Part of our Types of Audit guide

What Is Financial Statement Audit?

A financial statement audit is defined as an independent examination of the company’s financial statement and its disclosures by auditors. It provides a true and fair view of its financial performance. The auditor ensures that the statements are in accordance with the framework of filing after a thorough check of the statements of the company.

The balance sheet, income statement, statement of retained earnings, and cash flow statement are the four major parts of the financial statement audit process. These statements are scrutinized to ensure no material errors are made and are in compliance with filing regulations. Only a Certified Public Accountant (CPA) can audit these statements and deem them fit for filing.

Key Takeaways

- Financial statement audit meaning refers to an examination of an organization’s financial statements, like the balance sheet, carried out by professionals called auditors.

- Financial statement audit meaning refers to an examination of an organization’s financial statements, like the balance sheet, carried out by professionals called auditors.

- A key benefit of such 0061n audit is that it helps ensure consistency in companies’ financial reporting. Moreover, it gives assurance to investors.

- A key limitation of this process is that auditors are not able to gain absolute assurance regarding the material correctness of the financial statements.

Financial Statement Audit Explained

The financial statement audit meaning refers to the process of scrutinizing the important statement of a company such as the income statement, cash flow statement, and balance sheet to ensure they are free from material errors and are fit according to the filing regulations or framework.

Let us understand the most important documents an auditor scrutinizes before submitting their financial statement audit report.

- Income Statement: This is the statement of a company’s financial performance over a specific accounting period. It shows revenue, expenses incurred through operating and non-operating activities,es and net profit or loss incurred during this period.

- Balance Sheet: This is a statement of the company’s financial position at a specific point in time. It is done by detailing the assets, liabilities, and shareholders’ equity to give an idea of what the company owns along with the liabilities. The balance sheet is prepared based on the idea that Assets = Liabilities + Shareholders’ Equity.

- Cash Flow Statement: This is a statement of the company’s cash and cash equivalents during a specific accounting period

These financial statements are the ones often utilized for audit purposes. However, some adjustments might be made to the statements by the company after the finalization of the audit for a better representation of facts in the financial statement audit report.

Before diving deep into the concept of financial statement audit, individuals need to have a clear understanding of financial statements. If one does not have knowledge of the same, they can take this Financial Planning & Analysis course. This expert-led course aims to help learners develop a practical understanding of financial statements, ratio analysis, financial modeling, capital budgeting, and related concepts via different examples.

Video Explanations of Financial Statement Audit

Principles

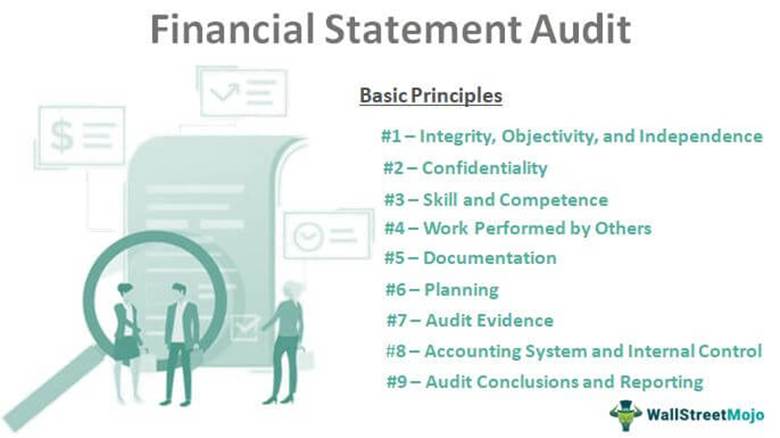

Below are some of the basic principles governing a financial statement audit process.

- Integrity, Objectivity, and Independence – The auditor should be straightforward, honest, and sincere in his professional work. He should be fair and must not be biased.

- Confidentiality – He should maintain the confidentiality of information acquired during his work and not disclose any such information to a third party.

- Skill and Competence – He should perform work with due professional care. The audit should be performed by persons having adequate training, experience, and competence.

- Work Performed by Others – The auditor can delegate work to assistants or use work performed by other auditors and experts. But he will continue to be responsible for his opinion on financial information.

- Documentation – He should document matters relating to the audit as the financial statement audit checklist.

- Planning – He should plan his work to conduct an audit effectively and timely. Plans should be based on knowledge of the client’s business.

