Part of our Private Equity guide

What Is Carried Interest In Private Equity?

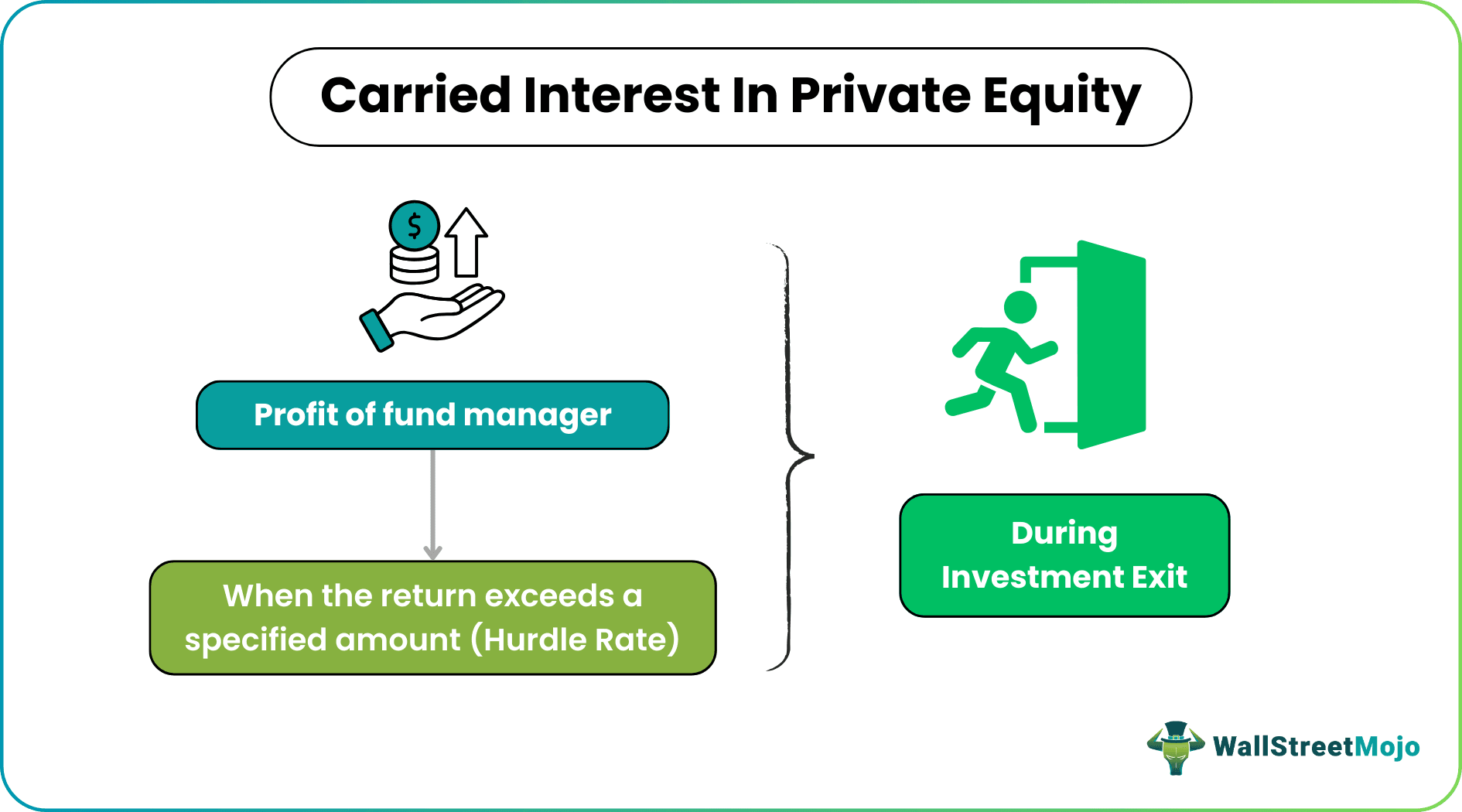

Carried interest, also known as “carry,” is the share of the profit earned by a Private equity fund or fund manager on the exit of investment done by the fund.

It is the most important of total remuneration earned by the Fund manager. It can be on a deal basis earned on every deal or a whole fund basis. Generally, the split in profits among the limited partners, the investors, and the general fund manager partner are 80:20. Remember, Carried Interest in private equity is not earned automatically. It will be earned by a fund manager only when a fund’s profits exceed a specified return. This specified return is known as the Hurdle rate. If the fund manager cannot achieve the hurdle rate, it won’t be entitled to receive any carried interest.

Carried Interest In Private Equity Explained

The term carried interest in private equity refers to the profits that the general partners earn in the field of hedge funds, private equity or venture capital. It is one of the main methods of making payment to fund managers and is paid provided the fund is able to earn a return that is more than the hurdle rate.

