Part of our Banking and Financial Institutions guide

Murabaha Meaning

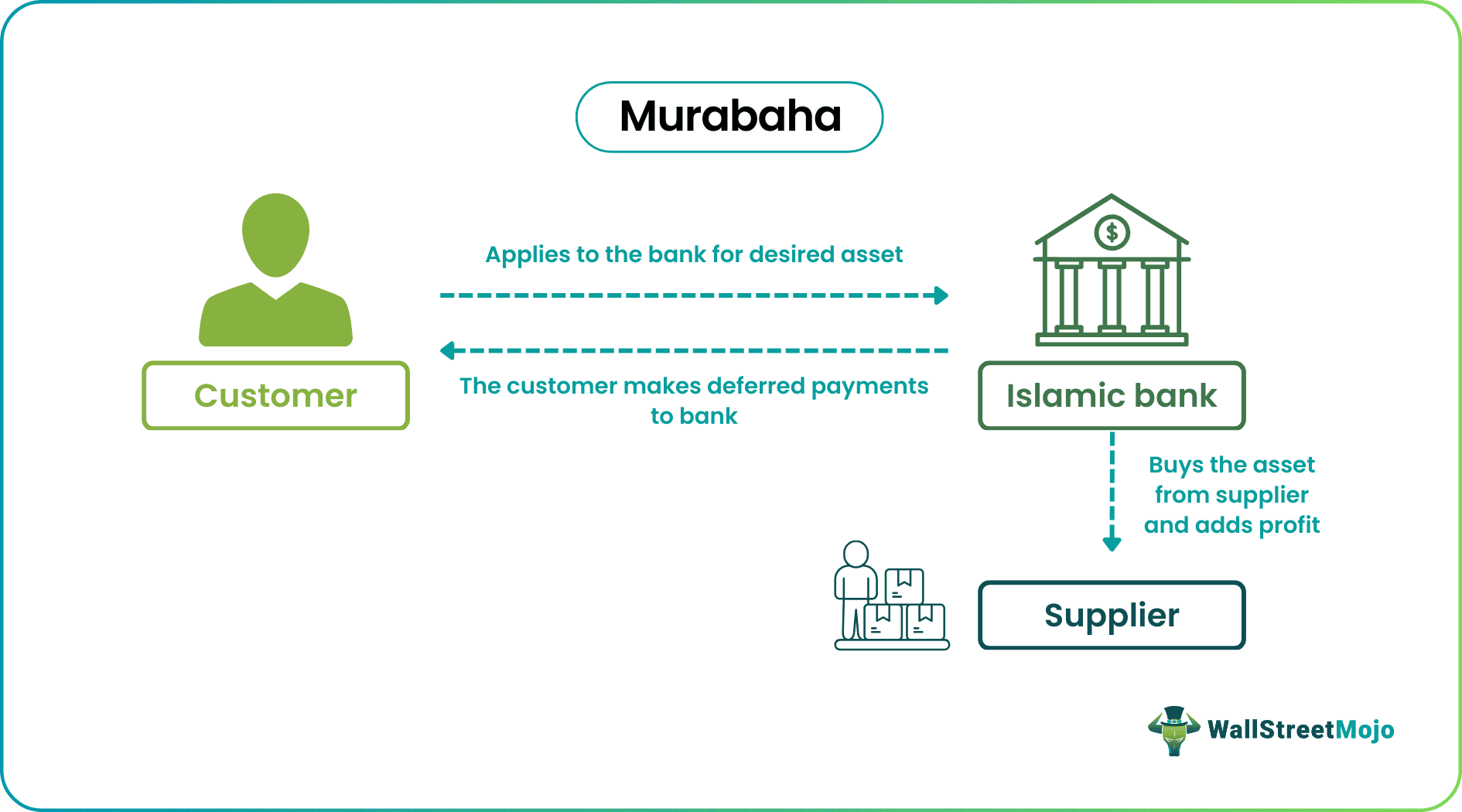

Murabaha (cost-plus financing) refers to an Islamic way of banking where the lender and borrower sign a sales contract for selling goods at a certain profit margin by the lender. It has become the keystone in Islamic banking finance as it helps avoid riba or interest.

It also helps these loans to be Sharia-compliant as it does not involve any kind of interest. Under it, the lender first buys the goods on behalf of the customer, and then, the lender sells these to the borrower at cost price plus the profit margin. After the contract, the buyer repays the Murabaha in installments. It has become the default form of Islamic banking globally.

- Murabaha is a financing contract where the buyer and seller make a cost-plus-profit agreement.

- It allows for financing of trade, home purchases, and working capital without involving any interest, so the process falls under Shariah compliance.

- The main difference between Murabaha and Musawamah remains in the price disclosure of the asset, as unlike in Murabaha, the seller does not disclose the asset to the buyer.

- The difference between ijarah and Murabaha is that in ijarah financier becomes the title holder, unlike in Murabaha, where a customer becomes the titleholder.

Murabaha Explained

Murabaha is a sales contract between the buyer (customer) and the lender (bank), which involves the lender buying an item the buyer has earmarked from the producer and then selling the same item to the buyer at cost price plus profit. As a result, Islamic banks finance the working capital or finance trade or fund house buying in a way that complies with Sharia without involving any interest.

