Part of our Banking and Financial Institutions guide

What Is Infinite Banking?

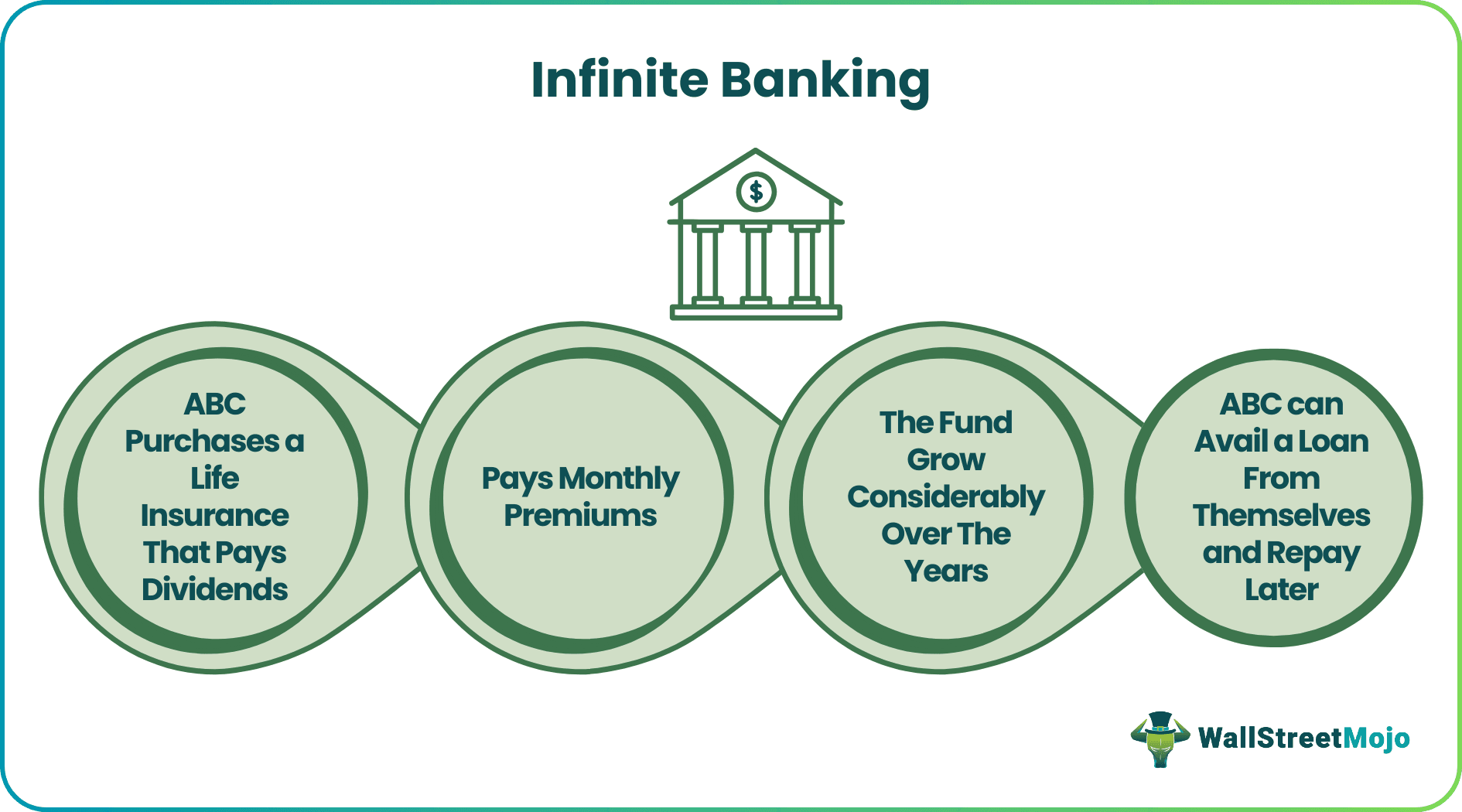

Infinite banking is the series of activities or processes through which an individual can take up the role of a banker. It was conceptualized and documented in the book “Becoming Your Own Banker,” authored by Nelson Nash. The infinite banking concept allows individuals to act as their bank through a permanent life insurance policy that pays dividends as a leveraging instrument.

It is important to note that building sufficient funds before an individual can be their own banker. Moreover, starting early and choosing a reputed insurer can result in lower premiums being paid. The term ‘infinite banking’ is a reference to the loan an individual takes from themselves and repays the same at any given time.

- Infinite banking refers to the activities or processes series through which an individual can take up the banker role. Nelson Nash developed this concept in the book “Becoming Your Own Banker.”

- The features of infinite banking are its overall framework is based on the Whole Life insurance policy; an individual must always pay 10% of his regular income towards retaining and sustaining the whole life policy. Lower loan interest over policy than the conventional loan products get collateral from the wholesale insurance policy’s cash or surrender value.

- It is a concept that allows the policyholder to take loans on the whole life insurance policy. It should be available when there is a minute financial burden on the individual, wherein such loans may help them cover the financial load.

