What Is Business Banking?

Business banking is a specialized bank or financial institution division that deals only with businesses and corporate clients and offers products like business loans, assets management, and electronic transfer of funds specifically designed to meet their needs. These banking services allow corporates to be financially fulfilled for a healthy competition and growth.

Business banking loans do not serve the needs of individual customers. Instead, they directly cater to the needs of the companies/businesses. Though banks majorly focus on this area as these services and clients are their significant source of profit, interest rates, and fees are still higher for corporate clients than retail clients.

- Business Banking is a banking service that suits business corporations’ and organizations’ needs.

- The main services offered include business loans, asset management, electronic transfer, etc.

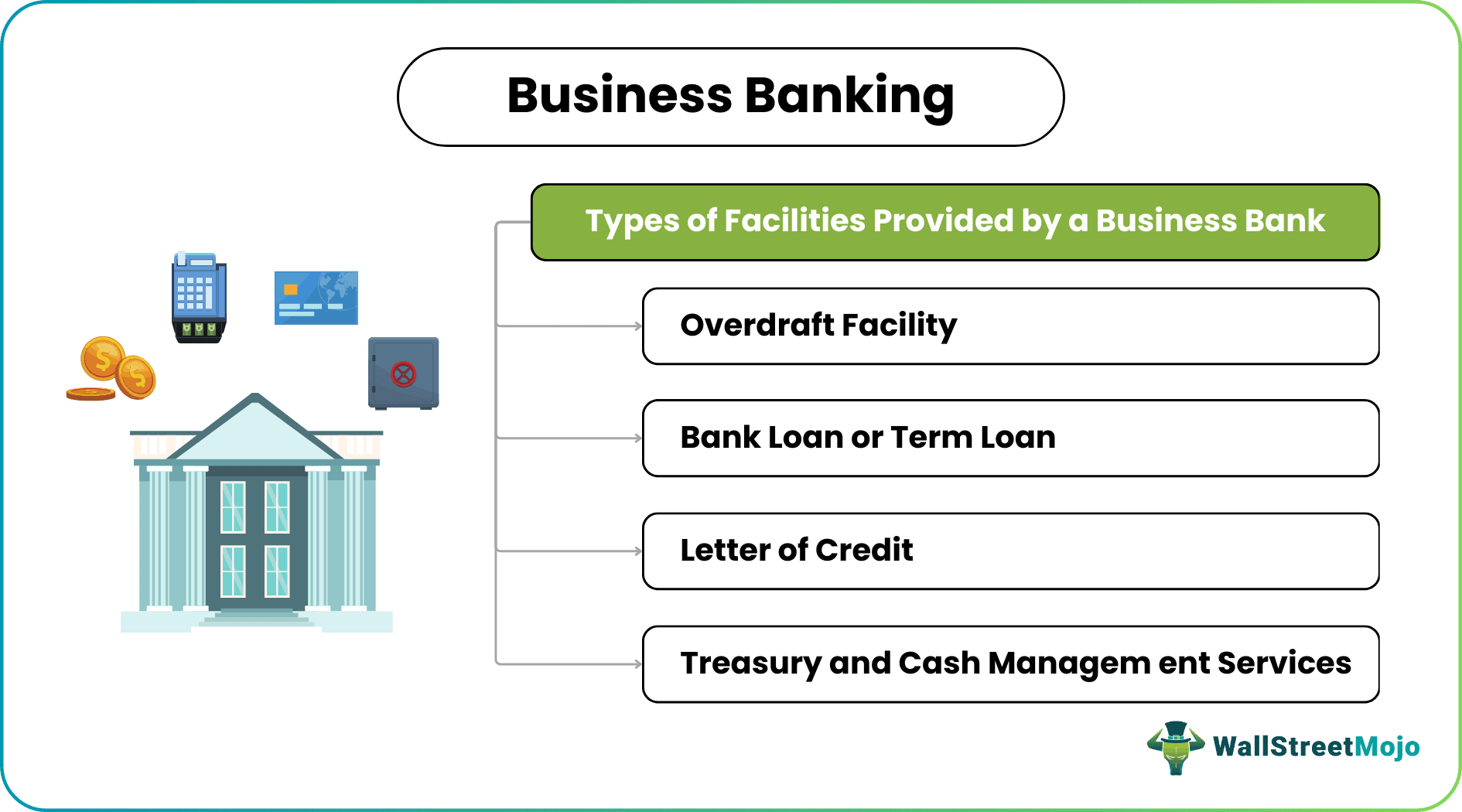

- Banks’ four main features to business organizations are Overdraft Facility, Credit facility, Bank Loan/Term Loan, and treasury and cash management.

- Business Banking has facilitated business organizations in the modern era to function better financially and in operations.

Investors seeking a comprehensive platform may consider Saxo Bank International for a variety of account types and investment options.

Business Banking Explained

Business banking, also known as corporate banking or commercial banking, helps corporate participants to obtain funds when required with the goal of providing them with the best corporate banking solutions using Innovative technologies to ensure the smooth functioning of businesses and create a loyal institutional client base for future growth.

From providing small business banking solutions to being available for the major businesses requiring financial assistance, a banking institution does it all. The major service seekers include corporations, partnerships, Limited Liability Companies (LLCs), and sole proprietorships, The most significant products that these financial institutions have in stock for their customers are everything from physical monetary assistance to electronic fund transfers.

Financial Institutions like Wells Fargo or Barclays bank sign agreements with corporations, which allow companies to use various facilities and services of a bank at fixed service costs. Facilities like short to long-term loans and services like a letter of credit are provided, ensuring a business’s smooth functioning.

Services

The types of business banking services available to corporate finance seekers have been listed below:

#1 – Overdraft Facility

