What Is The Audit Risk Model?

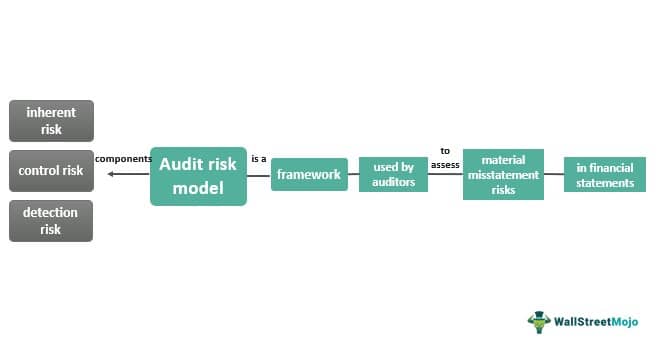

The audit risk model is a framework auditors use to assess the risk of material misstatement in a company’s financial statements. The model has based on the premise that all audits involve some level of risk and that auditors must take steps to manage that risk. It’s purpose is to help auditors assess risks.

It is vital as the auditors must evaluate components and determine an appropriate level of audit procedures. It helps to mitigate the overall audit risk to an acceptable level. The auditor may also adjust the level of inherent and control risk assessments. By using the audit risk model, auditors can effectively plan and execute their audits. In addition, it ensures the reliability of the financial statements.

- The audit risk model is based on the interrelationships between inherent risk, control risk, and detection risk, which are all critical factors in determining the level of audit risk.

- The inherent risk factor, which represents the level of risk associated with the nature of the business and industry in which it operates, is a key element of the audit risk model.

- The audit risk model has certain limitations, including subjectivity, limited scope, and the risk of incomplete information, which auditors must be aware of when using this tool.

Audit Risk Model Explained

The audit risk model is a framework auditors use to assess the risk of material misstatement in a company’s financial statements. The model comprises three components: inherent risk, control risk, and detection risk. Inherent risk is the risk that a material misstatement exists, control risk is the risk that a material misstatement will not be prevented or detected by internal controls, and detection risk is the risk that the auditor will not detect a material misstatement.

The auditor evaluates each component and determines appropriate audit procedures to mitigate overall risk. By using the audit risk model, auditors can plan and execute their audits effectively and ensure the reliability of financial statements.

Components

The audit risk model is made up of three components:

#1 – Inherent Risk

This is the risk of a material misstatement in the financial statements, regardless of any controls. It is influenced by factors such as the nature of the company’s business, the complexity of transactions, and financial reporting history.

#2 – Control Risk

This is the risk that a material misstatement will not be prevented or detected by a company’s internal controls. Instead, it is influenced by the design and effectiveness of the company’s control environment, including the tone at the top, control activities, and monitoring.

#3 – Detection Risk

This is the risk that the auditor will not detect a material misstatement, even if it exists. It is influenced by the nature, timing, and extent of audit procedures the auditor performs.

The auditor must assess each component to determine an appropriate level of audit risk and design and execute audit procedures that address the identified risks. The ultimate goal is to obtain sufficient and appropriate audit evidence to support the auditor’s opinion on the fairness of the financial statements.

Formula

The audit risk model can be expressed mathematically as follows:

Audit Risk = Inherent Risk x Control Risk x Detection Risk

This formula shows that the overall level of audit risk is a product of the individual risk components. Therefore, the auditor must assess each component and determine an appropriate level of audit procedures to reduce the risk to an acceptable level.

For example, suppose the inherent and control risks are assessed as high. In that case, the auditor may need to perform more extensive audit procedures. As a result, it reduces detection risk and achieves an acceptable overall audit risk. Conversely, if inherent and control risks are assessed as low, the auditor may be able to perform less extensive audit procedures, resulting in a lower overall audit risk.

By using this formula, auditors can evaluate the risk associated with an audit engagement and design a plan to perform audit procedures commensurate with the identified risk level.

Examples

Let us look at the following examples to understand the concept better.

Examples #1

Let’s say an auditor is conducting an audit of a manufacturing company. The auditor first assesses the inherent risk, which is high due to the complex and volatile nature of the industry, as well as the company’s history of noncompliance with regulations.