- The Whole Life insurance cash or the surrender value plays as collateral whenever one takes the loan.

Infinite Banking Explained

Infinite banking is adapted from the book “Becoming Your Own Banker” authored by Nelson Nash. Nash describes the practical application of life plan insurance policies that deliver dividends. By taking ownership of such policies, individuals can dictate their terms and effectively use cash flows by leveraging themselves rather than reaching out to lenders or bankers for loans.

Infinite banking system specifically looks into the surrender value of the whole life insurance. Such surrender value acts as cash collateral for a loan. The policyholder needs to connect with the insurance company to request a loan on the policy. A Whole Life insurance policy can be termed the insurance product that provides protection or covers the individual’s life.

In the event of the possible death of the individual, it provides financial security to their family members. The wholesale policy delivers strong dividends, which then add to the effective cash value of the insurance policy. As soon as the policy is effective, it contains a cash value on which the individual can take a loan and keep the policy as collateral.

Usually, infinite banking performs well when the person entirely relies on the banks themselves. Such concepts work well for individuals who have strong financial cash flows. One should only take such policies if the individual is financially sound and can handle the premiums of such policies. The policy may require monthly, quarterly, or yearly payments.

It begins when an individual takes up a Whole Life insurance policy. Such policies may invest in corporate bonds and government securities. Such policies retain their values because of their conservative approach, and such policies never invest in market instruments.

Therefore, Infinite banking is a concept that allows the policyholder to take up loans on the whole life insurance policy. Such loans should be available when there is a minute financial burden on the individual, wherein such loans can help them cover the financial load. The cash or the surrender value of the whole life insurance acts as collateral whenever taken loans.

Example

Suppose an individual enrolls for a Whole Life insurance policy with a premium-paying term of 7 years and a policy period of 20 years. The individual took the policy when he was 34 years old. He has served seven years of the policy and is now 41 years.

He paid a premium of $4,999 monthly. Therefore, the individual paid up to $419,916. If, on the advent of any financial crisis, the individual can take a loan of $419,916 or less. Since the policy invests in corporate and government securities, the policy’s overall value may exceed $419,916.

Features Of Infinite Banking

- The overall framework depends upon the whole life insurance policy.

- An individual should always pay 10% of his regular income towards maintaining and sustaining the whole life policy.

- The loan interest rate over the policy is comparatively lower than the conventional loan products.

- The collateral derives from the wholesale insurance policy’s cash or surrender value.

Advantages & Disadvantages

Infinite banking Concept has its share of advantages and disadvantages in terms of its fundamentals, application, and functionalities. These factors on either extreme of the spectrum of facts are discussed below:

Advantages

- Infinite banking as a financial innovation improves cash flow or the liquidity profile of the policyholder.

- The overall value of the whole life insurance plan is a highly liquid instrument taken up as collateral.

- In financial crises and hardships, one can utilize such products to avail of loans, thereby mitigating the problem.

- It offers the lowest finance cost compared with the conventional loan product.

- The insurance policy loan can also be available when the person is jobless or facing health issues.

- The Whole Life insurance policy retains its overall value, and its performance does not link with market performance. Therefore, one can put that such products are conservative products.

- The loans on such products are tax-free, and one can utilize them as deferred growth products.

- One can transform infinite banking into an estate planning product, and such products one can transfer to dependent individuals as an inheritance.

Disadvantages

- The individual must be eligible to take the whole life policy.

- The premiums on the Whole Life policy are very hefty, which leaves a substantial financial burden on the individual, constraining their financial resources.

- If the financial hardships continue to linger along for a longer time, then there may be a case that an individual may not be able to service such loans and may even default on them.

- In simpler words, he may not make sufficient payments on the policy.

- Suppose the individual lacks financial planning or conviction on utilizing such loans. In that case, infinite banking is not the right methodology for such individuals.

- Such products only favor those individuals who have a strong financial background.

- They must display good levels of financial discipline.

- Such products do not obey the principle of diversification.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions

Does infinite banking work?

Generally, infinite banking policy acts well if one entirely relies on banks themselves. These concepts work for those who possess solid financial cash flows. In addition, one must take only such policies when one is financially well off and can manage the policies premiums.

Is infinite banking a good idea?

Infinite banking is not a scam, but it is the best thing most people can opt for to enhance their financial lives.

Does infinite banking work in Canada?

Yes. One must know that in Canada, the policy loans are taxable above the Adjusted Cost Base (ACB).

Is infinite baking legit?

Infinite banking concept is indeed legit. It is not a scam. But unfortunately, most people believe they have been scammed after buying a not-designed whole life redeploying dormant savings accounts method with ongoing cash flows by a life insurance policy to make continuous compounding on these funds even if borrowed.

Recommended Articles

This article is a guide to Infinite Banking and its meaning. We discuss Infinite Banking’s example and features along with its advantages and disadvantages. You may learn more about financing from the following articles: –