Part of our Types of Audit guide

Forensic Audit Meaning

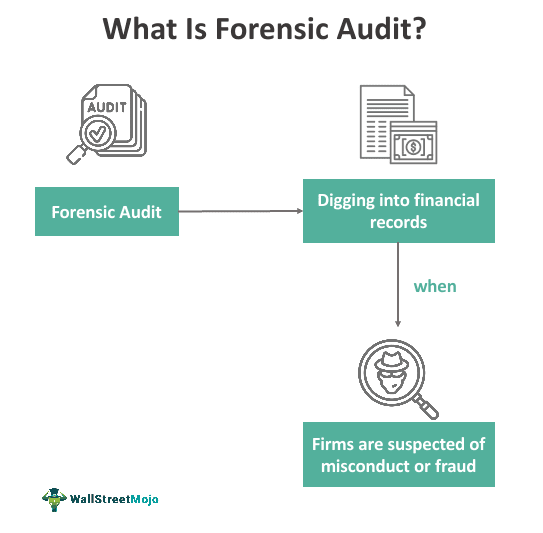

A forensic audit is a structured examination of the financial records of a business entity in an investigative manner to find out the evidence that can be used for legal proceedings in court. It is one step ahead of an internal audit, and the person who conducts such an audit should know the law and legal frameworks and have expert knowledge of accounting and auditing.

A forensic audit is only conducted when there is something suspicious about a firm or organization. The government or administrative authorities conduct these audits to detect the fraudulent activities, malpractices or misconducts happening with an organization. If any negative activity is detected, the investigation continues for evidence and legal proceedings begin.

- A forensic audit is a structured examination of the company’s financial records analytically to get the proof to be used for legal proceedings in court.

- The person performing such an audit must understand the law and legal frameworks and possess knowledge of accounting and auditing.

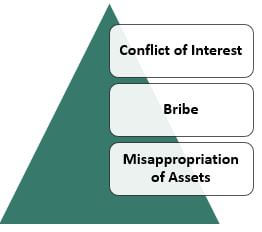

- Conflict of interest, bribes, misappropriation of assets, and misrepresentation of financial statements are the reasons for doing the forensic audit.

- The steps of a forensic audit are planning the investigation, collecting evidence, reporting, and court proceedings.

Forensic Audit Explained

A forensic audit is required for a specific purpose like finding the fraud or misrepresenting a financial statement by examining the past transaction and collecting evidence that will prove that some fraud has happened and can be used in court for legal proceedings. At the same time, internal audit is focused on compliance, policies, accounting standards, and other controls that companies need to follow for their operation.

Forensic audit has multiple purposes to serve when it comes to ensuring accurate and reliable maintenance of records in the financial statements. Some of the objectives of this process are as follows:

- Identifying the cases of fraud through different investigation methods and taking care of them.

- Ensuring prevention of frauds by implementing internal controls besides the advice and recommendations from authorities.

- The participation of auditors in the development of fraud prevention programs.

- Investigation of required matters and collection of evidence for the legal or judicial proceedings.

Types

Based on the type of frauds and issues that occur in a business setup, the type of forensic audit reports may differ. However, such audits are broadly classified into two categories – financial statement audit and financial due diligence audit.

- Financial Statement Audit: It checks for accuracy in the financial statements that companies prepare. The main focus is on te footnote disclosures that mentions the risk management factors besides others. The auditor, in this case, also ensures the statements prepared comply with the guidelines specified by financial regulatory bodies.

- Financial Due Diligence Audit: It is different from standard auditing techniques as it goes beyond considering the financial statements only. Instead, it focuses on acquiring evidence that could help decide whether a business is fit to be bought or sold or should one invest in it for it to operate further.

Checklist

There are four steps followed for a standard forensic audit procedures:

- Planning the investigation

- Collecting evidence

- Reporting

- Court Proceedings

#1 – Planning the Investigation

Auditors will plan the investigation to leave nothing out and achieve the audit’s objective. Below are some points which auditors keep in mind:

- Identifying the fraud being carried out

- The period during which fraud has been carried out

- Reason or root cause of fraud

- Find out employees involved in the fraud

- The loss suffered by the company because of the fraud, whether it is financial or non-financial

- Establishing evidence collection by copying in court proceedings.

- Suggesting actions for preventing these types of frauds in future

#2 – Collecting Evidence

It is an essential part of forensic audits. After identifying the fraud, the auditor will collect the evidence, which can be substantiated and accepted in court. These documents must reflect how the fraud has happened, who has done it, and what amount of loss the company has suffered.

For example, a vendor has finalized the purchase of raw material. If it suspects that some malicious things happened in that finalization, the auditor will examine the below things:

- Who has approved the vendor

- Whether company policy was followed at the time of finalizing

- Quotation from other 3-4 vendors has been taken or not

- If taken, whether all these quotations were compared with each other in terms of pricing and quality

- After finalizing, whether the vendor provided the same quality of material, which it has shown at the time of selection

#3 – Reporting

After completing the above process, a forensic auditor will prepare a report summarizing the audit and present it to the management/client. The report contains the below points:

- Observation/findings during the audit

- Evidence gathered which will substantiate the fraud

- How much loss the company has suffered

- How the fraud has been conducted

- What steps should be taken to stop this type of fraud

Based on the report, the management can decide whether they should go for legal proceedings or not.

#4 – Court Proceedings

Suppose management decides to take legal action based on the forensic audit report. In that case, the auditor should also be present at the court to explain how the fraud has been done and how the evidence will support the statement. The forensic auditor will also simplify the accounting fraud in simple language so that everyone can understand it.

