Part of our Private Equity guide

Term Sheet Meaning

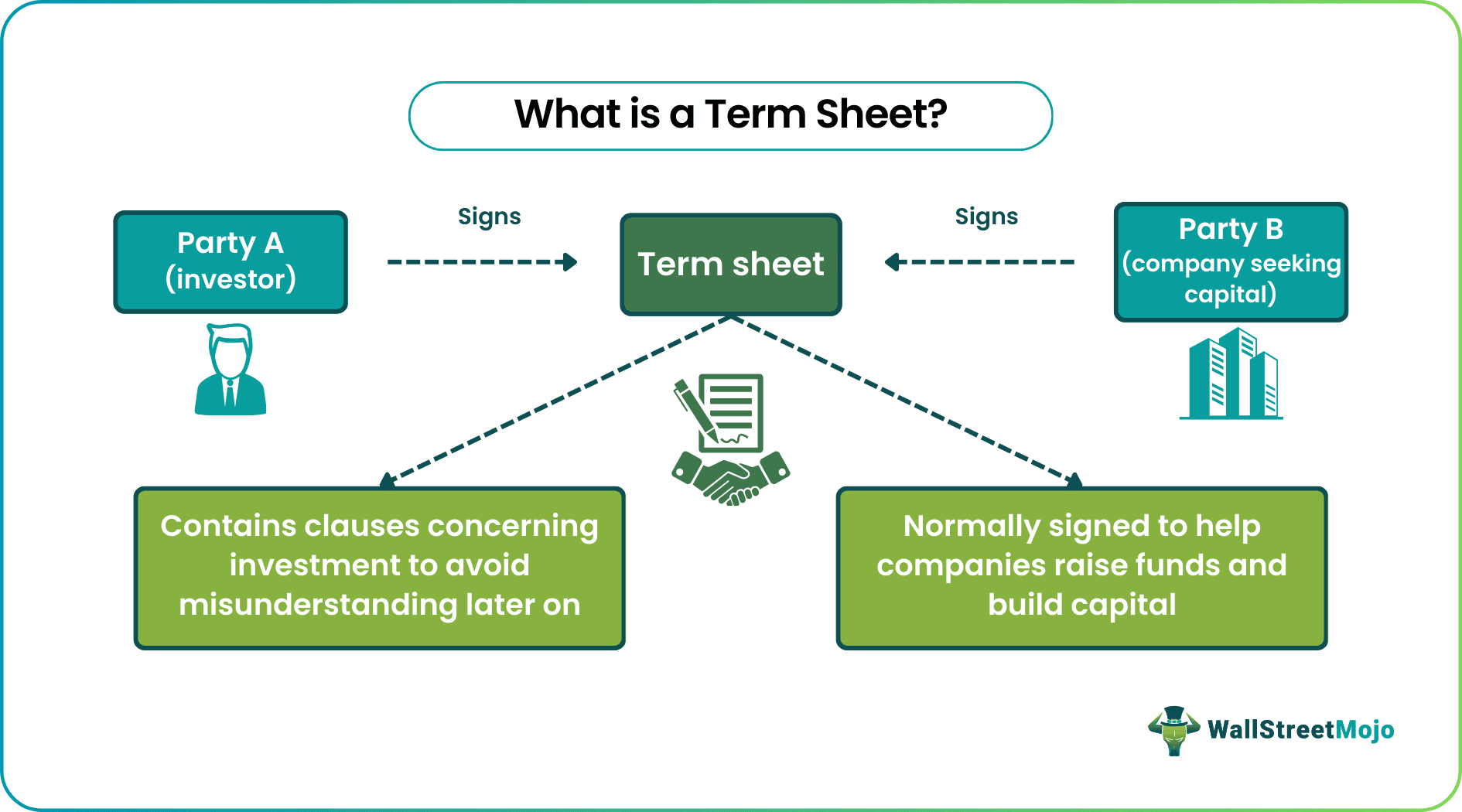

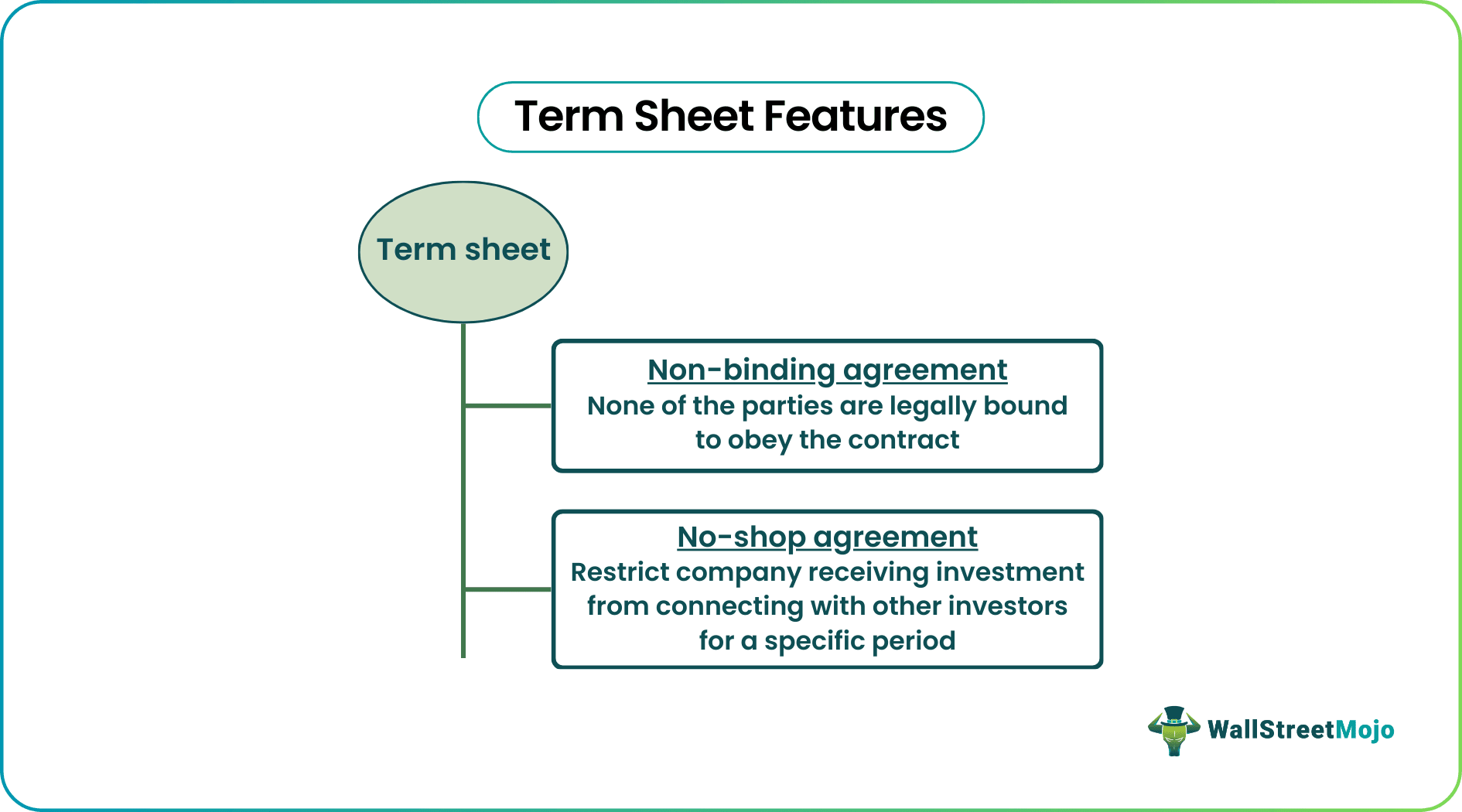

A term sheet is an agreement facilitating a fundraising process whereby two parties mutually agree to abide by the mentioned clauses concerning the investment. It is a non-binding contract, which neither of the parties is bound to obey. The document is shared at the very onset of the transaction deal.

The format of a term sheet is such that it contains all the points that the two parties, especially the investors, need to be aware of before spending on equity. It includes all required investment details, including issuer information, valuation terms, amount, and other information. It, thus, ensures the parties know what to expect once they begin their collective journey.

- A term sheet is a non-binding document containing all investment details to avoid further misunderstandings.

- It is similar to an LOI (Letter of Intent) or MoU (Memorandum of Understanding) that clarifies multiple aspects of a deal to all parties involved.

- As a no-shop agreement, it restricts target companies from having another set of investors for fundraising purposes for a specific period.