It has the following characteristics:

- Murabaha financing does not involve a loan of any kind.

- The lender sells the asset to the borrower after adding its profit.

- The borrower already knows about the amount of profit taken by the bank.

- Bank calculates profit by subtracting the seller’s price of the item from the price charged by the banker to the borrower.

- The borrower can then either pay the full amount of the asset to the bank or pay in monthly installments, whichever they deem good.

The transaction involved here gets termed as Murabaha transactions. The lender sells the asset, and the bank owns it till it resends it to the customer. As a result, the transactions do not involve any interest in complying with Sharia law. Let us understand how it works.

Suppose a person wants to buy a house but has no capital. It approaches a Sharia-compliant bank and applies for buying the house. The bank buys the house for the person in full cash, then adds a certain profit and allows the borrower to pay the full amount of the house in deferred payment mode or in installments. Thus, the borrower gets their choice of home, and the bank profits from the house.

Examples

Let us look at some examples to clarify the concept of the topic.

Example #1

Suppose Alex wants to buy a machine for its factory. Alex approached the Islamic bank as he heard that it does not charge any interest. Islamic bank asks Alex to submit the details of the machine he wants to buy. After that, the bank buys the machine at a cost-plus financing contract which Alex signs and discloses the real price of the machine and the profit margin it charges. Thus, Alex becomes the owner, but Alex must repay the bank’s full price plus profit before he can claim complete ownership.

Example #2

Eliot wants to buy a house for the family. Eliot approaches an Islamic bank for the reason of no interest but rather cost sharing. The Islamic bank bought a house that Eliot needed without disclosing the original price and added its profit margin before letting Eliot bargain for a suitable buying price. After, the bargaining bank and Eliot settled for 5 million dollars as the selling price to be repaid by Eliot in 30 years, which included profit as well.

Advantages And Disadvantages

Let us understand the advantages and disadvantages of the Islamic banking financing system using the table below:

| Advantages | Disadvantages |

|---|---|

| It involves a guarantor. | All the cost and profit has to be disclosed to the client. |

| Asset ownership gets transferred to the client hence all the defects on the shoulders of the clients. | The process does not involve flexibility. |

| It comprises multiple contractors | In case of defaults, it involves legal consequences and/or repayments of overdue. |

| Almost fifty percent cost gets retained by the bank by default. | No such things happen here. |

| Only a down payment required | Without a down payment, no loan got granted. |

| There is no interest payment involved. | It tends to be costlier for banks. |

Difference Between Murabaha And Musawamah

Let us analyze the differences between Murabaha & Musawamah in the table below:

| Murabaha | Musawamah |

|---|---|

| Here the buyer knows the actual price of the asset he buys from the seller. | Here the buyer does not know the actual price of the asset sold by the seller. |

| Here the buyer remains under an obligation to buy the asset as it initiated the process of buying it. | The final price of the asset is determined by the bargaining abilities of the buyer & seller. |

| The seller does not require to be honest in the transactions. | Here the seller has to be honest |

| It does not involve bargaining an asset price. | The final price of the asset gets determined by the bargaining abilities of the buyer & seller. |

| It comes under the cost-plus sale mechanism. | It comes under the absolute selling mechanism, where bargaining supersedes the transaction. |

| Murabaha falls in the category of trust-based sales acting transparently under sharia. | It does not come under trust-based sale. |

Murabaha vs Ijarah

Here are the key differences between ijarah and Murabaha.

| Murabaha | Ijarah |

|---|---|

| The title holder of the financed property remains the customer. | Prepayment is allowed to the customer. |

| Here the interest rate remains fixed with the loan duration. | The interest rate remains variable. |

| No prepayment has been allowed to the customer. | Prepayment gets allowed to the customer. |

| It has no provision for refinance. | Prepayment is allowed to the customer. |

| The entire risk of the asset falls upon the customer. | The entire risk of the asset falls upon the financier. |

| In case of late payments by the customer, the bank suffers loss. | The bank could control losses due to the late payment by the customer. |

Frequently Asked Questions (FAQs)

1.Is Murabaha halal?

Yes, Murabaha has been widely accepted as a halal form of transaction by the Sharia board of Islamic countries. It is because it does not involve any interest during the whole transaction.

2.What is commodity Murabaha?

It means buying a specific commodity on a cost-plus-profit basis as per the agreement made between the buyer and seller. This commodity is then sold to a third party, which is often another trader.

3.What is Murabaha financing?

It is cost-plus financing where the seller and buyer agree to buy and sell goods in place of certain markup fees charged by the seller to the buyer. The markup fees take the place of interest, which is illegal as per Sharia laws.

4. What is sukuk Murabaha?

It is understood as an Islamic trust contract having clearly defined markup fees on the original cost of the asset fully disclosed to both parties.

Recommended Articles

This has been a guide to Murabaha and its meaning. Here, we explain its examples, advantages, disadvantages, and comparison with Musawamah and Ijarah. You can learn more about it from the following articles –