The auditor then assesses the control risk, which is moderate due to the company’s implementation of effective internal controls and procedures, such as regular employee training, quality control checks, and documentation practices.

Finally, the auditor assesses the detection risk, which is low due to the use of a comprehensive audit plan, including sampling and testing of the company’s financial records and reports, as well as the experience and expertise of the audit team.

Based on these assessments, the auditor concludes that the overall audit risk is high. He then develops an appropriate audit plan to address the identified risks. For example, this might include additional testing of high-risk areas. In addition, it may include inventory or revenue recognition and ongoing communication and collaboration with company management to ensure the audit is conducted effectively and efficiently.

Example #2

Let’s consider a company called Charismatic Electronics Inc. that manufactures and sells electronic devices. The company has been in business for five years and has recently expanded its operations to several new markets. It has experienced rapid growth in recent years and has a diverse range of products.

For Charismatic Electronics Inc., the inherent risk could be considered moderate to high. This is because the company operates in a rapidly evolving and competitive industry. As a result, there are inherent risks related to product obsolescence, technology changes, and remaining competitive. Additionally, the company’s recent expansion into new markets and diverse product portfolio may increase the inherent risk.

Importance

The audit risk model is an important concept in auditing, as it provides a framework for auditors to assess the risks associated with a particular audit engagement. For example, the model helps auditors identify and evaluate the risk of material misstatement. It is the risk that the financial statements are materially incorrect or misleading.

The importance of the audit risk model can be understood from the following perspectives:

- Helps to plan the audit: The audit risk model provides a structured approach for auditors to plan the audit engagement. By assessing the risk of material misstatement, auditors can identify the areas of the financial statements. Some require more attention and resources during the audit process.

- Enhances audit quality: Using the audit risk model can help auditors enhance the quality of their audit work. Assessing the risk of material misstatement and developing appropriate audit procedures are done. Thus, auditors can provide more reliable and relevant information to the users of financial statements.

- Assists in making audit judgments: The audit risk model helps auditors to make informed judgments. They consider the nature, timing, and extent of audit procedures that need to be performed. By identifying the areas of the financial statements at higher risk of material misstatement, auditors can focus their audit efforts on those areas.

- Facilitates communication with stakeholders: The use of the audit risk model can help auditors to communicate with stakeholders, such as management, audit committees, and regulators. By explaining the audit risk model and the audit procedures that have been performed, auditors can provide stakeholders with a better understanding of the audit process, and the conclusions reached.

Limitations

While the audit risk model provides a structured approach for auditors to assess the risks associated with a particular audit engagement, its application has certain limitations. Some of the limitations of the audit risk model are:

- Subjectivity: The audit risk model involves a degree of subjectivity. Auditors must make judgments and estimates about the risks associated with the audit engagement. This can lead to risk assessment variations, particularly when the risks are difficult to quantify or evaluate.

- Limited scope: The audit risk model is limited. It only considers the risks associated with material misstatement in the financial statements. It does not address other risks relevant to the business, such as operational, strategic, or reputational risks.

- Incomplete information: The audit risk model relies on the information available to the auditor during the audit. Incomplete or inaccurate information can lead to incorrect risk assessments and failure to detect material misstatements in financial statements.

- Fraud risk: The audit risk model may not adequately address the risk of fraud. It is a growing concern in many industries. Fraud can be difficult to detect and may not be identified through standard audit procedures.

- Time and cost constraints: The audit risk model requires significant time and resources to assess and address the risks. Time and cost constraints may limit the level of assurance that can be provided to stakeholders.

Frequently Asked Questions (FAQs)

How can an auditor use the audit risk model?

An auditor can use the audit risk model to assess the risks associated with a particular audit engagement and to develop an appropriate audit plan to address those risks.

What is the most important element of the audit risk model?

The most important element of the audit risk model is an inherent risk, as it represents the level of risk associated with the nature of the business and the industry in which it operates.

What are audit risk model relationships?

The audit risk model describes the relationships between inherent, control, and detection risks. These risks are interrelated, and changes in one risk factor can impact the assessment of other risk factors.

Recommended Articles

This article has been a guide to what is Audit Risk Model. Here, we explain it in detail with its formula, examples, components, limitations, and importance. You may also find some useful articles here –