When companies have more cash requirements than the available balance in companies’ current accounts, then companies generally avail overdraft facilities from banks for which banks charge interest rates. Overdrafts are often used as an alternative source of funding for unexpected expenditures. Overdraft is a very common source of funding for small and medium enterprises.

Important characteristic

- Overdraft facility is available as short-term financing and useful for companies with fluctuating finance requirements or a seasonal business cycle.

- An overdraft facility can be used with or without pre-approval from a lender. Generally, a pre-approved facility carries a lower interest rate than without approval.

- Sometimes large overdraft facilities can be secured against company assets, which brings down the Interest rate as the risk to the lender will be lower.

- Interest paid is tax-deductible, and the balance of overdraft is not included in the company’s business financial calculation.

#2 – Bank Loan or Term Loan

When companies want to go for business expansion, like purchasing a new property, plant, or machinery, then companies generally prefer to go for a bank loan that has a fixed tenor with a fixed or variable rate of interest. The loan companies can expand their business through the bank without taking a big hit on an available cash reserve.

Important Characteristic

- Bank loans are the best funding source for medium and long-term business needs.

- The interest rate can be fixed or variable rate. The variable rate is based on LIBOR (London Interbank Offered Rate).

- The company’s revenue generation capability, future cash flow, loan amount, repayment schedules, and loan tenor will be decided.

- If the loan is secured against the company’s assets, interest rates will generally be lower, but in any case, the business fails to repay. The lender has the right to seize the assets and recover the loan amount.

- The default loan payment can increase the Interest rate for future loans and legal proceedings against the company.

#3 – Letter of Credit

A letter of credit or LC is generally used in international trades. Letter of the credit agreement states that, in any case, if the importer (or buyer) is not able to make the payment, then the issuer of LC, i.e., bank, will make full or remaining payment to the exporter (or seller) on behalf of the buyer.

Types of Letter of Credits

- Standby Letter of Credit: In this type of LC, the bank pays the amount only when the applicant of LC cannot make payment.

- Traveler’s Letter of Credit: This type of LC is useful for the traveler, in which issuing banks honor payment requests made at the foreign country banks.

