile-based banking without an internet connection also. | Internet banking requires an internet connection. |

| It is more convenient to use. | It is less convenient to use. |

| The mobile app for banking is less secure due to unseen loopholes in coding. | Online banking is more secure as it uses HTTPS secure gateway, which is difficult to hack. |

| It provides limited banking functionality. | It gives a full range of access to banking services to the customer. |

| It is easily available to everyone having a smartphone and is affordable. | It can be used only by people having desktops or laptops, which are costly. |

Frequently Asked Questions (FAQs)

Is mobile banking safe?

Nowadays, m-banking is mostly safe. This is because banks provide biometric login, app password, and two-step verification of OTP with their mobile-based banking app. Moreover, account holders can use antivirus software and VPN to stay safe while using the banking app for transactions on mobile.

How to activate mobile banking?

Customers may download the m-banking application provided by banks. After downloading, they must create an online account to register for access by answering simple questions and creating a username and password. Then proceed to set an MPIN. Note that m-banking is also possible over SMS or USSD.

What is the difference between mobile banking and net banking?

Mobile banking is different from net banking. M-banking can be done using a mobile app, SMS, or USSD. Financial transactions can be made even without the internet. However, net banking always needs an internet connection along with a desktop or PC for its execution.

Recommended Articles

This has been a guide to Mobile Banking & its Meaning. Here we discuss mobile banking service along with its features like online loans, apps, etc. You can learn more about accounting from the articles below –