Part of our Retirement Planning guide

Differences Between IRA and 401k

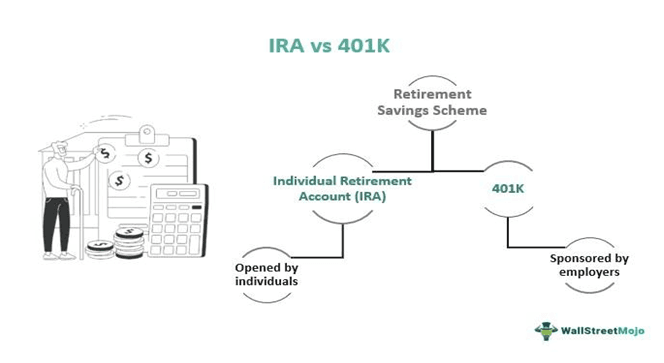

An Individual Retirement Account (IRA) refers to the savings account individuals own to secure their financial position post-retirement. On the other hand, 401K is a retirement savings scheme that employers sponsor for their employees as a loyalty reward for their tenure of service.

Together, they form the most significant retirement savings schemes that individuals can opt for to have a financially secure post-retirement life. However, both these options differ in terms of the investment options they offer and the contribution limits. Though most people think they have to choose between these two post-retirement savings options, they can opt to invest in both schemes simultaneously for a financially healthy life after retirement.

IRA vs 401K – Comparative Table

Let us have a glance at the differences between IRA and 401K retirement schemes:

| Category | IRA | 401K |

|---|---|---|

| Status | Employee-owned | Employer-sponsored |

| Contribution | Within 50 – up to $6,000 At and above 50 – up to $7,000 | Within 50 – up to $20,500 At and above 50 – up to $27,000 |

| Eligibility | Anyone with earned income | Only if employers provide for the scheme |

| Taxation | Federal and state taxes apply to traditional IRAs distributions after 59.5 years of age. | A mandatory federal tax upon withdrawal |

| Choices | Investment choices are more, ranging from stocks, funds, bonds, fixed income investments, and other assets. | Limited investment choices with the freedom to invest in only a few dozen mutual funds. |

| Employer contribution | None as such | Employers normally choose to make a matching contribution based on a portion of the employee’s salary. |

| Suitable for | All those who have earned income | For only those whose employer provides for the option. Also, it is meant for individuals with higher income as the contribution limit is higher. |

What is IRA?

IRA stands for Individual Retirement Accounts, which are opened by individuals themselves, helping them plan their retirement well. It is a tax-deferred investment vehicle that lets individuals keep investing in the scheme without paying any taxes on the savings. Moreover, these tax shelter savings are compounded at a higher interest rate, enabling the planners to acquire more return on their investment.

Any individual having an earned income can open an IRA account with any financial institution, be it a bank, mutual fund, stockbroker, life insurance company, etc. In addition, people filing returns jointly with their partners can open a spousal IRA account, which is applicable even if one has a non-working spouse. People who are yet to turn 50 can invest up to $6,000 in their account, while those who are 50 or above can invest $7,000 as per the latest update.

IRA accounts allow savers to purchase/invest in high-return assets, including CDs, mutual funds, Exchange Traded Funds (ETFs), stocks, bonds, etc.

What is 401K?

401K is a retirement savings scheme that individuals can enjoy only if employers provide for it. Through this savings option, employers recognize the efforts of their loyal employees and let them have a share in the company’s profits. In this investment plan, employees contribute a portion of their wages to individual accounts while employers contribute a significant amount to their accounts from their end as well. As a result, the retirement savings for individuals is a joint effort of the individuals themselves and their employers simultaneously.

In this defined contribution plan the contributions are made through payroll deductions. However, the Internal Revenue Services or IRS has some contribution limits to be followed by individuals. For example, if savers are less than 50-year-old, they can spend up to $20,500 in their 401K account in 2022, whereas if they are 50 or above, the limit increases to $27,000. In addition, the limits for employees from high-income groups may differ to some extent.

IRA vs 401k Infographics

Let’s see the top differences between IRA vs 401k.

IRA vs 401K – The Types

IRA Types

When individuals invest in IRAs, they come across multiple options to choose from. The types of IRA that could be opted for are as follows:

Traditional IRA

It is the option that allows individuals to keep investing in the IRA account without paying any taxes. However, savers have to pay taxes at an ordinary income rate at the time of withdrawal. The amount to be deducted as tax is determined based on the income level of the individuals.

Roth IRA

The type of savings allows individuals to enjoy tax-free returns while withdrawing the amount saved. In short, the contributions are not deductible, but there are income restrictions, which could make the return taxable if exceeded.

Besides the above two broad categories, there are some less popular but significant IRA types that individuals should know about to explore other open alternatives. These include:

- Payroll Deduction – This type of IRA account is set up by the employers, whereby employees contribute through payroll deduction.

- SEP – It stands for Simplified Employee Pension plan where employers directly contribute from their end to an IRA set up of individual employees.

- Simple IRA Plan – It stands for Savings Incentive Match Plan for Employees, a provision for employees from the employer’s side. Under this plan, employees may choose to contribute via salary reduction, and employers may make equal or considerable contributions.

401K Types

People choosing 401K as their savings option for a financially independent retirement life also get many options to invest in. Some of these alternatives include:

Traditional 401K

This retirement savings plan is similar to a traditional IRA scheme. The only difference is that these are employer-sponsored. The employee contributions and earnings, in this case, are tax-free. However, the returns on investment become taxable as soon as they are withdrawn.

Safe Harbor Plan

This is a scheme similar to the traditional 401K plan. However, in this case, when the employer contributions are made, they are fully vested. As a result, the contribution might be equal for all eligible employees or could be based on the elective deferrals they make.

SIMPLE Plans

This retirement savings scheme allows small businesses to have a cost-efficient measure to introduce effective retirement benefits to their employees. In addition, unlike the traditional 401K scheme, this retirement tool is not likely to go through any annual nondiscrimination tests.

Recommended Articles

This is a guide to IRA vs 401k. Here we explain their meanings, types, similarities & major differences using infographics and a comparison table. You may also have a look at the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.