- Revolving Letter of Credit: This type of LC allows any number of payments within a certain limit for a specific time period.

- Confirmed Letter of Credit: Two banks are involved (issuing bank and confirming bank); if the issuing bank or holder of LCs cannot make a payment, confirming the bank ensures payment to the seller.

Important Characteristic

- When a seller from another country cannot determine the reliability of an individual buyer, then letter credit from the buyer side plays an important role in completing the trade.

- Bank takes credit risk based on the buyer’s creditworthiness and takes the service cost for issuing a letter of credit. Charges will be higher if credit risk is higher.

- Aspects such as distance, differing laws in each country, and difficulty in knowing the opposite party personally make a letter of credit even more important.

- A letter of credit helps in better payment terms and timely shipments of goods for both buyers and sellers.

#4 – Treasury and Cash Management Services

Banks provide Treasury management services to cooperate like a collection of payments. Disbursements, trading, and Investment in bonds, foreign exchange. Banks have a special department devoted to treasury management and provide these services at a fixed cost.

Important Functions

- Effective Treasury management helps in the smooth functioning of business and gain lender and stakeholder confidence.

- The main purpose of Treasury management is to ensure a firm’s liquidity position is stable.

- Treasury management helps the company mitigate various operational and financial risks.

Examples

Let us consider the following examples to have a better understanding of business banking services:

Example 1 (Overdraft Facility)

Suppose a small retail firm based out of New York has emergency cash requirements to pay off suppliers. The firm has the option to take a secured overdraft facility against its fixed deposit with a bank. Since an overdraft is secured against a fixed deposit, it will carry a lower Interest rate, and the firm can pay off overdraft principle and interest upon cash receivables.

Example 2 (Letter of Credit)

Suppose a furniture company Ladder Inc. based in the United States, wants to export $100,000 of furniture to a company ABC based in Kenya. Still, Ladder Inc. is concerned about Kenyan companies’ ability to pay them.

So, ABC gets a letter of credit from its bank, Bank of Kenya, indicating that it will make good on the $100,000 payment in 60 days or the bank can pay itself. Bank of Kenya then sends the letter of credit to Company Ladder Inc., which agrees to ship the furniture.

After the shipment goes out, Company Ladder Inc. then asks for its $100,000 by presenting a written draft (also called a bill of exchange) to the Bank of Kenya.

Example 3 (Treasury & Cash Management)

Suppose a company belonging to an export business has a standard requirement for foreign currencies. Then, the company can request the bank’s treasury service to get the best foreign exchange rate.

Business Banking Vs Personal Banking

Though the name business banking and personal banking reveal the services each of them offers, here is a list of differences between them mentioned briefly:

- While business banking is meant to serve the financial requirements of organizations, personal banking takes care of the personal finance requirements of individuals.

- In business banking, companies or businesses need to present and submit formal credentials, including their business license, tax return details, etc, to get their loans approved. On the other hand, personal banking takes into account the credit records of the individuals to assess their profile.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

How is Business Banking different from commercial banking services?

Business Banking involves the banking services that facilitate business organizations and corporations and assist them in financial capabilities. Commercial Banking, on the other hand, is for individual savings accounts.

What are the functions of Business Bankers?

The main functions and operations of Business Bankers include analyzing loan and credit services, assisting business corporations in creating expansion plans, financing corporations, managing cash and cash equivalents, etc.

What are the benefits of employing Business Banking?

The numerous benefits of it include Financial Planning, Cash Management, Checking and Savings Accounts, Credit Building, Tax assistance, and others.

What is the difference between business and commercial banking?

Smaller businesses, especially sole proprietors, typically employ “business” banking services. ‘Commercial’ or ‘corporate’ banking often refers to the products and services utilized by bigger businesses with a significant turnover.

Recommended Articles

This has been a guide to what is Business Banking. Here we explain its types of services, vs personal banking along with examples. You can learn more about financing from the following articles –