Part of our Retirement Planning guide

What Is 401k Plan?

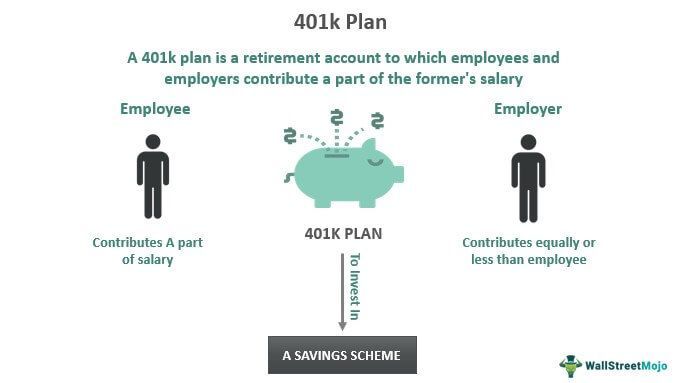

401k plan is a retirement savings plan enabling qualified employers and employees to contribute a part of the latter’s salary for investment in schemes like bonds and stocks. It allows the workers to safeguard a portion of their remuneration for a financially sound life after retirement. Hence, The 401k plan providers fulfill employee expectations and assist the small businesses in maintaining the best talent.

Please note that the Internal Revenue Service (IRS) decides the amount to be contributed. For employees aged below 50, the highest contribution is $14,000 (2022). Moreover, workers aged 50 and above may make an extra catch-up contribution worth $3000.

- The 401k plan meaning denotes a tax-deferred remuneration savings plan wherein employees and employers contribute a part of the latter’s salary to individual accounts.

- The IRS has fixed the contribution limit to $14,000 for workers under the 50-year age bracket. In addition, employees over 50 can make an additional catch-up contribution of $3000.

- It is classified into three types, Traditional, Roth, and Simple 401k plans.

- Investors aged 59.5-72 years may withdraw the contributed amount. However, an early withdrawal can penalize the investor with an additional 10% tax.

How Does The 401k Plan Work?

401k plan is a feature of the eligible profit-sharing scheme, letting workers give away a part of their pay to personal accounts. Moreover, the Internal Revenue Service (IRS) sets contribution limits to the plan for both employee and merged employee/employer, which differ yearly.

To clarify, employees aged 21 years or more qualify for the plan. Additionally, they must acquire one year of work experience or get covered by a collective bargaining contract not offering plan participation (when retirement benefits were the topic of good faith bargaining).

The employee elective deferral limit (for safe harbor and traditional plans) is $20,500 in 2022, based on cost-of-living arrangements. Other than the chosen Roth extension, optional salary deferrals are excluded from the employee’s net income.

So, here are four vital actions to possess the best 401k plan and relish tax benefits,

- Acquire a written strategy

- Organize a financial fund for the plan’s reserves,

- Establish a documentation approach, and

- Offer plan details to contributors

Apart from qualified distributions of assigned Roth accounts, distributions (covering wages) are included in taxable retirement payments.

Types Of 401k Plan

Please note that the 401k plan companies offer various services covering Safe Harbor and Solo plans. Moreover, here are the three most common types,

#1 – Traditional

The most usual type of 401k plan allows contributions with pre-tax currency to enjoy untaxed pay. The disbursements (withdrawals) are taxed as ordinary income, not capital gains. It can lessen the present tax bracket of account holders.

#2 – Roth

In this plan, employee contributions are made with after-tax income; hence, the received profits (capital gains, dividends, or interest) are non-taxable. This plan is fitting for people with a potentially higher income tax bracket after retirement than presently.

#3 – Simple 401k Plan

Like the safe harbor plan, the employer must make fully vested contributions. Moreover, this plan is exclusively accessible to employers with a maximum of 100 workers obtaining at least $5000 in earnings for the previous fiscal year. Therefore, employees might not get benefit accruals or contributions under different plans of the employer.

Examples

Let’s go through some examples to understand the 401k plan meaning.

Example #1

Suppose Nina works with ABC Co. Ltd. and invests in the traditional 401k plan worth $20,000 through her present employer. Now, her contribution comes from the pre-taxed earnings. Resultantly, the contributed amount remains untaxed till the time of withdrawal.

Let’s consider this situation with a Roth plan. So, Nina’s contributions are deducted from her taxed earnings. This way, she can stay assured of no additional taxes on the contributed amount at the withdrawal time.

Example #2

The Boeing defense workers decided to vote on the firm’s modified contract offer on August 3. Under this new plan, workers may get about $8000 payment upon ratification and can let their total amount be deposited in the 401k plan. Moreover, Boeing had dropped its amended 401k match proposal.

The conflict began when The International Association of Machinists and Aerospace Workers (IAM) criticized the firm’s 401k contract remuneration. Presently, Boeing offers a 4% company contribution with a 75% match on the first 8% of a worker contribution.

401k Plan Withdrawal Rules

The IRS permits penalty-free withdrawals from the plan after the investor turns 59.5 (59 years and six months) years old till 72. Moreover, the taxpayers must discuss the issue with their investment manager to avoid confusion and ensure seamless investment in bonds and stocks.

An early withdrawal may cost the investor an additional 10% penalty on the withdrawn amount with relevant income tax. However, the penalty is non-applicable to untaxed withdrawals comprising withdrawals of contributions that the investors already paid tax on.

Rollover is one such type of untaxed withdrawal for the 401k plan for small business, multi-national business, or individual investors. Please note that the excess 10% tax is levied to motivate continuing engagement in employer-endorsed retirement plans.

This rule also has some exceptions like,

- Corrective distributions

- Automatic enrolment

- Disability

- Death

- Domestic relations

- Employee stock ownership plan (ESOP)

- Equal payments

- Medical

- Levy

- Military

- Separation from service, and

- Rollovers

Frequently Asked Questions (FAQs)

1. How To Start 401k Plan?

Follow these steps to start the 401k plan for small business or as an eligible individual investor,

#1 – Check with the employer about the sign-up process

#2 – Select the account type

#3 – Analyze the investment options

#4 – Compare the investment fees

#5 – Ensure sufficient contribution for the employer match

#6 – Complement the savings besides the best 401k plan

2. Can You Have 2 401k Plans?

Yes, you can have two 401k plans. Usually, investors have their previous account(s) with the former employer(s) in addition to the latest one. However, possessing multiple plans is risky and certainly not a good idea, so investors must make such investments.

3. Can A Company Have A 401k And a Profit-sharing Plan?

Yes, a company can have a 401k and a profit-sharing plan. Resultantly, this offers the employee some control over the retirement savings amount. The employer can also make excess flexible contributions to the retirement savings.

Recommended Articles

This has been a guide to 401k Plan and its Meaning. Here we explain the 401k plan for small businesses, its types, examples, and withdrawal rules. You can learn more about it from the following articles –