Part of our Private Equity guide

What is Private Equity?

Private equity (PE) refers to a financing approach where companies acquire funds from firms or accredited investors instead of stock markets. PE firms make a direct investment in these companies for an extended period as many of them are not publicly traded.

The ultimate goal of PE investments is to boost a company’s growth to the extent that it can go public or get acquired by a bigger entity. In exchange, investors earn fees and a substantial share of the improved profits. Many times, they also become the company’s shareholders.

- Private equity is a financing method that facilitates companies to acquire direct investments from PE firms for a long-term without adopting the traditional ways of fundraising such as public listing or business loans.

- The various methods adopted by the PE firms to invest in companies include buyout or leveraged buyout, merger, venture capital, growth capital, distress funding, fund of funds, etc.

- PE firms charge a management fee of typically 2% of AMU and a performance fee of 20% of the profits.

Private Equity Explained

Private equity comes as a rescue when struggling or growing companies cannot opt for public trading or bank loans. Resultantly, they take the help of a private equity firm that invests in the business directly without the need for public listing. A PE fund receives funding from wealthy investors, pension funds, labor unions, Insurance companies, universities endowments, foundations, etc.

The fund involves a limited partnership between general partners and limited partners. A general partner contributes 1-3% of the total investment and handles the fund’s management as a manager. The rest of the funding comes from limited partners whose liabilities and earnings are proportional to their capital contribution. They lock in funds for 3-5 years.

A company acquires PE funding to revamp its business or to grow. End goals usually revolve around going public, mergers or being acquired by a successful firm. PE firms tend to help with these objectives in exchange for management and performance fees. The management fee is usually 2% of the asset under management (AUM).

While the performance fee is the share of net profit allocated to the General Partner, it is typically 20% of the profit. A general partner can earn it most of the time after the hurdle rate is achieved. Many times, limited or general partners also acquire some equities of the company.

Video Explanation of Private Equity

Private Equity Investments

Raising PE capital from investors involves three crucial phases, i.e., pre-offering, offering and closing. Once convinced that the business holds potential, the PE firm invests in it through any of the following routes –

- Buyout or Leveraged Buyout: Here, the PE firm extends finance by buying the firm. Usually, more established companies raise funds through buyouts with the investors exercising a controlling interest in the business. In many cases, once the business bounces back or shows enough potential, the firm sells it off to another company or makes it public.

- Venture Capital: Startups and other small emerging entities are often left behind due to lack of funds. When they exhibit high growth potential with visionary business plans, venture capitalists provide them funding.

- Growth Capital: When a mature company seeks finance for expanding its business operations through restructuring or penetration into new markets, PE firms extend growth capital.

- Distress Funding: Hedge funds, investment firms and business development companies usually purchase a distressed company’s debt at a significant discount to make profits if the target company revives.

- Fund of Funds: PE firms pool investors’ money using mutual or hedge funds. It helps retail investors in putting their money as otherwise they cannot invest such massive amounts.

- Real Estate Private Equity: Such funds are accessible to high-net-worth investors, providing them with an opportunity to invest a considerable sum in the real estate through ownership, acquisition or financing of the target company.

Examples of Private Equity

A renowned example of private equity funding is the ride-service company Lyft. As a startup, it had been raising funds privately that helped it grow into one of the largest cab companies in the US and a close rival of Uber.

In 2017, Lyft raised an additional $600 million Series G PE funding, valuing the firm at $7.5 billion, a steep increase from the $5.5 billion funding round of 2018. Finally, in 2019, Lyft went public with its first-day valuation at $22.2 billion. The image above shows its journey of fundraising.

A piece of more recent news about private equity funding is of Morrisons, which is Britain’s fourth-largest supermarket. In 2021, Morrisons agreed to the takeover proposal by a global investment company, Fortress Investment Group. The deal values Morrisons at $8.7 billion. The supermarket giant rejected another PE firm’s offer of 5.52 billion pounds before saying yes to Fortress.

