What Is Back-End Load?

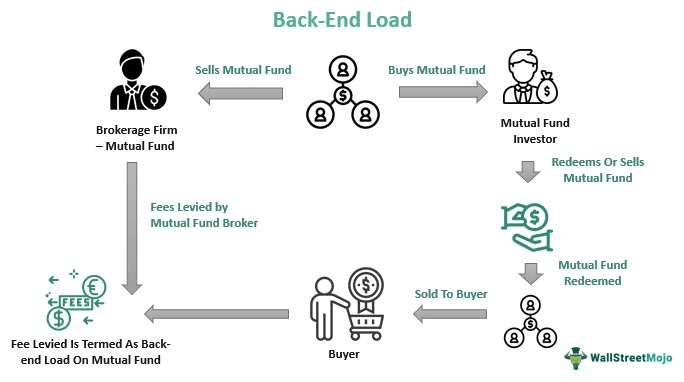

Back-end load (exit load) refers to a fee levied by the brokerage firms on the investors when they redeem their mutual funds’ shares or annuities. It is usually a certain percentage of the investor’s total value of the mutual fund investment. Its main objective is to discourage investors from frequent mutual funds trading and pre-mature withdrawals.

The fund managers or financial advisors charge this fee to earn a commission on the fund’s sale. They charge it to an investor irrespective of the yield on the funds. Although investors consider it unnecessary, they can avoid the fee by staying invested in the mutual fund for a certain period.

- The back-end load is a commission charged by the brokerage or mutual fund houses on the selling of mutual funds by the investors as a percent of the total investment.

- It stabilizes mutual funds by thwarting frequent trading of mutual funds by investors but acts negatively on investors by reducing their net yield while selling for emergency needs.

- The financial intermediaries receive the exit load. The funds’ operating expense does not include it.

- Widely available Index funds, ETFs, and no-load mutual funds do not have an exit load. For certain mutual funds, the investors can avoid the exit load if they hold the fund for a specified periHowever, thisThis strategy does not work in front-end loads.

Back-End Load Explained

A back-end load means a certain commission the brokerage firms charge the investors for selling their mutual funds. It is a small percentage of the investment. Sometimes the fees are called back-end sales charges or exit fees against the normal back-end fee. Most firms charge a flat or higher back-end load fee in the first year of back-end load mutual funds, which gradually decreases with increasing time, usually within five to ten years of investment in mutual funds. Hence, here the fee percentage is high in the first year; later, it decreases until it drops to zero.

A type of exit load that depends on the holding period includes the contingent deferred sales charge.

The back-end load calculation gets commonly expressed as a percent of the total investment made by the investors in mutual funds or annuities. However, informing investors of the actual fee charged by the fund houses in their investor security prospectus is mandatory. The mutual fund house or the fund manager gets the desired commission through the exit load. The load depends on the classes of mutual funds.

For instance, class A will have a front-end charge, whereas class B and C mutual funds do not have a front-end load, but they attract an exit load after the investors redeem their funds. It appears when certain funds offer different share classes. For example, class C shares have high operating charges. Typically, the percentage charged as back-end load ranges a maximum value of 5%.

Moreover, investors who stay invested for more than five years get their load percentage reduced to zero. The load charging stabilizes the mutual funds and prevents frequent trading. Exchange-traded, index, tax-saving, and no-load mutual funds do not have an exit load.

Examples

Some of the back-end load examples given here will clarify the concept much clearly.

Example #1

Let us look at an example of mutual fund B traded under a fund house. It has 5% of the total investment as the exit load. Let there be an investor X having mutual funds worth $10,000 in holding. The investor decides to sell the mutual fund after one year of holding.

Therefore, after redeeming the mutual fund, the fund house will deduct 5% * $10,000= $500 from the sales proceeds. It is a commission by the fund house. Hence, the investor will get a sum of $10,000 – $500= $9,500 as sales proceeds from selling the mutual fund.

Example #2

Let us assume that Sarah invested $200,000 towards mutual fund C, having a backload of 5% for the first year. However, at the end of 3 years, the charge will reduce to 3%. But, due to some urgent need, she sells the mutual fund within two years. In this case, the rate of exit load would still be 5% which fund companies would deduct upon selling the mutual fund C.

At the time of selling the mutual fund C, the value of the invested amount grows by 10% to $220,000. As a result, Sarah gets a yield of $20,000 on the investment.

However, after the selling of mutual fund C, the end load would be = 5%*220,000 = $110,00

Therefore, Sarah would get an amount = $220,000 – $11,000= $209,000 or the net yield would be = $209,000 at the back-end charge of 5%.

Example #3

Widely available index funds, exchange-traded funds (ETFs), and no-load mutual funds do not have an exit load.

ETFs are often stable and are available at a low exit load. Now, investors prefer ETFs over mutual funds as they overperform the latter. In addition, the former is more tax efficient. In mutual funds, some fund shareholders are often stuck with tax bills if the value of the holdings appreciates. Also, they have to sell some of their holdings to generate the necessary cash. In contrast, ETFs and stocks trade similarly. Here, fund houses are absent as investors trade/exchange ETFs among themselves.

In 2020, the COVID-19 sell-off accelerated the investments in ETFs. Mutual funds took close to $24 billion; in contrast, ETFs took close to $1.1 trillion since August 2020, owing to the low or absence of exit load.

Pros and Cons

Like every other financial instrument, exit load has some pros and cons, as listed in the table.

| Pros | Cons |

|---|---|

| Exit load stabilizes mutual funds from frequent withdrawals by investors. In short, it prevents pre-mature withdrawal of funds. | Exit load is an unnecessary charge that is not required to get levied. |

| It provides the necessary commission to fund managers and fund houses for managing the mutual funds. | It reduces the profit earned by investors while selling their mutual funds. |

| After 6 to 8 years, class B shares may get converted to class A shares. | It discourages people from investing in mutual funds owing to reduced yield. |

| It gets reduced eventually if the funds stay invested for more than five years. | In case of emergency fund requirements, the end load is a punishment to needy investors. |

Frequently Asked Questions (FAQs)

1. How do you calculate back-end load?

Back-end load gets calculated using the below formula:

Net investment value = investment value at the sale – back-end fee or,

Back-end fee= Investment value at a selling price – Net investment value

Alternatively, back-end fee = back-end load * investment value at sale.

2. Which is better front end load or back-end load?

Although it may appear to many investors that the exit load is better than the front-end, it is not true. A front-end load is far better than an exit load as redemption fees apply if one sells securities too often to make the full invested amount work for the investors.

3. What is a back-end load in insurance?

Back-end loads are the fees that investors must pay to the broker while selling their mutual fund or when they cancel their insurance policy. The percentage of fee charges as exit load is around five to six percent of the invested amount.

Recommended Articles

This article is a guide to What is Back-End Load in Mutual Fund/Annuities. Here, we explain it in detail with its pros and cons and examples. You can also go through our recommended articles on corporate finance –