- Audit Evidence – The auditor should obtain sufficient and appropriate audit evidence by performing compliance and substantive procedures. Evidence enables the auditor to draw reasonable conclusions.

- Accounting System and Internal Control – Internal control system ensures that the accounting system is adequate and that all the accounting information has been duly recorded. The auditor should understand the management’s accounting system and related internal controls.

- Audit Conclusions and Reporting – The auditor should review and assess the conclusions drawn from the audit evidence obtained through the performance of procedures. The audit report should contain a clear written expression of opinion on the financial statements.

Objectives

Let us understand the objectives of a financial statement audit report being prepared by every organization through the discussion below.

- The objective of a financial statement audit is to enable the auditor to express an opinion on financial statements. The entity’s management prepares an audit.

- It is essential that financial statements are prepared as per the recognized accounting policies and practice and relevant statutory requirements, and they should disclose all material matters.

- However, his opinion does not constitute an assurance as to the future viability of the enterprise or the efficiency or effectiveness with which its management has conducted the enterprise’s affairs.

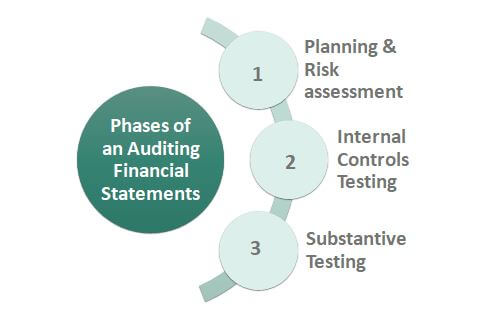

Phases

Let us understand the different steps in the financial statement audit process through the detailed explanation below.

#1 – Planning & Risk assessment

The initial stage of financial statement audit checklist involves putting together an audit team and laying down general guidelines for effectively carrying out an audit. The next step is to determine any risks that could lead to material errors in the statements. Identifying such risks requires the auditor to have a thorough knowledge of the industry and business environment in which the company operates.

#2 – Internal Controls Testing

This stage involves a critical analysis of internal controls adopted by a company and their level of efficacy in eliminating any possibility of material misstatements in financial statements. These internal controls could include automated systems and processes employed by a company to ensure higher operational efficiency, safeguard assets, and ensure that all transactions are accurately reported.

#3 – Substantive Testing

At this stage, the auditor looks for substantial evidence and cross-verification of facts and figures reported in the statements, which might include the following:

- Physical inspection of assets, if required.

- Cross-checking recorded figures in statements against actual documents and records with the company;

- Third-party or any external confirmations of financial transactions and their details reported by the company; This often includes an independent verification of such statements from the banks and any commercial entities a company is engaged in business with.

Financial Statement Audit Opinions

There are 4 main types of opinion reports, which are letters reflecting the auditor’s opinion. Let us look at them.

- Unqualified Opinion: This is a clean report without any adverse comments. Moreover, such reports do not come with any disclaimer regarding the audit or any clause.

- Qualified Opinion: It indicates that an auditor does not have confidence regarding a particular transaction or process. They do not issue a clean report because of this lack of confidence. Auditors outline the reasons why they cannot provide an unqualified opinion.

- Adverse Opinion: Suppose an auditor finds an organization’s financial statements are materially incorrect or the statements are not in line with GAAP. In that case, they give an adverse opinion and state the reason for issuing the same.

- Disclaimer Of Opinion: This means that the auditor does not wish to express any opinion regarding the company’s financial statements. This happens when the auditor is unable to figure out if the financial statements of the business are materially accurate.

Examples

Let us try to understand the concept of financial statement audit opinions with the help of examples.

Example #1

Let us assume ABC Ltd is a furniture manufacturing company which has engaged an audit firm for the financial audit purpose. So initially the auditor will the objective and scope of the procedure for that organization. They will try to identify the main risk areas and timeline of the audit and gather information about the company operation and accounting and reporting system.

Then they will try to find any kind of misstatement or incomplete transactions which are not satisfactory. For this purpose they may pick up samples of transactions and check them thoroughly for completeness and accuracy.

They also compare the data with current and past data, industry benchmarks or other relevant information to identify unusual trends. They will also interact with third parties like customers, suppliers, lenders, for information and consider management decisions and suggestions regarding any issue.

Finally, they will create a report and give their opinion regarding the true and fair view about the financial condition of the business. This report is valuable for management, and all other stakeholders.