The hurdle rate in this context refers to a particular level of return that the investment should achieve so that a particular condition receives approval for execution. Based on this, the companies can decide whether it is profitable to continue with the investment or project at hand.

In the case of carried interest calculation in private equity, the general partner, which is a group or people or an entity, takes the liability regarding the activities based on the fund. They manage the day-to-day operations and have more risk and responsibility than limited partners.

The carried interest is like an equity in the startup companies, and venture capital funds use it to provide incentive to the fund managers. However, they also get other forms of compensation like salary or any other frm of commission, but the carried interest is a major chunk of their income. It does not fall under the ordinary income category but is a capital gain on which tax is charged.

Using this method the general partners pass the profits to the fund managers. But in case the fund is not able to perform as per the expectations, this payment can be taken back or forfeited. It is a situation where the investors who are the limited partners can claw back or withdraw apart of the amount. in order to cover up for the shortfall.

How To Calculate?

To understand the calculations of Carried interest in private equity, let’s take another example. Suppose a PE firm, ABC Capital partners, has raised $ 1 bn funds from Investors & General partners. Investors have contributed $950 million to this fund, and the Manager or General Partner contributed $50 million.

- So 95% was contributed by Limited partners and 5% by General Partner. After receiving the capital, GP then makes investments in various target companies to earn profits.

- After five years, the GP exited all investments and received $2.5 billion. In this scenario, Limited partners would get $1bn first as that would be the capital returned.

- The remaining $1.5 bn shall be divided between LP and GP in the 80:20 ratio. So the LPs would get $1.2 bn, and $0.3 bn would go to GP.

- So GP earned 5x (250/50) on investing $50 mn.

Now, in carried interest calculation in private equity, remember that not all profits go to GP. The profits are divided among senior partners who get a bigger pie while the remaining are distributed among others.

Carried Interest In Private Equity Explained In Video

Example

Let us understand the concept carried interest in private equity fund with the help of a suitable example.

Assuming a Private equity fund has a carried interest of 20 % for the fund manager and a hurdle rate of 10 %. When a PE Fund realizes the profits, these profits shall be first allocated to the limited partner, Investors. This process shall be repeated until these profits reach a cumulative IRR of 10%. This 10% shall be calculated on the capital amounts that the investors have contributed. Any profits over and above 10% shall be split between the General Partner & Limited Partner using a ratio of 20% for the General Partner and the remaining 80% for the Limited Partner.

Carried Interest Accounting

Let’s now understand how carried interest in private equity fund is treated in books of accounts. Under the provisions of Income-tax, carried interest in private equity shall be classified as capital gains. They would be taxed at the capital gain tax rate. It is a favorable rate compared to the ordinary tax rate. Most critics believe that carry should be charged at an ordinary tax rate; however, this is counter-argued with the point that any increased tax would suppress the incentive of the GP to take such high risk and invest in target companies to earn profits for LP.

There are two different views for understanding carry. They are -:

- Carry is considered as profit that is transferred from investor to manager. – Here, the focus is on the Legal form of the arrangement.

- It is seen only as a performance fee of the General partner – Here, the focus is on the substance of the arrangements.

The accounting treatment would be based on the view adopted for Carried Interest. Most firms continue to account for this on a cash basis as a distribution. At the same time, other private equity funds would account for it on an accrual basis. When such interest is accounted for accrual, then the carried interest balance needs to be adjusted after the realization of investments made and the revaluation of investments made.

Carried Interest Under IFRS

Under IFRS, various accounting standards would have to be considered. Firstly, you should determine it a -:

- A liability or

- A distribution

The standards to be considered are -:

- IAS 32 – Financial instruments – The fund manager is considered a service provider and not the only owner. So it is treated as per the liability model and not as per the distribution model.

- IAS 37 – Provisions, contingent liabilities, and contingent Assets – As per the agreement entered into, carried interest is treated on an accrual basis and recorded in each financial year. In this case, deal by deal, waterfall provision is applied wherein the hurdle rate is calculated for each deal. Here the fund has an obligation for each year.

Sometimes, such interest is settled by way of equity instead of cash. In this scenario, the transaction shall be treated as per IFRS 2 – “Share-based Payment.” For accounting, the Private equity fund shall measure the compensation payable at the fair value of the services received, and a corresponding entry shall be made into equity. Overall the impact would be a dilution of equity attributable to Limited partners, and no liability shall be created on the fund.

Carried interest in Private Equity is an incentive for a General partner for their decisions to successfully deploy the money and earn handsome profits on the Limited partner’s money. It is earned by a fund manager only when a fund’s profits exceed the hurdle rate.

Recommended Articles

This article has been a guide to what is Carried Interest In Private Equity. We explain how to calculate with example, accounting & carried interest under the IFRS. You may learn more about Private Equity from the following articles –