Mudarabah Meaning

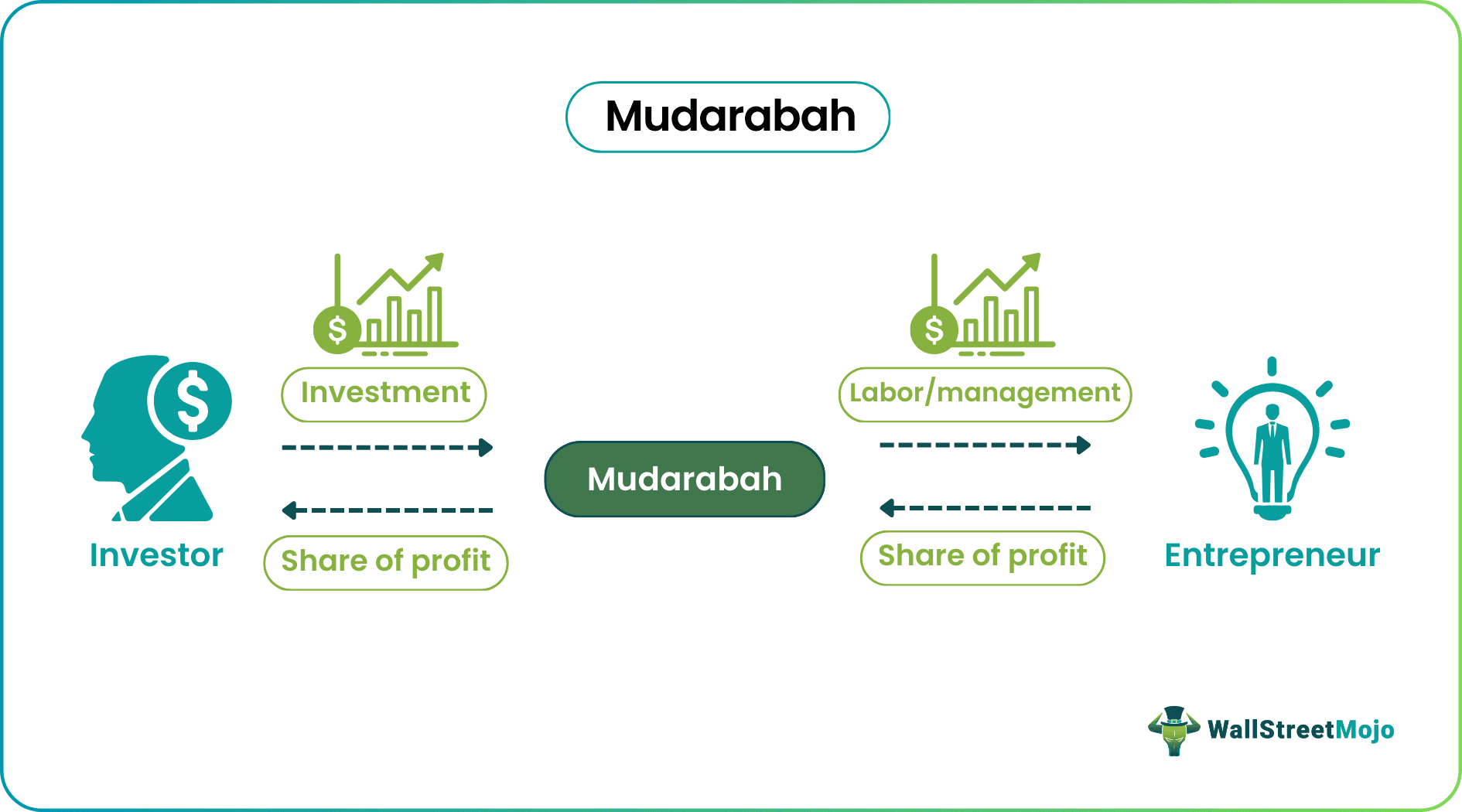

Mudarabah (profit-loss sharing business) is a type of business agreement between two parties where one party provides capital (Rabb-ul-Maal) and the other labor or management (Mudarib) for the business. It helps finance businesses based on profit sharing without involving any riba or interest. Hence, it forms a Sharia-compliant mode of financing.

The financing mode allows investment only in a lawful business and prohibits investment in an unlawful business. Under this arrangement, the Mudarib earns a certain fee for their labor in the business. Any loss becomes the sole responsibility of the Rabb-ul-Maal. However, any profit gets distributed as agreed in the agreement.

- Mudarabah is a form of business partnership in which two partners contribute only capital and labor, skill, and management in return for a share of the business’s profit.

- It streamlines sharia-compliant financing of working capital for a business. The bank has a profit-sharing agreement with the business owner, helping the business grow without any interest.

- It differs from musharakah because musharakah entails equal partnership in business, with partners sharing profits and losses.

