Part of our Risk Management guide

What is Inherent Risk?

Inherent Risk can be defined as the probability of a financial statement being defective due to error, omission, or misstatement, which occurs due to factors beyond the control or cannot be controlled with the help of internal controls. Examples include non-recording of the transaction by an employee, segregating duties to reduce risk of control, and collating employees/stakeholders for malafide intentions.

Types of Inherent Risk

- #1 – Risk Due to Manual Intervention – Human intervention can undoubtedly lead to errors in processing. No human can be perfect at all times. There are chances of mistakes/errors.

- #2 – Complexity of Transaction – Certain accounting transactions may be easy to record/report, but the situation is not the same every time. Complex transactions which may not be quickly recorded/reported.

- #3 – Complexity of Organizational Structure – Some organization may form a very complex type of organizational structure which may contain many subsidiaries/holding company/joint ventures etc. It may lead to difficulty in understanding and recording transactions in between.

- #4 – Collusion among Employee – To reduce the risk of fraud and errors, the organization segregates duties between multiple employees or other stakeholders. It is a kind of internal control. If employees collude with mala fide intentions, chances of control lapse increase and lead to fraud, error, and misstatement in the financial statement.

Examples of Inherent Risk

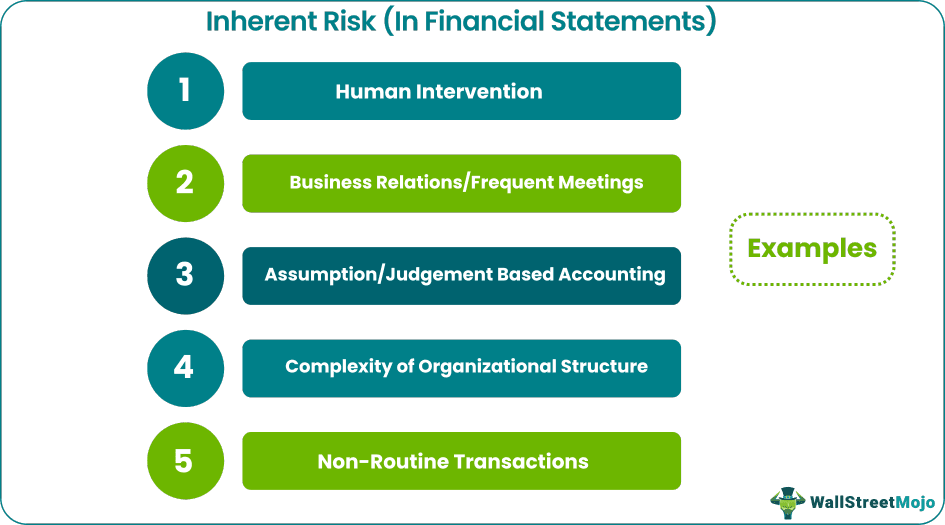

#1 – Human Intervention

There are chances of error in some activities out of multiple activities performed or the same action multiple times. For example, there are chances of non-recording purchase transactions from a vendor having multiple transactions or recording the same with the wrong amount. As discussed in the above-stated points, no human can always be perfect like machines.

#2 – Business Relations/Frequent Meetings

Sometimes frequent meetings and repeated engagements may lead to personal relationships with auditors, which may lead to the creation of personal relationships. Also, frequent engagement of auditors may lead to laxity or overconfidence. It may not be in the interest of the organization.

#3 – Assumption/Judgement Based Accounting

Although Accounting standards provide detailed accounting methods and policies for recording/ reporting transactions, there are still gray areas where organizations have to assess based on judgments and assumptions. It may vary based on organizations that create a gap for risk.

#4 – Complexity of Organisational Structure

Many organizations grow complex in structure due to the formation and existence of many subsidiaries, holdings, joint ventures, associates, etc. It creates the complexity of recording and reporting transactions between these companies.

#5 – Non – Routine Transactions

Sometimes it may happen where the organization needs to record a transaction that does not occur in routine or repeatedly. It can lead to an error because of a lack of knowledge or inaccurate knowledge.

Important Points about Inherent Risk

Due to growing innovations, changes in technology, and changing business models, inherent risk affecting an organization’s financial statement has also increased. Following are some of the significant affecting changes:

- Changing Business Models: Frequent changes in business models create complexities in recording and reporting new transactions. As a result, there is an increased probability of the financial statement being misleading due to the inherent risk of new business models.

- Increased Technology Innovations: Every organization is affected by growing technology. An organization needs to adapt itself according to changes taking place; otherwise, its infrastructure may become obsolete and may lead to the risk of wrong/incorrect/misleading information, etc.

- Difficulty in Adopting Changing Statutory Norms: There are growing complexities among businesses to adopt changes in statutory regulations and norms every day. Every organization needs to be updated about such changes taking place; otherwise may face penalties from government departments. Noncompliance with which results in penalties and fines.

- Reduced Manual Intervention: Human intervention is reducing with the increasing technological interventions. Robotics technology is performing tasks previously performed by human beings. It results in reduced human errors. As in the case of robotic automation, the program needs to be installed once. After that, it performs the same transaction repeatedly without any error.

Conclusion

An inherent risk that occurs in the financial statement is due to factors beyond the control of an accountant and is the result of error, omission, or misstatement of financial transactions. With the changing business models, growing technological innovations, and statutory norms inherent risk of the financial statement being misleading is also increasing.

Recommended Articles

This has been a guide to the inherent risk and its definition. Here we discuss types and examples of inherent risk in financial statements and its advantages and disadvantages. You can learn more about accounting from the following articles –