Example #2

According to a report published on April 24, 2025, Axis Bank Limited disclosed its financial statements for the financial year ended March 31, 2025, following a financial statement audit. The organization’s statutory auditors presented an unmodified (unqualified) opinion, indicating that its financial statements present an accurate and fair view of the financial performance and position.

Responsibility

Preparing a fool proof report requires the management to carry out a certain standard of record keeping and consistency throughout the year. Let us understand their responsibilities towards ensuring an up to data financial statement audit report.

- The management is responsible for maintaining an up-to-date and proper accounting system and preparing financial statements.

- The auditor is responsible for forming and expressing opinions on the financial statements.

- The financial statement audit does not relieve the management of its responsibility.

Scope

The auditor decides the scope of his audit and the financial statement audit opinions having regard to;

- The requirement of the relevant legislation

- The pronouncements of the institute

- Terms of engagement

However, the terms of engagement cannot supersede the pronouncement of the institute or the provisions of relevant legislation.

Benefits

Let us discuss the importance of such a detailed and a tedious process that companies conduct every single year through the points below.

- Enhances Qualification of Business Process – A rigorous audit process may also identify areas where management may improve their controls or processes, further adding value to the company by enhancing the quality of its business processes.

- Assurance to Investors – An audited financial statement provides a high, but not absolute, assurance that the amounts included in the company’s financial statements and notes to accounts (disclosures) are free from any material misstatement.

- True and Fair View – An unqualified (“clean”) audit report provides the user with an audit opinion, stating that financial statements show a true and fair view in all material aspects and are by generally accepted accounting principles.

- Provides Consistency – Financial statements Audit provides a level of consistency in financial reporting that users of the financial statements can rely on when analyzing different companies and decision-making.

Limitations

The limitations of the financial statement audit process are as discussed below.

- The auditor cannot obtain absolute assurance.

- It is due to the inherent limitations of an audit due to which the auditor obtains persuasive evidence rather than conclusive.

- It arises from the Nature of financial reporting, audit procedures, and Limitations concerning time and cost.

Due to aforesaid inherent limitations, there is an unavoidable risk that some material misstatements may remain undetected.

Financial Statement Audit Vs Integrated Audit

Both the above concepts are related to external audit procedures done by auditors. However, there are some differences between them as follows:

- The auditor of the former has the responsibility of identifying areas of misstatement or incompleteness of financial statements and find the reasons behind them, whereas the latter goes beyond financial statements and looks into auditing of the company’s internal control system also.

- The former verifies whether the financial statements are reported as per the financial standards, which is GAAP or IFRS. But the latter checks the efficiency and effectiveness of the internal control system.

- The former involves checking the income statement, balance sheet, cash flow statement and statement of changes in equity for any misstatement or fraud in the same but the latter concentrates on the type, design and operation of the company and evaluates the procedures for reliability.

- The report produced by the auditor in case of the former presents the fairness of the financial statements and identify the misstatements, whereas the latter produces report regarding the strength and weakness of the internal controls.

Thus, what kind of audit is required depends on the company the type of industry or products they deal with, the regulator requirements, competition, risk profile, etc. But both are equally important in the financial market.

Frequently Asked Questions (FAQs)

What are the three types of financial statement audits?

These audits are of three types, and they are as follows:

- Internal audit: Employees within the organization who are called internal auditors conduct the audit.

- External Audit: In this case, employees of an independent organization carry out the audit.

- Internal Revenue Service or IRS Audit: Auditors of the IRS conduct the audit of a company’s financial statements to determine the material accuracy.

Is there any framework for financial statement audit?

Yes, auditors must follow the Generally Accepted Auditing Standards, or GAAS, when conducting the audit of an organization’s financial statements. GAAS comprises the rules and regulations that must be followed to ensure that auditors carry out the process with utmost professionalism. Simply put, GAAS comprises principles governing the process of auditing.

How often should a financial statement audit be carried out?

Typically, the Securities and Exchange Commission requires the audit of a company’s financial statements on an annual basis. That said, this requirement may vary based on the rules and regulations applicable to companies worldwide.

How to obtain favorable financial statement audit opinions?

One can take these measures to apply the same:

- Execute internal controls

- Formulate strong policies

- Conduct reviews regularly

Recommended Articles

This article has been a guide to what is Financial Statement Audit. We explain it with example, objectives, benefits, differences with integrated audit & principles. You may learn more about basic accounting from the following articles –