Part of our Banking and Financial Institutions guide

What Is Private Banking?

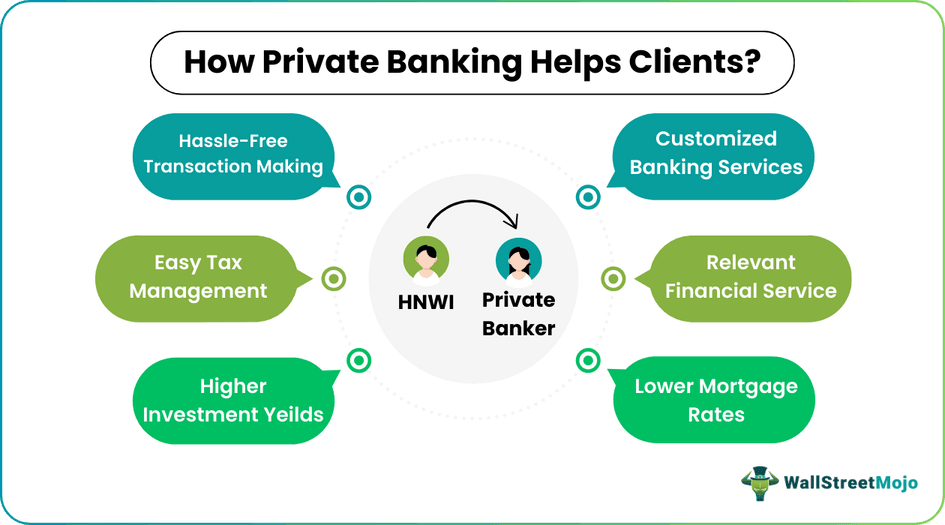

Private banking refers to a type of banking and financial service offered by certain banks only to high-net-worth individuals (HNWIs). Clients opting for this service are individually assigned a financial representative who personally takes care of their banking needs.

Key Takeaways

- Private banking is a form of banking service in which the HNWIs get a dedicated financial representative who manages their banking and financial matters. This facility is available only to high-net-worth individuals (HNWI) who have a certain minimum amount of investable assets.

- The services offered by a private banker differ as per banks. Some of it includes banking transactions and providing discounted rates on loans and investment. Some banks also provide asset investment, mortgage advice, tax, and estate planning.

- Certain banks also offer personalized investment and tailored schemes to help their HNWI clients preserve and grow their wealth.

How Does Private Banking Work?

- A high-net-worth individual (HNWI) possesses wealth more than the average population. According to a World Wealth Report, to be an HNWI, the investable assets must be USD 1 million or beyond. The amount above excludes primary residence and consumables. However, different banks have unique criteria for determining a high-net-worth individual. As such, the threshold differs amongst the banks.

- Given the size of their assets, HNWI individuals need a private banker to oversee their banking activities without undertaking them personally. Also, many banks offer huge bonuses, discounted transactions, lower loan rates, and higher returns.

- The private banker is aware of the financial condition of the HNWI client. Many banks offer advice on asset investment to help preserve and grow the client’s wealth. They also suggest schemes that could prove to be tax-saving and profitable. Depending on the services offered, clients are also informed on tax management services that emerge now and then.

Steps Involved In Private Banking

- Eligibility is the first step in getting a private banker and enjoying hassle-free banking through customized financial services.

- As previously mentioned, to be classified as an HNWI, one must have a minimum investable asset of USD 1 million. However, the figures can vary depending on the banking institution.

- After the eligibility requirements are met, high-net-worth individuals are assigned a private banker.

- The representative handles everything on behalf of its client, from knowing their financial ownerships to depositing checks.

- Certain banks help their clients achieve long-term financial goals through professional advice and recommendations.

Examples

Example #1

Thomson has decided to move from a rented apartment to a house in Switzerland. However, the installments seemed to cost him an arm and a leg. As a high-net-worth client, he contacted his private banker. His dedicated representative informed Mr. Thomson of the lower mortgage interest rates he was entitled to as an HNWI. After that, everything became a lot easier for him to handle. Mr. Thomson applied for a mortgage and bought the home of his dreams.

Many banks are offering this service around the globe. Some of the leading names in private banking include Bank of America, Morgan Stanley, UBS, Credit Suisse, J.P. Morgan, Citibank, and Goldman Sachs. In 2019, Citi Private Bank was awarded the Best Global Private Bank at a prestigious international banking award.

Example #2

The Bunq Elite plan provides a premium banking experience with benefits such as worldwide travel insurance, a personalized Metal Card, and eco-friendly initiatives like planting mangrove trees in Kenya for every €100 spent. Additionally, users receive 4 x 2GB of free worldwide data annually through an integrated eSIM feature.

Is Private Banking Worth It?

It is a concept designed, developed, and implemented keeping in mind the customers’ convenience. Customers who trust a banking brand are more likely to deposit and invest without hesitation. Therefore, these services have been implemented to reward the loyalty of such high-net-worth clients.

- HNWIs get everything they need from their private bankers, from preferential mortgage rates to financial advice. It can be done over the phone without going to the respective bank. Moreover, certain banks create tailored plans for their clients to assist them in achieving their financial objectives.

- From the bank’s or financial institution’s standpoint, it is quite a profitable sector, making it popular amongst many top banks. Despite Covid-19’s crippling effects on the financial sector in 2020, many banks profit from their billionaire clients. UBS received around 4 million quote requests per day from its private clients in the initial months of 2020, double of its December requests. As such, as a career option, private banking careers are a hit, especially in terms of salary. In the United States, the national average salary of a banker doing a private banking job is around $84,228.

- An important element to note is that this sector thrives on the relationship and mutual trust between the client and the advisor. However, factors like the growing number of millennial investors, automation in financial services, and turnover-centric approach hurt the client-banker relationship. Therefore, banks and financial institutions should establish long-term relationships and trust with high-net-worth clients.

Advantages

- It maintains privacy as customer names and transaction details remain confidential.

- Clients are likely to receive the financial products and services at a discounted or comparatively lower rate.

- The exclusive range of services offered to clients may include access to hedge funds and other alternative investments.

- Customers will get all their customized services in one place by calling their dedicated representative.

- Other advantages include higher annual percentage yields on assets and lower annual percentage rates on mortgages.

Disadvantages

- The banks or financial institutions can change the private banker assigned to their clients at any time and replace it with another.

- Higher maintenance fees (fixed or a percentage of investments) because the customers who use the service have higher-than-average assets.

- Interest rates paid on the investments and savings to private banking account clients tend to be lower.

- Banks and financial institutions with a small geographic presence prefer to provide fewer investment products and services to the HNWIs.

- The regulatory requirements require private bankers to be transparent and accountable for their services. As a result, they must exercise extreme caution when providing financial advice to their clients.

Recommended Articles

This has been a guide to private banking and its meaning. Here we discuss how it works, steps, examples, advantages, and disadvantages. You may also have a look at the following articles to learn more –