Part of our Futures and Forwards guide

What Are Bond Futures?

Bond Futures is a contract that puts liability on the holder to purchase and sell a fixed amount of bonds as specified in the contract agreement at a price which is predetermined by the contract holder where the other side is the exchange. Hedgers and speculators use these to safeguard or protect their holdings.

Bond Futures can be bought and sold in the exchange market, the price and dates are standardized at the time when an agreement is entered into by the holder. These generally involve Treasury bonds or government bonds and are considered one of the most liquid financial products.

Key Takeaways

- Bond futures are financial contracts enabling investors to speculate on future price movements of government bonds or fixed-income securities, managing interest rate risk and potentially profiting from price changes.

- The value of bond futures is determined by the underlying bond’s price, yield, and maturity. The futures contract represents an agreement to buy or sell the bond at a predetermined price and future date.

- Bond futures serve multiple purposes, including hedging against interest rate fluctuations, speculating on interest rate movements, and gaining bond market exposure without physically holding the bonds.

How Do Bond Futures Work?

Bond futures are the most popular financial products that investors invest in. The delivery assets in this case are treasury or government bonds.

One of the important interest rate contracts is Treasury bond contracts traded in the United States. The party with the short position has a number of interesting delivery options:

- Delivery can be made any day during the delivery month.

- There are a number of alternative bonds that can be delivered.

- On the day of the delivery month, the notice of intention is to deliver at 2.00 pm, and the settlement price can be made any time up to 8.00 pm.

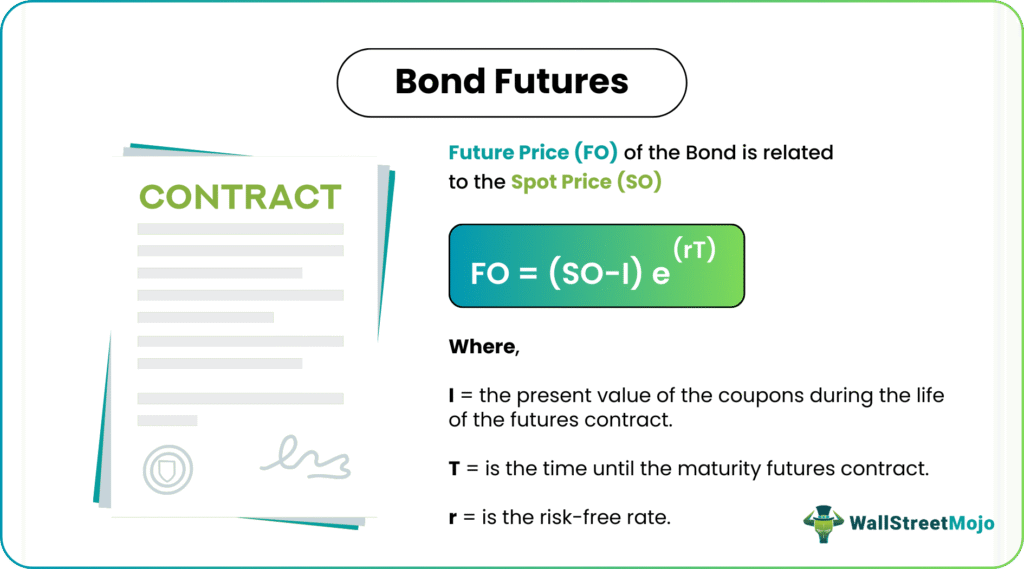

Calculating the price of the products is a crucial affair and there is a sequence of steps that is followed to learn how these are priced. Here is an instance that explains how these bond futures are priced:

CME bond futures have more than 15 years to maturity on the first day of the delivery month and is not callable within 15 years from that day can be delivered. The 10, 5, and 2-year Spot price (S0)

Where,

- I – the present value of the coupons during the life of the futures contract

- T – is the time until the maturity futures contract

- r – is the risk-free rate

This contract is quoted in dollars and thirty seconds of dollars per $100 face value. This is similar to the way bonds and notes are quoted in the spot market. Let’s say the settlement price of this contract for June 2017 delivery is specified as 124-150. This means 124 (15/32) or 124. 46875. Taking the next example, if the settlement price of September 2017 is quoted as 120-105 means 120 (10.5/32) or 120.328125.