Examples

Let us consider the following instances to understand what is forensic audit and how it is conducted:

Example #1

Suppose Firm ABC belonging to the environmental sector obtained funds from the government in the name of initiating campaigns to spread awareness about preservation of ecological resources. The company, as per its proposal, stated its willingness to visit every corner of Nevada.

To achieve the purpose, it took the required funds from the government. However, it was found that it did not spend anything on the campaign. Thus, the authorities ordered to conduct forensic auditing where the auditors investigated the matter, and found the firm ABC guilty of misusing the funds obtained in the name of doing good for the environment.

The auditor and team gathered the evidence to prove their point, thereby making the guilty pay for the misdeed.

Example #2

In August 2023, a new revelation was made about the central bank of Lebanon as a result of the forensic audit conducted against it by a New York firm Alvarez & Marsal. The latest report unveiled the former governor Riad Salameh’s misconducts and illegitimate commissions worth approximately $111 million.

The audit was conducted per the orders received from the International Monetary Fund following the deteriorating status of the country.

Importance

The forensic audit importance can be derived from the scenarios that become the reasons for it to be carried out. Some of the instances that make it necessary for such audits to be conducted are as follows:

#1 – Deal With Conflict of Interest

When an employee misuses their position for personal gains and causes the company to incur a loss, a forensic audit comes into the picture.

For instance, a manager approving an employee’s excess/unwanted expenses due to personal relations will get some leverage over the employee on a personal level. However, in this case, the manager will not benefit financially from this activity.

#2 – Identify Bribery

An organization offering money or giving expensive gifts to get things done or making the situation in its favor is a bribe.

For example, the head of the purchasing department approves purchases from a vendor that will supply the material at a higher cost or cost less than other vendors. Although the quality of the product is not good, the head is getting some personal compensation from that vendor.

#3 – Identify Misappropriation of Assets

It is the most prevalent type of fraud where employees misuse the company’s assets for their benefit.

For example, an employee submitting a fake bill for using the company stationery or showing the damaged or expired inventory (primarily in FMCG companies) and receiving funds.

#4 – Detect Misrepresentation of Financial Statement

This type of fraud generally happens at a higher level of the company by showing better business performance against the actual performance. Thus, investors will not hesitate to invest in the company, and lenders can easily offer loans at lower interest rates. Top management will also benefit by getting bonuses or incentives based on the company’s performance. Misrepresentation can be done by showing less provision against accrued expenses or debtors, hiding any contingent liability, and not giving the proper disclosure about the information which can influence investors or lenders.

Advantages and Disadvantages

Conducting forensic audit has its own set of advantages and disadvantages. Let us have a look at a few of them in tabular form:

| Advantages | Disadvantages |

| It helps identify financial crimes and deal with them. | It is a time consuming process. |

| It monitors the professionals to check if the tampering with the statements was intentionally done. | Disruption of normal business activities. |

| It simply checks the financial records to ensure accuracy. | It is the best when conducted by experts. |

| It also helps in conducting complete investigation and gather evidence for further legal proceedings in severely serious matters. | Organizations may resist the change and do not accept the findings that easily in all cases. |

Forensic Audit vs Financial Audit

Forensic and financial audits are two types of audits that are conducted to ensure businesses maintain accurate and reliable records. However, there are a few aspects in which they differ.

Let us have a look at some of those aspects of both the terms together below:

- Financial audits are quite a normal phenomenon in any company and are conducted mostly annually or anytime before as and when required. On the contrary, forensic audits are conducted only when some fraudulent activities are suspected in an organization.

- A financial audit report is used by the management and stakeholders of the businesses to be aware of the current financial position of the firm so that the management can decide on improvement of strategies and investors can decide whether to invest in its assets. On the other hand, a forensic audit report enables firms or authorities at the central level find out about the malpractices or frauds happening inside an organization.

Forensic Audit vs Internal Audit

Forensic audit and internal audit are quite familiar terms for those in the corporate world. However, there are individuals and entities that may not be aware of the basic differences between the two.

Listed below are some of the differences between the two for them to have a look at:

- A forensic audit is done to find the fraud that happened in the company, whereas an internal audit is done to find the lapse in accounting or company policies.

- Forensic auditors must have expert knowledge of the law, whereas this is not compulsory for internal auditors.

- Forensic audits can be used for legal proceedings, whereas evidence gathered in an internal audit will not be acceptable in legal proceedings.

- A forensic audit is required when there is suspicion that an employee has intentionally committed fraud for personal gain. In contrast, an internal audit is done regularly to check whether all accounting policies and accounting standards have been followed, but mistakes have not been made.

Frequently Asked Questions (FAQs)

How long does a forensic audit take?

Commonly, the hours from the start of the investigation to the final issuance is approximately 50 – 70 hours. However, if it involves more than one year, then the additional years will take about 30 – 40 hours per extra year.

What is forensic audit in banks?

A bank forensic audit is a firm’s or individual’s financial records examination and evaluation. In a forensic audit, an auditor needs proof to produce in court. In addition, one may also use it to discover criminal behavior like fraud or embezzlement.

Why is it necessary to have a forensic audit?

A forensic audit is generally conducted to bring action against a party in court for fraud, embezzlement, or other financial crimes. In the forensic audit procedure, the auditor may be approached to work as an expert witness during the trial proceedings.

Is forensic audit mandatory?

A forensic audit is crucial in evaluating and examining an individual’s or a firm’s financial records to get proof that can be used in a legal proceeding or court of law.

Recommended Articles

This article has been a guide to Forensic Audit & its meaning. We explain its checklist, importance, examples, types, vs financial & internal audit, advantages and disadvanatages. You may learn more about financing from the following articles –