Difference Between Annuity and 401k

Annuity is a life insurance policy that works as an investment plan. A contract is created between a participant and an insurance company in which the participant gives money to the insurance company; in return, the insurance companies make payments per the terms and conditions. In comparison, 401k is a popular tax-deferred retirement savings plan sponsored by employers. Employees are allowed to divert their salary by making the defined contribution.

An annuity is an insurance product, while 401k is a retirement product or plan the employer offers. In this article, we look at the differences between them.

- An annuity is an insurance product wherein installments are periodic. An annuity can be considered a contract between the investor and a party where the investor pays a lump sum amount to the organization and receives the installment once age has reached.

- An annuity gives steady income to investors after they reach retirement age. Annuities also provide death benefits and give the beneficiaries a pre-decided amount in case there is a sudden death of the investor before the end of tenure. An investor can own annuities jointly and bring them with money in the taxable account.

- 401k plan types are among the most popular retirement plans in the US. The employer plans 401k, but the employee contributes. 401k is saving for retirement. The employee deducts a particular amount from the employee’s salary every month and uses this as an investment towards the fund the employee will get after retirement.

- The deduction is tax-deferred. The maximum amount one can contribute is $18,500 per annum, and the amount of tax is deferred until payments are received till retirement.

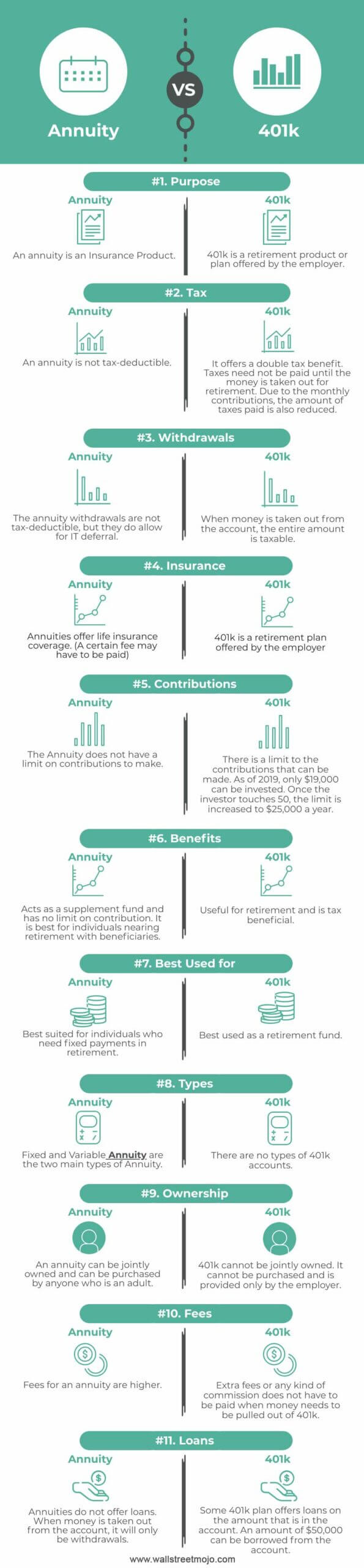

Annuity vs 401k Infographics

Let’s see the top differences between Annuity vs 401k.

Key Differences

- An annuity is not tax-deductible, while a 401k offers a double tax benefit. Taxes need not be paid until the money for retirement. Due to the monthly contributions, the taxes paid also reduce.

- The annuity withdrawals are not tax-deductible but allow for IT deferral. The entire amount is taxable when taken money from the account.

- The annuity does not have a limit on contributions to make. There is a limit to the contributions that one can make. As of 2019, we can only invest $19,000. Once the investor touches 50, the limit is increased to $25,000 a year.

- One can jointly own an annuity, and anyone can purchase who an adult is. One cannot jointly own a 401k. It cannot be purchased and is provided only by the employer.

- Fees for an annuity are higher. Extra fees or commissions must not be paid when money needs to be pulled out of 401k.

- The following are the main types of annuity:

- Fixed Annuities – These types of annuities are not affected by changes in interest rates or market fluctuations and are thus the safest. Types of fixed annuities are Immediate Annuity and Deferred Annuity. In an immediate annuity, the investor receives payments as soon as he makes the first investment. In a deferred annuity, the money is accumulated for a predetermined period before the payments begin.

- Variable Annuities – These types of annuities are not affected by changes in interest rates or market fluctuations and are thus the safest. Types of fixed annuities are Immediate Annuity and Deferred Annuity. In an immediate annuity, the investor receives payments as soon as he makes the first investment. In a deferred annuity, the money is accumulated for a predetermined period before the payments begin.

- There are no particular types of 401k accounts.

Annuity vs 401k Comparative Table

| Basis | Annuity | 401k |

|---|---|---|

| Purpose | An annuity is an insurance product. | 401k is a retirement product or plan offered by the employer |

| Tax | An annuity is not tax-deductible. | It offers a double tax benefit. Taxes need not be paid until the money is taken out for retirement. Due to the monthly contributions, the taxes paid are also reduced. |

| Withdrawals | Annuity withdrawals are not tax-deductible but allow for IT deferral. | The entire amount is taxable when money is taken out from the account. |

| Insurance | Annuities offer life insurance coverage. (A certain fee may have to be paid) | 401k is a retirement plan offered by the employer |

| Contributions | The annuity does not have a limit on contributions to make | There is a limit to the contributions that can be made. As of 2019, only $19,000 can be invested. Once the investor touches 50, the limit is increased to $25,000 a year. |

| Benefits | Acts as a supplement fund and has no limit on contribution. It is best for individuals nearing retirement with beneficiaries. | Useful for retirement and is tax beneficial. |

| Best Used for | Best suited for individuals who need fixed payments in retirement. | Best used as a retirement fund. |

| Types | Fixed and Variable Annuity are the two main types of Annuity. | There are no types of 401k accounts. |

| Ownership | An annuity can be jointly owned and can be purchased by anyone who is an adult. | 401k cannot be jointly owned. It cannot be purchased and is provided only by the employer. |

| Fees | Fees for an annuity are higher. | Extra fees or commissions must not be paid when money needs to be pulled out of 401k. |

| Loans | Annuities do not offer loans. When money is taken out from the account, one will only withdraw it. | Some 401k plans offer loans on the amount that is in the account. For example, $50,000 can be borrowed from the account. |

Conclusion

Both Annuity and 401k provide sound retirement plans if managed properly. The Annuity has a large number of options, while there are no options in 401k accounts. The main difference between these two schemes lies in the contribution limit amount. Contributions in 401k are restricted with limited funds, while the Annuity is not affected by such limitations.

Both these products provide the chance to increase and grow your investment on a tax-deferred basis. An important point to note is that these investments are not mutually exclusive, and an investor can invest in both these products if he wishes to. However, there is no reason why an individual should opt for both, especially if they have exhausted the tax-advantaged accounts.

Recommended Articles

This article is a guide to Annuity vs. 401k. Here we discuss the top differences between Annuity and 401k, infographics, and a comparison table. You may also have a look at the following articles: –