Part of our Audit Procedures and Techniques guide

What is Audit Evidence?

The Audit Evidence is the information that the company’s auditor collects from the company. It is part of auditing work to review and verify the company’s different financial transactions, internal control, and other requirements to express his opinion on the objective and unbiased view of the company’s financial statements during the period under consideration.

Reliable evidence enhances the credibility of financial reporting and supports the assurance process, instilling confidence in stakeholders. Despite its importance, audit evidence procedure has limitations. Factors like inherent biases, potential management manipulation, and the evolving nature of business risks can impact the effectiveness of evidence, potentially leading to incomplete or inaccurate audit assessments.

Audit Evidence Explained

Audit Evidence is the vital information that the auditor appointed by the company collects as part of its auditing work to express their opinion on the financial statements of the company during the period under consideration, i.e., whether the financial statements of the company present the right and fair picture or not.

To establish audit evidence sources, auditors employ a variety of procedures, such as inspection, observation, inquiry, and confirmation. Inspection involves examining documents, records, and tangible assets, providing tangible proof of financial transactions. Observation allows auditors to witness certain processes or activities, enhancing their understanding of internal controls. Inquiry involves seeking information from management or employees, helping auditors gain insights into the entity’s operations.

Furthermore, auditors often use external confirmation to verify the accuracy of certain financial information. This may involve contacting third parties, such as banks or suppliers, to corroborate the details presented in the financial statements. These procedures collectively contribute to the creation of a credible audit trail.

The importance of sufficient and appropriate audit evidence cannot be overstated, as it forms the basis for auditors’ conclusions about the fairness of financial statements. It provides stakeholders, including investors and regulators, with assurance regarding the reliability of reported financial information. Therefore, audit evidence is like the backbone of the auditing process, reinforcing the credibility and integrity of financial reporting in the dynamic landscape of finance.

Characteristics

Let us understand the characteristics of the concept through the discussion below.

- Audit evidence must be directly related to the financial statement assertions being tested, ensuring its significance in supporting the auditor’s conclusions.

- The reliability of evidence is crucial, with more reliable sources, such as external documents or third-party confirmations, carrying greater weight in the audit process.

- The consistency of evidence across different sources and periods enhances its credibility and contributes to a more comprehensive understanding of financial transactions.

- Auditors strive for complete evidence coverage to minimize the risk of overlooking material misstatements, ensuring a thorough and accurate evaluation of financial statements.

- Evidence should be genuine and unaltered, confirming the legitimacy of financial transactions and reinforcing the overall reliability of the audit process.

- Audit evidence should be sufficient in quantity and quality to support the auditor’s conclusions, providing a robust foundation for the expressed opinion on the financial statements.

- The timely availability of reliable audit evidence sources is crucial for an effective and efficient audit, allowing auditors to address issues promptly and meet reporting deadlines.

Types

Let us understand the different types of audit evidence procedures followed by auditors through the explanation below.

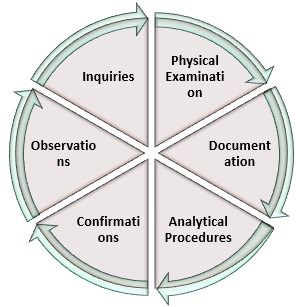

#1 – Physical Examination

Physical examination is where the audit inspects the asset and counts them whenever required. This evidence is collected wherever possible based on the nature of the audit.

#2 – Documentation

Under the documentation, the auditor collects written documents like purchase invoices, sales invoices, policy documents of the company, etc., which can be internal or external. This evidence is more reliable as there is some proof in writing based on which the auditor is forming his opinion.

#3 – Analytical Procedures

Auditor uses the analytical procedure to derive the required data or know the correctness of different information. It includes the usage of the comparisons, calculations, and the relationships between the various data by the auditor.

#4 – Confirmations

The auditors often require the balance confirmations from the third party to ensure that the clients do not manipulate the balances reflected in the financial statements. This receipt of the written response directly from the third party to verify the accuracy and authenticity of different information required by the auditor.

#5 – Observations

Observation is where the auditor of the company observes the various activities of the clients and their employees before making any conclusion.

#6 – Inquiries

Inquiries are the different questions asked by the company’s auditor to the company’s management or concerned employee in the areas where the auditor has doubts. The auditor obtains the answers to these questions.

If you want to learn more about Auditing, you may also consider taking courses offered by Coursera –

Examples

Now that we understand the concept’s basics and intricacies, let us also understand its practicality through the examples below.

Example #1

The company Y ltd appoints M/s B as the company’s auditor for auditing the company’s financial statements for the fiscal year 2018-19. The auditor asks for the written confirmation of the balances from the customers as selected by them to ensure that the balances reflected in the financial statements are correct.

Receiving the written response directly from the third party is required to verify the accuracy and authenticity of various information needed by the auditor. It forms part of the audit evidence of the auditor’s work. In the above case, the auditor asks for the written confirmation of the balances from the customers as selected by them to ensure that the balances reflected in the financial statements are correct. So, these written confirmations are an example of audit evidence.

Example #2

The National Financial Reporting Authority (NFRA) in India imposed fines totaling Rs 2.15 crore on three entities, including two auditors, and barred them for varying periods due to shortcomings in the audit of Coffee Day Global Ltd for the fiscal year 2019-20. Coffee Day Global Ltd (CDGL) and MACEL operate as subsidiaries of the publicly listed entity Coffee Day Enterprises Ltd (CDEL).

The regulatory action stemmed from the auditors’ failure to obtain adequate and relevant audit evidence during the examination of deferred tax assets, leading to a misstatement of Rs 244 crore. Additionally, discrepancies amounting to Rs 26.19 crore in related party disclosure, specifically pertaining to the procurement of coffee beans from MACEL, were identified. Notably, these lapses resulted in total material and pervasive misstatements of Rs 1,615.04 crore for CDGL, which were not identified or reported in the independent auditor’s report.

Importance

Let us understand the importance of audit evidence sources through the points below.

- Audit evidence is essential for establishing the credibility and reliability of financial statements and instilling confidence among stakeholders.

- Stakeholders rely on audit evidence to make well-informed decisions regarding investments, loans, and other financial engagements.

- Proper audit evidence ensures adherence to regulatory standards and financial reporting frameworks, safeguarding against legal and compliance issues.

- A thorough examination of evidence helps identify and mitigate the risk of material misstatements, enhancing the accuracy and integrity of financial reporting.

- Transparent and well-supported financial statements, backed by robust audit evidence, foster trust and confidence among investors, contributing to a healthy financial ecosystem.

Advantages

The advantages of audit evidence procedures are as follows:

- It helps ensure the auditor’s accuracy and authenticity of the information furnished to him by his client.

- It forms the basis on which the auditor of the company expresses his opinion on the company’s financial statements during the period under consideration, i.e., whether the company’s financial statements present the right and fair picture or not.

Disadvantages

Despite the various advantages, the disadvantages of audit evidence sources are as follows:

- Sometimes the information obtained as the audit evidence, mainly derived from the internal sources, is manipulated by the clients. If the auditors rely on that information, it will express the wrong audit opinion on the company’s financial statements.

- If the data size is enormous, then the auditor generally considers the material things only as his sample for verification of the data and not the whole of the data. If the data having the problem are left out by the auditor in his sample, it will not present the correct picture of the company.

Recommended Articles

This article has been a guide to what is Audit Evidence. Here we explain its types, characteristics, examples, importance, advantages, and disadvantages. You can learn more about auditing from the following articles-