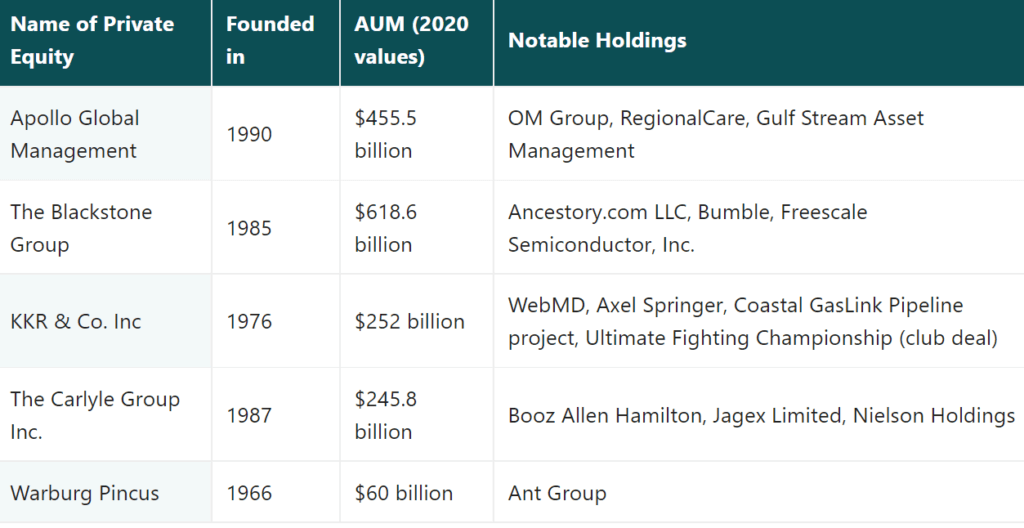

Let us now take a look at some highly renowned private equity firms of the world.

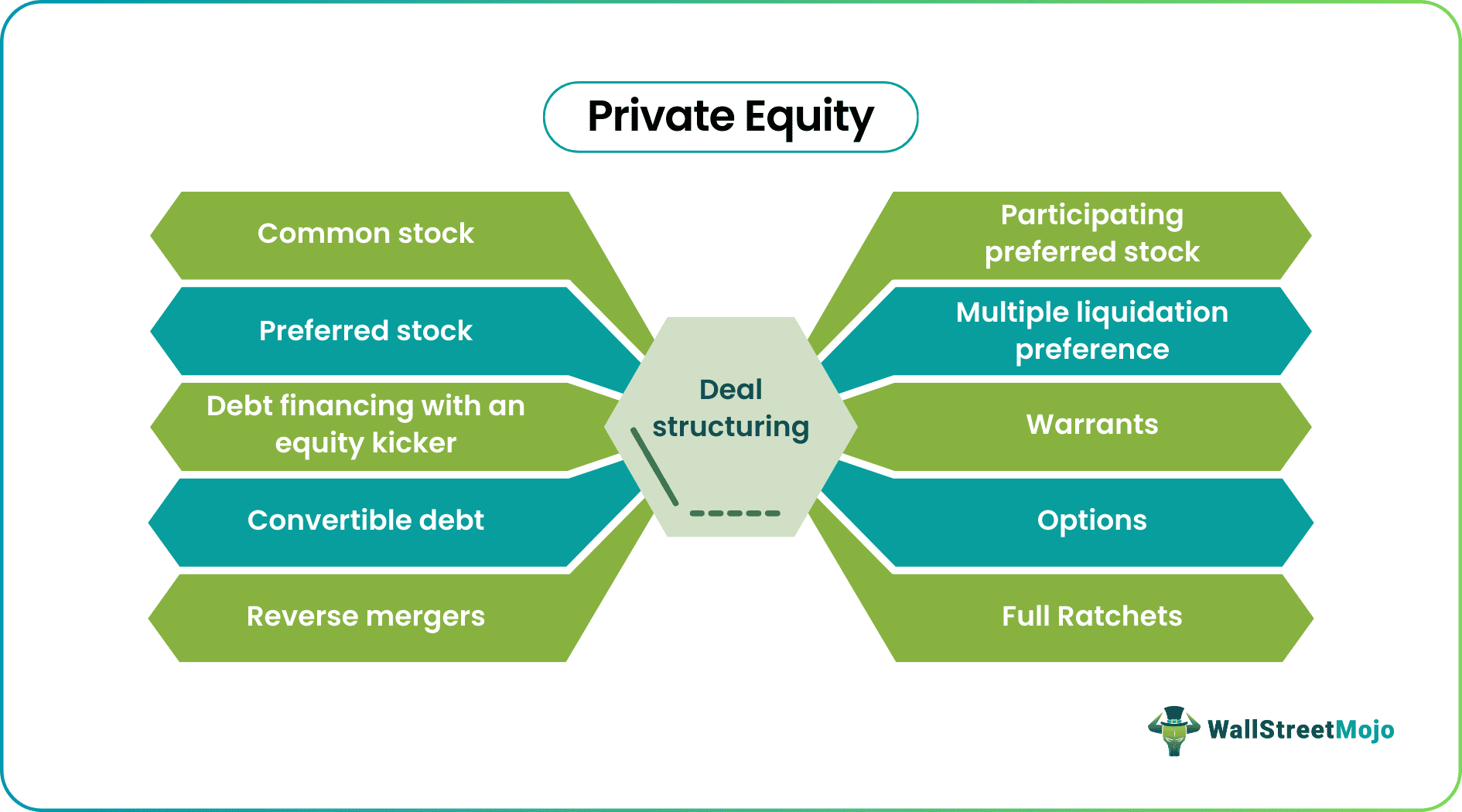

Private Equity Deal Structuring

A PE deal is structured after the investor negotiates with the investee and lays down the final clauses in a term sheet. In addition, there is usually an anti-dilution provision. It protects an investor from stock dilution if the stock is later issued at a lower price than what the investor originally paid.

Thus, PE would fund a company in any of the following ways:

- Common Stock: The investor and the target company (investee) mutually decide a certain sum to be given as funds. In addition, they decide upon the percentage of stock the investor will receive.

