Part of our Costing Methods guide

What are the Objectives of Cost Accounting?

Cost accounting means allocating and recording all the expenses incurred till the final result, which clearly distinguishes the costs and allocation for every expense.

- Cost accounting refers to allocating and documenting all expenditures up to the result while precisely identifying the charges and allocation for each item.

- It has various objectives, some beneficial and others foul. It helps immensely in the finalization of financial statements.

- Another benefit of cost accounting, the per-unit cost of production for various items can thus be easily ascertained by accurately assessing all the costs for the corresponding products.

- When cost records are being audited, well-maintained accounts and allocation will influence the auditor’s perception of the company’s compliance efforts and persuade them to provide a favorable report of accounts.

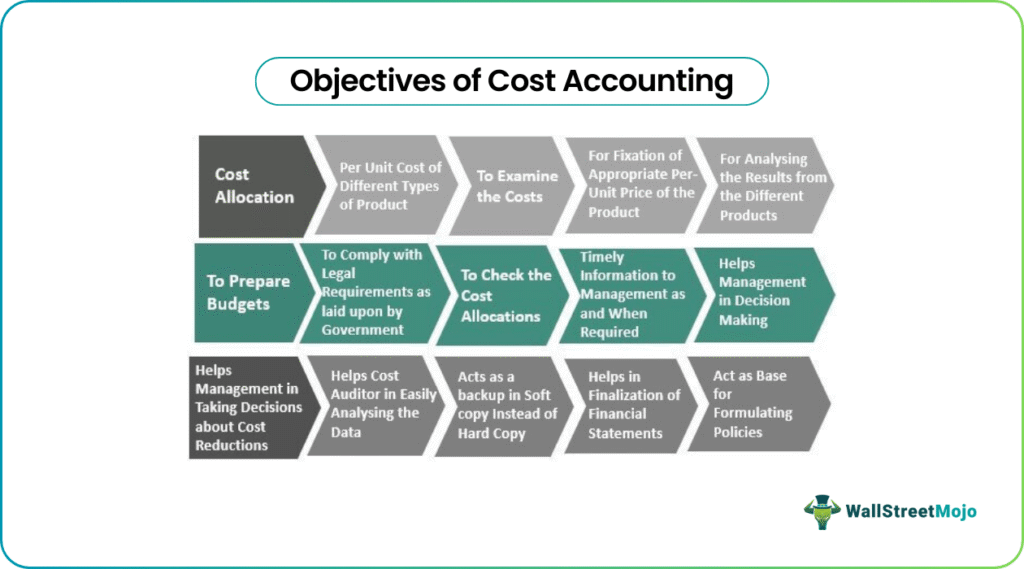

Below is the list of the top 15 objectives of cost accounting –

#1 – Cost Allocation

The primary purpose of cost accounting is to allocate all the expenses incurred to the respective product and bifurcate the cost individually as and for incurred.

#2 – Per Unit Cost of Different Types of Product

Various entities produce many types of products within a factory, and purchasing the required product is common for all the products. Then by correctly analyzing all the costs for the respective products, one can quickly determine the per-unit cost of production for different products.

#3 – To Examine the Costs

Sometimes, the management wants to decide whether to produce the product in-house or outsource the same. For making such a decision, management has to thoroughly examine the costs associated with the production of the product in-house. After that, choose wisely by comparing the same from the outsourcing proposal.

#4 – For Fixation of Appropriate Per-Unit Price of the Product

By correctly allocating all the expenses incurred, one can easily judge the cost of producing or manufacturing the product and the number of units produced. It serves a useful purpose to the management for deciding the per unit selling price of the product to be charged from the purchaser as per market demand and supplies and keeping in view the availability of the substitute.

#5 – For Analyzing the Results from the Different Products

One can quickly determine the production results of every product, such as the cost incurred on procurement of material, labor, overheads, etc., for each respective product or department-wise.

#6 – To Prepare Budgets

Every organization plans its fund utilization and prepares a budget for the production of each product, which needs the analysis of past costs and future requirements, which can easily be seen from the maintained cost records.

#7 – To Comply with the Legal Requirements as laid upon by the Government

Various legal implications were also laid upon the enterprise to maintain and prepare such records as required by the law on a timely basis and in such a manner as prescribed under law. So, for some enterprises, maintaining cost records is also compulsory.

#8 – To Check the Cost Allocations

When all of the expenses are incurred regarding the production process, it helps senior account reconcilers to check whether the proper allocation of all the expenses is done or not.

#9 – Timely Information to Management as and When Required

Sometimes, the budgeted plans are in variance with actual expenses incurred for producing the product. Thus, correctly maintained cost records help the management decide where cost-cutting may be done or should be done.

#10 – Helps Management in Decision Making

As discussed above, timely analysis of the maintained cost account helps management make wise decisions regarding future events to have occurred.

#11 – Helps Management in Taking Decisions about Cost Reductions

It is seen that there may be a variance of costs incurred from the budgets prepared with the actual amount incurred. It may sometimes also be because of the government policies and other factors; for instance, suppose we have a manufacturing plant in a remote area. Due to the weather problem, there is an unavailability of raw material to be used in production. If the same could not be made available for the next ten days, then the cost of labor and other overheads for such ten days will result in extra costs not considered while preparing budgets.

#12 – Helps Cost Auditor in Easily Analyzing the Data

As per the policies and regulations of the Government, such companies fulfill the criteria required to maintain such records in a prescribed manner and get them audited by the person authorized to do so in case of cost records cost auditor. When the cost records are to be audited, then properly maintained accounts and allocation will positively affect the auditor’s mind regarding the compliances made by the enterprise and convince such auditors to issue a favorable report of accounts.

#13 – Acts as a backup in Soft copy Instead of Hard Copy

When records are maintained properly, it helps the management easily check the records maintained as and when required from any remote location. In addition, it serves as a backup of all the physical records maintained in digital form and can be easily kept over the years.

#14 – Helps in Finalization of Financial Statements

At the time of preparation of financial statements, the properly maintained accounts help the financial analysts easily understand the costs and expenses that an enterprise incurred over some time and could also save time.

#15 – Act as Base for Formulating Policies

By analyzing the properly maintained cost accounts, the management and the decision-making team can easily judge the pros and cons of the decisions considered and taken shortly regarding the business’s activities and day-to-day operations. Furthermore, as proper accounting is done by analysis, one could easily formulate the policies laid upon or adhered to.

Cost Accounting Explained in Video

Frequently Asked Questions (FAQs)

What is cost accounting’s fundamental goal?

According to the cost idea, the purchase prices of all assets must be recorded in the books of accounts. It refers to the price associated with installation, transportation, and purchase.

What are cost accounting standards?

The Cost Accounting Standards (CAS) goal is to “create uniformity and consistency in cost accounting methods. Revenue recognition, asset classification, permissible depreciation methods, what qualifies as allowable depreciation, lease classifications, and outstanding share measurement are a few instances of specific accounting rules.

Is cost accounting hard?

Cost accounting might be difficult for individuals who carry out tasks like cost analysis and efficient evaluations. Cost accounting, however, shouldn’t be a very challenging vocation for people with the necessary education and math proficiency.

What are cost accounting systems?

A cost accounting system is a type of managerial accounting that measures a company’s variable and fixed expenses to determine its overall cost of production. It aids in estimating the cost of producing a good or service. System types include process costing and job order costing.

Recommended Articles

Is this article a guide to the Objectives of Cost Accounting? Here we discuss the top 15 objectives, including cost allocation, to examine the costs, prepare budgets, and help management in decision making, etc. You can learn more about it from the following articles –