What Is National Insurance Contributions (NIC)?

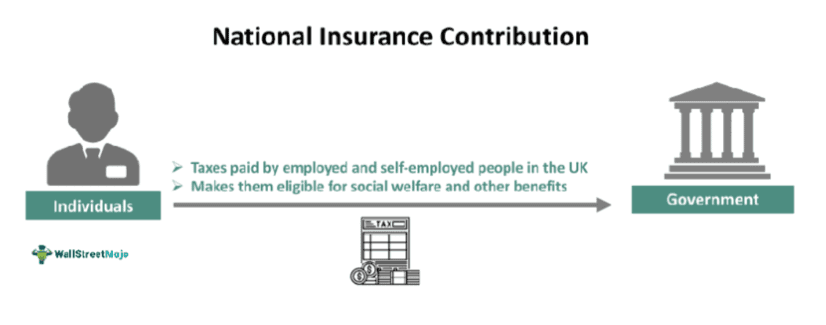

National Insurance Contributions (NICs) are a form of tax paid by individuals in the United Kingdom to fund various social welfare programs, including the National Health Service (NHS), the State Pension, and other benefits. NICs are mandatory for employed or self-employed people falling under specific categories in the UK. The contributions are typically deducted from people’s wages or profits, depending on whether they are employed or self-employed.

These contributions are important because they make individuals eligible for certain state benefits and entitlements, such as the state pension, unemployment benefits, and healthcare services through the National Health Service (NHS). NICs are typically deducted from an individual’s earnings through their employer’s payroll.

Key Takeaways

- NIC stands for National Insurance Contributions. It is a system where contributions or taxes are paid by individuals and employers in the United Kingdom to fund various state benefits and services,

- ncluding the National Health Service (NHS) and the State Pension.

- NICs are mandatory for most employed and self-employed people in the UK, and the amount paid is typically based on an individual’s earnings or profits.

- These contributions offer individuals access to healthcare services, unemployment benefits, and retirement benefits, among other benefits under social welfare programs.

- NICs are an essential part of the UK’s social security and tax system.

National Insurance Contributions Explained

National Insurance Contributions (NICs) in the United Kingdom resemble the Federal Insurance Contributions Act (FICA) — the withholding taxes in the United States. Here is an overview of how NICs work:

- Employee and Employer Contributions: Both employees and employers contribute to NICs. Employers deduct the employee’s portion of NICs from their wages and make independent contributions on behalf of their employees. Self-employed individuals are required to contribute or fund both parts themselves since no external entity (employer) is involved in such cases.

- National Insurance Number (NIN): To pay NICs, individuals need a National Insurance Number (NIN), which is similar to a Social Security Number (SSN) in the United States. It is a unique identifier for each taxpayer.

- Eligibility Criteria: Individuals must meet certain criteria to be liable for NICs, including:

- Contributors must be 16 years or older.

- Earning more than a specific amount (threshold between £242 and £967, which may vary) per week, or if a person is self-employed with an annual profit above a certain threshold (£12,570).

- Voluntary Contributions: Employees can voluntarily make extra contributions to increase their entitlement to state benefits, such as a higher pension in the future. Self-employed individuals and UK citizens employed abroad can also make voluntary contributions for pension eligibility.

- Funding Benefit Programs: NICs fund various benefit programs, including the National Health Service (NHS), the State Pension, and other social welfare benefits. The contributions are categorized into different classes based on an individual’s employment status and income.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

History

The history of National Insurance Contributions (NICs) in the United Kingdom represents the interesting evolution of social welfare programs and government policies. Here is a brief overview:

- National Insurance Act of 1911: The National Insurance Act of 1911 laid the foundation for National Insurance. Initially, it provided government-funded unemployment benefits. In those times, private trade unions, certain approved societies, and other professional associations were in charge of health insurance and pension benefits. Also, the Old Age Pension scheme was introduced for people over 70.

- World War II and Expansion: World War II prompted the British government to consider making insurance more inclusive. In March 1943, Prime Minister Winston Churchill announced the following on radio — “National compulsory insurance for all classes for all purposes from the cradle to the grave”. This marked a significant shift in the scope of social insurance.

- Full Implementation in 1948: The comprehensive National Insurance system in effect today was not formulated until 1948. This marked a significant milestone in the development of the UK’s social welfare system.

- 20th Century – Changes Assimilated: Throughout the 20th century, the National Insurance system improved, and changes were assimilated in the existing system to strengthen it. This boosted the funding levels for various social programs, including:

- The National Health Service (NHS): It provides healthcare services to all residents.

- Public Retiree Pension Plan: It increased the pension benefits.

- Unemployment Benefits: It offers financial support to those out of work.

These changes were introduced to offer more comprehensive insurance facilities for citizens, covering healthcare, retirement, and unemployment support.

Benefits And Coverage

National Insurance Contributions (NICs) in the United Kingdom fund a range of benefits and coverage for eligible individuals. Here are some key benefits and coverage areas provided through NICs:

- State Pension: NICs contribute to an individual’s entitlement to the State Pension. The amount one receives depends on their NIC records, with a higher record leading to a larger pension.

- National Health Service (NHS) Healthcare: NICs help fund the NHS, providing access to healthcare services, including doctor’s visits, hospital care, and other medical treatments for residents.

