What Is A SEP IRA?

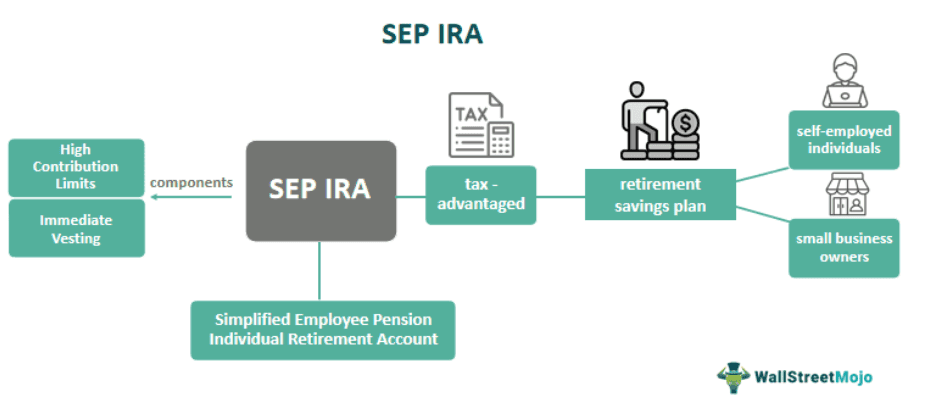

A Simplified Employee Pension Individual Retirement Account (SEP IRA) is a tax-advantaged retirement savings plan for self-employed individuals and small business owners. Its primary purpose is to provide a straightforward and flexible way for these individuals to save for their retirement while offering tax benefits.

Contributions are typically tax-deductible for the employer and tax-deferred for the employees until they withdraw the funds in retirement. The importance of a SEP IRA lies in helping individuals secure their financial future and attract and retain talent within their small businesses by offering a valuable retirement benefit. It serves as a valuable tool for both retirement planning and business success.

Key Takeaways

- SEP IRAs are a straightforward and accessible retirement savings option for self-employed individuals and small business owners. They offer a hassle-free setup process with minimal administrative requirements.

- Business owners can contribute up to 25% of their net self-employment income or 20% of their net earnings if they are sole proprietors, allowing for substantial retirement savings potential. The maximum contribution limit for 2023 is $61,000.

- SEP IRAs provide tax-deductible contributions for employers, reducing taxable income and tax-deferred growth for both employer and employee contributions.

- SEP IRAs require equal contributions for all eligible employees, promoting fair retirement benefits within the organization.

How Does SEP IRA Work?

A Simplified Employee Pension Individual Retirement Account (SEP IRA) is a retirement saving plan that is designed to provide a safety net along with certain tax benefits for self-employed individuals and small business owners. Employers must offer SEP IRA participation to all eligible employees who meet certain criteria, including age and income thresholds. One of the key advantages of a SEP IRA is its simplicity and accessibility.

It works by allowing employers to make tax-deductible contributions on behalf of themselves and their eligible employees, promoting retirement savings without the administrative complexity of some other retirement plans. These contributions must be made at the same percentage of compensation for all eligible employees. It is aimed for retirement relief, hence early withdrawals before age 59½ incur a 10% early withdrawal penalty and income taxes.

Rules

The Internal Revenue Service (IRS) establishes rules governing SEP IRAs to ensure compliance and fair treatment of both employers and employees. Here are the key rules associated with SEP IRAs:

- Eligibility: Eligible employees generally include those at least 21 years old, have worked for the business in three of the last five years, and have earned at least $650 (subject to adjustments) during the year.

- Equal Treatment: SEP IRA contributions must be made equally on behalf of all eligible employees, including the employer.

- Tax Deductibility: Employer contributions are tax-deductible for the business, reducing taxable income. However, contributions are not tax-deductible for employees.

- Employee Ownership: SEP IRAs are owned and controlled by the employees. Thus, they have the right to choose how their SEP IRA funds are invested from options provided by the financial institution.

- Vesting: SEP IRA contributions are immediately 100% vested. This means that employees have full ownership of employer contributions from the moment they are made.

- Distribution Rules: Distributions can begin at age 59½, and withdrawals are taxed as ordinary income.

Examples

Let us look at examples to understand the concept better.

Example #1

Consider Sarah, a self-employed graphic designer, who runs her design studio. She decides to set up a SEP IRA to save for her retirement while providing a valuable benefit to her two employees, Mark and Lisa.

Sarah earns $60,000 in a given year, while Mark and Lisa each earn $40,000. Thus, Sarah can contribute up to 25% of her net earnings to her SEP IRA. So, she decided to contribute 20% of her income, which is $12,000. Since Mark and Lisa are eligible, she must also contribute an equal percentage of their salaries. Thus, Sarah contributes $8,000 (20% of $40,000) each.

The total contributions to the SEP-IRA for the year would be $28,000, helping Sarah reduce her taxable income.

Example #2

Consider Alex, a 35-year-old freelance web developer. She runs her own web development business and has no employees. Also, Alex earns a net self-employment income of $80,000 per year. Hence, she set up a SEP IRA to save for her retirement and reduce her tax liability.

Alex can contribute up to 25% of her net income to her SEP-IRA in a given year. So, she decides to contribute 20% of her income, which amounts to $16,000 ($80,000 * 20%). This $16,000 contribution helps her save for retirement. Over the years, Alex consistently contributes to her SEP IRA, and her contributions have grown tax-deferred.

By the time she retires, she has accumulated a substantial nest egg, allowing her to enjoy a comfortable retirement.

Contribution Limits

Contribution limits for SEP IRAs (Simplified Employee Pension Individual Retirement Accounts) are subject to the IRS’s specific rules:

- Employer Contributions: Employers can contribute to their own SEP IRAs and those of their eligible employees. The contribution limit for employers is up to 25% of their net self-employment income or 20% of their net earnings if they are sole proprietors. However, contributions are capped at the lesser of these percentages or a dollar limit set by the IRS.