Example

Suppose an investor enters into a treasury contract to deliver a bond @ 12 % coupon with a conversion factor of 1.6000 where the delivery will take place in 270 days. Coupons are payable semi-annually on the bond, and the last coupon date was 60 days ago, the next coupon date is in 122 days, the coupon date thereafter is in 305 days. The term structure is flat, and the interest rate is 10% per Annum. Assume that the current quoted bond price is $115.

The cash price of the bond is obtained by adding the quoted price the proportion of the next coupon payment that accrues to the holder.

= $115+(60/ (60+122)) * 6

= $116.978

A coupon of $6 will be received after 122 days (.3342 years). The present value of this

= 6*e(-.1*0.3342)

= 5.803

The future contract lasts for 270 days (0.7397). The cash future price, if the contract is written on a 12 % bond, would be

- = (116.978-5.803) e (0.1*.7397)

- = $119.711

There are 148 days of accrued interest from delivery. If the contract is written on a 12 % bond, accrued interest is excluded in order to calculate the quoted future price.

- = (119.711-6) + 148/(148+35)

- = $114.859

The quoted futures price is given below considering 1.6000 conversion factor equivalent to a 12% standard bonds

- = 114.859/1.6000

- = 71.79

How To Derive Cheapest Delivery?

The party with the short position or the writer of the bond chooses the bond that is cheapest to deliver among a wide variety of bonds. And his decision is based on the below derivation :

And the cost of purchasing the bond is,

The cheapest to deliver bond is one for which the below is the least.

The number of factors determines the cheapest to deliver the bond. If bond yields reach 6%, the conversion factor system enables the writer to deliver long maturity low coupon bonds. When yields are below 6%, then high short-term coupon bonds are favored.

Also, when the yield is upward-sloping, there is a tendency for bonds with long maturity to be favored, whereas when it is downward-sloping, bonds with short-term maturity will be delivered.

Conversion Factors

The contract allows the party with the short position to choose to deliver any bond that has a maturity of more than 15 years and is not callable within 15 years. A conversion factor is applicable at the time of delivery of a particular bond in exchange for the price received by the short position for the bond. The applicable quoted price is the product of the recent settlement price for the futures contract and the conversion factor. Taking accrued interest into account, the cash received for each $100 face value of the bond delivered is:

- Each contract is for the delivery of $100000 face value of bonds. Suppose that the most recent settlement price is 90-00, the conversion factor for the bond delivered is 1.3800, and the accrued interest on this bond at the time of delivery is $3 per $100 face value.

- The cash received by the party with the short position is then(1.3800*90.00) +3 = $127.20 per $ 100 face value. A party with the short position is one contract that would deliver bonds with a face value of $10,000 and receive $127,200.

Frequently Asked Questions (FAQs)

1. What are the advantages of bond futures?

Bond futures offer several advantages. Firstly, they provide liquidity, allowing market participants to enter and exit positions easily. Secondly, they facilitate efficient trading, as they are standardized contracts traded on organized exchanges. Thirdly, bond futures expose a diversified portfolio of bonds without the need for physical ownership. Finally, they also allow for leveraging positions, potentially amplifying returns.

2. What are the disadvantages of bond futures?

Bond futures also come with certain disadvantages. One disadvantage is leverage risk, as the use of leverage can amplify losses if the market moves against the position. Additionally, bond futures are sensitive to changes in interest rates, which can lead to price fluctuations and potential losses. Furthermore, bond futures require ongoing contract rollovers, which involve transaction costs and the need for active management to maintain exposure.

3. How do bond futures help manage interest rate risk?

Bond futures help manage interest rate risk by allowing market participants to hedge against adverse price movements in bonds due to changes in interest rates, providing a means to protect against potential losses or take advantage of interest rate predictions and market opportunities while maintaining liquidity in the futures market.

Recommended Articles

This has been a guide to What are Bond Futures. Here we explain the concept with examples, how they work, conversion factors, and deriving the cheapest delivery. You can learn more about from the following articles –