- Maternity and Paternity Benefits: NICs contribute to benefits for new parents, including maternity pay, paternity pay, and shared parental leave, allowing parents to take time off work to care for their newborns.

- Unemployment Benefits: NICs extend unemployment benefits, providing financial assistance to individuals who are temporarily out of work and actively seeking employment.

- Disability Benefits: NICs fund disability benefits, offering financial support and assistance to individuals with disabilities or long-term health conditions.

- Bereavement Benefits: NICs provide bereavement benefits to widows, widowers, and surviving civil partners, helping them cope with financial challenges after the loss of a spouse or partner.

Categories & Rates

National Insurance Contributions (NICs) in the United Kingdom are categorized into several classes, each with its own rates and thresholds. Here is an overview of the main NIC categories and their corresponding rates:

1. Class 1 NIC Rates and Threshold

- Primary (Employee) Rate: This rate is a percentage of the employee’s earnings. The percentage applied depends on the level of earnings. There are lower and upper earnings thresholds that determine the portion of earnings subject to Class 1 NICs. These thresholds are reviewed annually. The Lower Earnings Limit (LEL) is £123, while the Upper Earnings Limit (UEL) is £962. This is the basic criterion, with other factors being considered for further contribution computations.

- Secondary (Employer) Rate: Employers also contribute to NICs on behalf of their employees. Like the primary rate, it is a percentage of the employee’s earnings and is subject to annual thresholds review.

2. Class 2 NIC

It is applicable to self-employed individuals, irrespective of the profits they earn; it is levied at a fixed weekly rate. The rate may be subject to annual adjustments to account for the relevant economic changes.

3. Class 3 NIC Rates and Thresholds

Class 3 NIC rates are payable weekly—a fixed amount per week is required to be paid. Individuals wishing to fill gaps in their NIC record can opt for these voluntary Class 3 contributions. Opting for such payments increases their eligibility to receive state benefits.

4. Class 4 NIC Rates and Thresholds

Class 4 NIC rates apply to self-employed individuals and are calculated as a percentage of their taxable profits. The rates are divided into two bands, with different percentages applicable to eligible self-employed individuals based on the profits they make.

5. Annual Updates and Changes

Rates and thresholds for NICs are reviewed and updated annually by the UK government. These updates typically consider inflation, changes in the economy, etc. Any changes to NIC rates and thresholds are usually announced during the annual budget and implemented when the new tax year commences.

Examples

Let us look at some NIC examples to understand the concept better.

Example #1

Consider a hypothetical scenario where Jane works as a full-time employee in the UK. Let us assume her monthly earnings exceed the current earnings threshold for Class 1 NICs. As a result, both Jane and her employer contribute a percentage of Jane’s earnings towards National Insurance. These contributions go towards funding state benefits such as the National Health Service (NHS) and the State Pension.

This ensures Jane has access to healthcare services. She will also be eligible for the State Pension in the future based on her NIC records. In this way, the system can help Jane access the services and facilities she needs to live comfortably in the UK.

Example #2

According to a June 2023 press release, the UK government has extended the deadline for taxpayers looking to fill gaps in their National Insurance records from April 2006. The new deadline is 5 April 2025. This will allow individuals more time to consider boosting their State Pension entitlements. Initially set for 31 July 2023, this extension aims to ensure that hardworking individuals have ample opportunity to review their records and make voluntary contributions if necessary. Individuals in large numbers have already taken advantage of this extension, with more expected to follow suit.

By extending the deadline, the government aims to give people the flexibility to spread the cost and secure their State Pension entitlement. Eligible individuals, including those with low earnings, unemployed people, self-employed individuals with small profits, and those living or working abroad, can benefit from this opportunity. However, before proceeding, they should assess whether it will benefit them in their specific situations.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

How to top up national insurance contributions?

Taxpayers can top up their contributions through voluntary payments. It is advisable to contact the right departments or authorities and pay in line with the government’s guidelines. Boosting the size of voluntary contributions helps individuals get access to increased State Pension and other benefits.

What do class 3 national insurance contributions cover?

Class 3 National Insurance Contributions (NICs) in the UK are voluntary payments individuals can make to fill gaps in their NIC records primarily to increase their State Pension entitlement. By closing these gaps, individuals can secure a higher State Pension when they retire. While Class 3 NICs primarily impact State Pension entitlement, they can also indirectly affect eligibility for other benefits based on one’s NIC record.

Who is responsible for national insurance contributions?

National Insurance Contributions (NICs) in the United Kingdom are the responsibility of both employees and employers, depending on the class of NIC. The government sets the rates and thresholds for NICs, and both employees and employers (or self-employed individuals) have legal obligations to ensure that the correct NICs are paid and reported to HMRC.

What is the minimum national insurance contribution uk?

Employed individuals pay NICs when their weekly earnings exceed £242 in the 2023/24 tax year. Earnings below this threshold do not require NIC contributions. Earnings between £242 and £967 per week are subject to a 12% NIC rate. This means 12% of an individual’s earnings within this range go towards NICs. For earnings above £967 per week, a lower rate of 2% applies. So, only 2% of the earnings above this threshold contribute to NICs.

Recommended Articles

This article has been a guide to what is National Insurance Contributions (NIC). Here, we explain it with its categories, rates, history, benefits & coverage. You may also find some useful articles here –