- Dollar Limit: The IRS sets an annual limit on employer contributions to SEP IRAs. This limit is subject to change each tax year due to inflation adjustments. For the tax year 2021, the maximum contribution limit was $58,000. For the tax year 2022, it increased to $61,000.

- Employee Compensation: Employee compensation is considered when calculating employer contributions. To calculate the contribution percentage, the IRS may limit the annual compensation that can be considered. The current limit was $290,000.

How To Set Up?

Setting up a SEP IRA involves several steps:

- Eligibility Check: Ensure that the business and owner meet the eligibility criteria, including being self-employed or a small business owner with eligible employees.

- Choose a Financial Institution: Select a financial institution, such as a bank or brokerage firm, to serve as the custodian or trustee for the SEP IRA.

- Establish the Plan Document: Complete the necessary paperwork from the chosen financial institution, including the plan adoption agreement.

- Determine Contribution Levels: Decide on the contribution amount based on a percentage of one’s net self-employment income, up to 25% or 20% if they are a sole proprietor.

- Notify Employees: Inform eligible employees about the SEP IRA plan, its benefits, and how contributions will be made on their behalf.

- Set Up Employee Accounts: Ensure each eligible employee opens their SEP IRA account with the selected financial institution, providing the required personal information.

- Make Contributions: As the employer, make contributions to SEP IRA accounts for eligible employees, adhering to tax-deductible guidelines.

- Report Contributions: Report SEP IRA contributions on the business tax return, following IRS guidelines for limits and deadlines.

Pros And Cons

Let us look at some pros and cons of SEP IRA:

Pros

- Simplicity: SEP IRAs are easy to establish and maintain, with minimal administrative requirements compared to other retirement plans like 401(k)s.

- High Contribution Limits: Employers can contribute a significant percentage of their income, up to 25% or 20% of net earnings for sole proprietors, allowing for substantial retirement savings.

- Immediate Vesting: SEP IRA contributions are 100% vested from the moment they are made, giving employees full ownership of the funds.

- Employee Involvement: Employees have control over their SEP IRAs and can choose how to invest their contributions, providing some flexibility and autonomy.

Cons

- Contributions are Employer-Only: Unlike other retirement plans, employees cannot contribute to their SEP IRAs. All contributions come from the employer.

- Equal treatment Required: Employers must make contributions for all eligible employees at the same percentage of their income. This can be costly if the business has many employees.

- Required Minimum Distributions (RMDs): Like most retirement accounts, SEP IRA owners must start taking RMDs at age 72, which may affect their retirement income strategy.

SEP IRA vs Solo 401(K)

Let us look at the comparison between SEP IRAs and Solo 401(k):

| Parameters | SEP IRA | Solo 401(k) |

|---|---|---|

| Eligibility | Self-employed and small business owners with employees | Self-employed individuals with no employees |

| Contribution Limit (2023) | Up to 25% of net self-employment income, capped at $61,000 | Up to $61,000 ($68,500 if age 50+ with catch-up) |

| Employee Contributions | Employees cannot contribute | Employees can make both salary deferral and profit-sharing contributions |

| Administrative Complexity | Minimal paperwork and administration | More paperwork and administrative responsibilities |

| Contribution Flexibility | Contributions can vary annually | Contributions can be varied, including profit-sharing |

| Employee Loans | Not allowed | Permitted, subject to specific plan provisions |

SEP IRA vs Simple IRA

Let us look at the differences between SEP IRA and Simple IRA:

| Parameters | SEP IRA | SIMPLE IRA |

|---|---|---|

| Eligibility | Self-employed and small business owners with employees | Small businesses with 100 or fewer employees |

| Contribution Limits (2023) | Up to 25% of net self-employment income, capped at $61,000 | Employer matching contributions up to 3% of employee’s compensation or 2% non-elective contributions |

| Tax-Deductible Contributions | Contributions are tax-deductible for the employer | Contributions are tax-deductible for the employer |

| Roth Component | Not typically available | Some SIMPLE IRA plans may offer a Roth option |

| Investment Options | Depends on the financial institution | Typically provides a range of investment options |

| Access to Funds | Withdrawals can start at age 59½ and are taxed as income | Withdrawals can start at age 59½, subject to plan rules |

Frequently Asked Questions (FAQs)

1.Are there penalties for early withdrawals from a SEP IRA?

Yes, if one withdraws funds from a SEP IRA before reaching the age of 59½, it may be subject to a 10% early withdrawal penalty in addition to regular income tax on the distribution. However, some exceptions, such as for certain medical expenses or first-time homebuyers, may allow penalty-free withdrawals. It’s essential to be aware of these rules and consider the long-term nature of a SEP IRA when making withdrawal decisions.

2.Can employees contribute to their SEP IRAs?

No, employees cannot make contributions to their SEP IRAs. SEP IRAs are funded solely by employer contributions. Employees, however, have ownership and control over their SEP IRAs and can decide how to invest the funds within the account. Employee contributions are made to the plan in the form of employer contributions, not personal contributions.

3.Can I convert a SEP IRA to a Roth IRA?

Yes, can convert a SEP IRA to a Roth IRA, but it will be taxable. The amount converted will be subject to income tax in the year of the conversion. Converting to a Roth IRA allows for tax-free withdrawals in retirement. Still, consider the tax implications carefully and consult with a tax professional before making the conversion decision.

Recommended Articles

This article has been a guide to what is SEP IRA. We explain its contribution limits, comparison with solo 401(k) and simple IRA, rules, examples, pros and cons. You may also find some useful articles here –