Mudarabah Explained

Mudarabah in Islamic banking is a business contract between two parties for profit-sharing where one party, known as the Rabb-ul-Maal, provides the full capital, while the other, the Mudarib, manages the business. Mudarib runs the business operations, and the Rabb-ul-Maal owns the Mudarabah capital. Hence, it has been termed a profit-loss-sharing business. In Islamic banking, Mudarib and Rabb-ul-Maal have different and distinct roles.

Under the arrangement, both parties can not interfere in each other’s work. Although Mudarib or the agent manages the business for profitability, Rabb-ul-Maal has every right to define e working conditions in the contract for better management of the business and profits. As a result, Rabb-ul-Maal gets termed as a sleeping partner in the business. The parties share the profits in any form and ratio they want. However, any loss gets borne by the Rabb-ul-Maal, and the Mudarib loses the fee or enumeration.

In the case of a single profit-loss sharing business, banks form a contract with a person or firm for capital investment on a profit-sharing basis. In a joint profit-loss sharing business, many investors and one bank can have a business relationship on a profit-sharing basis. Most Islamic investment funds work on the principles of joint profit-loss sharing business.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Examples

Let us try to understand the topic using some examples:

Example #1

Let us assume that Alex and Kabir entered into a business agreement modeled on the profit-loss sharing business principles. Alex has lots of capital, and Kabir has lots of experience handling real estate business and making it profitable. So, both of them decide to start a real estate business by pre-deciding on the terms of profit sharing. Here, Alex becomes Rabb-ul-Maal, and Kabir becomes the Mudarib.

Hence, Alex handles capital and the profit and loss associated with it. Kabir looks after the management and puts hard work and labor into the business. As soon as the business turns profitable, Alex takes its share of the profit, and Kabir gets its due share of profit in the form of fees from the profit.

Example #2

Another example is related to Alizz Islamic Bank of Oman. The bank won the ‘Mudarabah Deal of the Year 2021’ award at the Islamic Finance News Awards 2021. The prestigious award acknowledges Alizz Islamic Bank’s important role as a Joint Issue Manager in the OMR 52 million OMINVEST Perpetual Sukuk transaction, done with Ubhar Capital SAOC. The award highlights the bank’s dedication to offering Sharia-compliant financial services and its role in helping OMINVEST achieve its goals, such as improving its capital structure, enabling long-term investments, and boosting returns on capital.

Advantages And Disadvantages

Some of the important advantages and disadvantages are the following:

Advantages:

- It forms the backbone of Islamic banking and finance.

- The return on investment to the customer depends on the business’s actual performance.

- It provides interest-free financing to the business.

- Mudarib only works for a fee and does not get any share in the profit.

Disadvantages:

- The financial aspect of the contract takes a backseat with little scope for development.

- It poses a huge risk to the capital the Rabb-ul-Maal invested.

- The Rabb-ul-Maal cannot hold the Mudarib responsible for the performance of the business.

- Every loss becomes the sole responsibility of the capital investor.

Mudarabah vs Musharakah

The differences between the two are as follows:

| Mudarabah | Musharakah |

|---|---|

| All the investment becomes the responsibility of the Rabb-ul-Maal. | All the member partners invest in the business. |

| Only mudareb takes part in the management of the business. | Every investor partner participates in the management of the business. |

| Any loss is borne by the Rabb-ul-Maal or the capital provider. | All partners equally share the responsibility of loss in the business. |

| The liability of loss is restricted only to the capital investor or Rabb-ul-Maal. | The partners’ liability in loss may exceed their share of the investment if the loss exceeds the capital. |

| Rabb-ul-Maal owns all the goods for selling or business. | Everybody equally owns the goods or business. |

| Profit is shared with Mudarib only when Mudarib brings sales and revenue to the business. | All partners benefit from the increasing value asset even if no profit through sales occurs. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. What are the types of Mudarabah?

Mudarabah can be categorized into “Al-Mudarabah al-Muqayyadah” and “Al-Mudarabah al-Mutlaqah,”. Under “Al-Mudarabah al-Muqayyadah,” the scope and nature of the business are specified. At the same time, “Al-Mudarabah al-Mutlaqah” offers more flexibility in business activities.

2. What are the basic rules of Mudarabah?

The basic rules of Mudarabah include the explicit agreement between the investor (Rabb-ul-Maal) and Mudarib/entrepreneur on profit-sharing plans. The Mudarib manages the business, while the Rabb-ul-Maal provides capital. Additionally, losses are solely borne by the capital provider, emphasizing the risk-sharing nature of this Islamic financial contract.

3. What is the structure of Mudarabah?

The structure of Mudarabah involves two main parties: the Mudarib (manager/entrepreneur) and the Rabb-ul-Maal (investor). The Mudarib utilizes the provided capital for business operations, and profits are shared based on predetermined ratios. Moreover, the structure emphasizes the Mudarib’s autonomy in managing the business while adhering to the agreed-upon terms with the Rabb-ul-Maal.

Recommended Articles

This article has been a guide to Mudarabah and its meaning. Here, we compare it with musharakah, and explain its examples, advantages, and disadvantages. You may also find some useful articles here –