- Preferred Stock: PE firms are always keen to use preferred Stock structures the most as it can be converted to common stock at the holder’s decision.

- Debt Financing with an Equity kicker : It can be used by investees who are already operational and profitable or have reached Break-even. The number of shares and percentages is based on the size of the loan and the company’s value.

- Convertible Debt: Here, the investor can convert the holding at will into common stocks of the company. Most often, investors with the motive to earn high returns, make use of their conversion rights.

- Reverse Mergers: When an ongoing private company amalgamates with an existing public company with a trading symbol, it is termed as a reverse merger. Such a public company is referred to as a shell company.

- Participating Preferred Stock: It is a combination of preferred and common stocks. It can be converted to equity without the participating features when the company makes an initial public offering (IPO). Participation can either be equal or based on the seniority of rounds.

- Multiple Liquidation Preference: Here, preferred stockholders of a specific round of financing get the right to receive a multiple of their original investment when the company is sold or liquidated. This multiple can be 2x, 3x, or even 6x. Multiple liquidation preferences permit the investor to convert to common stock if the company performs well.

- Warrants: Warranties are derivative securities that give the holder the right to purchase shares of a company. Purchased at a pre-determined price, usually, they are issued to make stocks or bonds more attractive to potential investors.

- Options: Options gives the investor a right to purchase/sell shares of stock at a specific price, within a period. Stock purchase options are most common option.

- Full Ratchets: Full Ratchets is a mechanism of protecting investors from future down rounds. If the full ratchet provision states that if a company in future issues stock which is at a lower price per share than existing preferred stock. Then, the conversion price of the existing preferred stock would be adjusted downward to the new, lower price which increases the number of shares of previous investors. Term sheet in Private Equity will give more clarity on these mechanisms.

Performance Measure

Since successful PE deals can rake in billions, private equity jobs are quite popular as many companies pay handsome salaries. As per Glassdoor, the annual national average salary of a private equity associate in the US is $1,16,366. However, it is not easy to measure illiquid investments like PE investments compared to measuring the performance of the traditional asset classes. As such, the Internal Rate of Return (IRR) and investments multiples are the two measures used to assess Private Equity investments’ performance.

The table below provides us with the types of PE investments along with their IRR return expectations.

Private Equity Trends

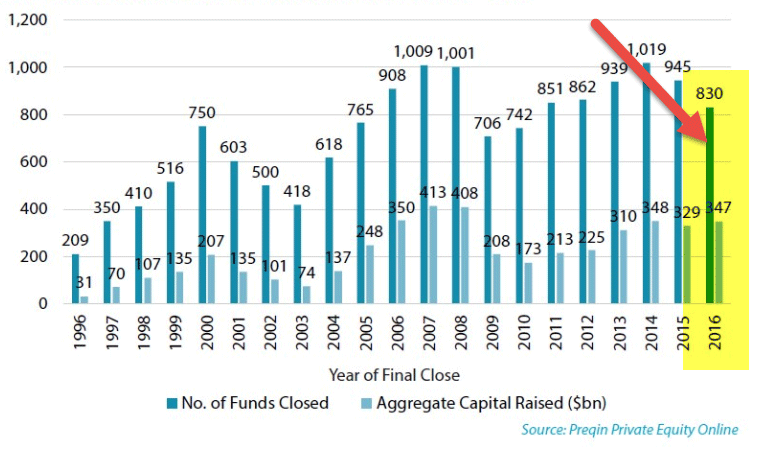

The industry saw tremendous growth post-1970s. In 2017, the total asset under the management of all PE funds together was reported to be USD 2.5 trillion. This growth has been due to the consistent and robust fundraised over the years by them.

Over the years, this industry has undergone consolidation, and hence the number of funds has fallen. Apart from traditional investors such as family offices and university endowments, PE fund has also attracted non-traditional investors such as sovereign wealth funds.

As per a report, the first quarter of 2020 witnessed a sharp decline in the PE investments by 25% in the US and 33% in Europe. In contrast, Asia recorded a 25% increase in the second quarter. The firms are now focusing on digitization of the investment cycle to facilitate easy access to the investors. Many investors are showing inclinations towards PE firms focusing on environmental, social and governance (ESG) factors.

FAQs

What is a private equity and example?

Private equity is a type of investment provided to companies with high growth potential (typically those not listed on any exchange) for a medium to long term period, in exchange for fees and profit.

Is private equity bad?

Private equity is a risky affair for investors since its failure results in massive losses. But if the company succeeds using the funds so acquired, investors could pocket heavy profits depending on the extent of success.

How does private equity make money?

PE adds value for the startups and other companies as it helps finance companies. Money comes through fees, shareholding and profits from sales/mergers or enhanced business.

Recommended Articles

This article has been a guide to What is Private Equity. Here we discuss the structure of Private Equity Firms, Deal structuring, Fees, and Performance Measures. You may have a look at the following articles to learn more about Private Equity –