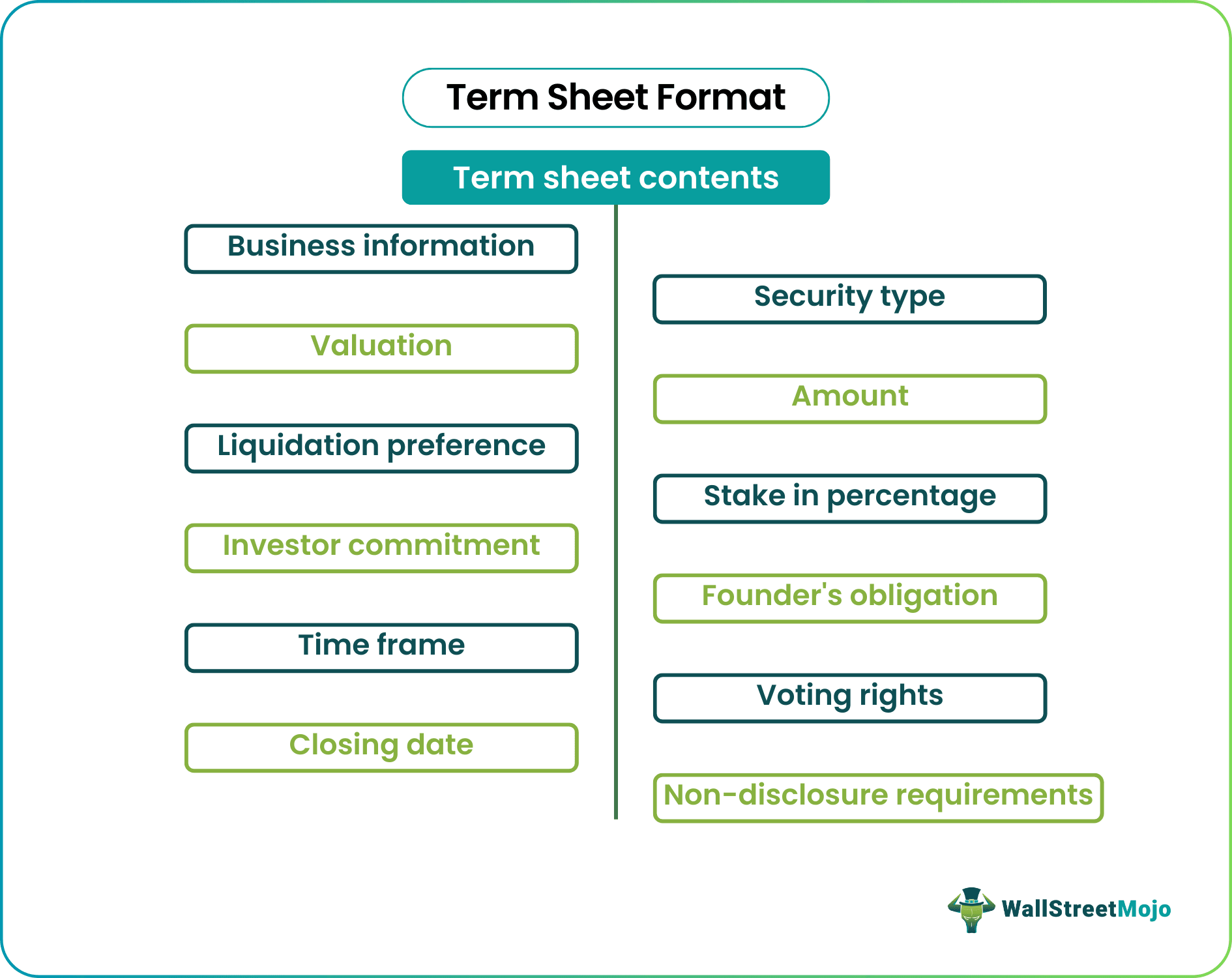

- Business information, type of security, valuation, investment amount, liquidation preference, percentage stake, voting rights, etc., are the most important aspects to be covered in a term sheet.

Term Sheet Explained

A term sheet discusses the major conditions for the parties to decide whether to get into a transaction deal. Moving into a term sheet investment contract ensures no misunderstanding exists in the future between the parties involved. It is similar to a letter of intent (LOI) or Memorandum of Understanding (MoU). These are non-binding documents featuring the terms for the parties to go through before they enter into merger & acquisition (M&A) or other deals.

A private equity provider identifies a few target companies that require to raise funds. Then, it goes through their business model, studies the business plan, and performs due diligence. After shortlisting, they conduct the necessary discussions and negotiations before finalizing the target company. Once a private equity fund provider decides which company to invest in, the term sheet comes into the scene.

Preparing this sheet is the first step towards finalizing the deal between the two parties. It contains all the essential and critical points of the agreement. However, it is a non-binding document that does not become an obligation for any parties, even if they sign it. It means either of them or both can back out if they do not feel like proceeding further.

The contract plays a crucial role in entrepreneurship. It is because investors need to know where they would be investing and how much returns they should expect. In addition, the contract acts as a no-shop agreement, restricting the target company’s relationship with other investors. As per this feature of the term sheet for investors, the target company cannot involve in another round of fundraising for a specific time range.

Format of Term Sheet

The term sheet template used in different sectors might differ. However, there are a few points that the agreement never fails to cover. Here is a list of clauses that are necessarily found within a term sheet for investors:

1. Business Information

This section includes the name of the parties involved. It should name the business seeking capital and the interested investor.

2. Security Type

This segment identifies the type of security offered and the price per share of that security. The types of assets available include equity, preference shares, warrants, etc. It is the initial deal term, which is determined between the private equity provider and target company.

3. Valuation

This clause mentions the price per share for the target company. As preferred shares have more attractive terms, they are preferred over equity by investors. Finally, the section provides information on the pre-money and post-money valuations of the company. The pre-money valuation is based on the number of outstanding shares before the financing is done. The post-money valuation, on the contrary, is done based on the number of shares outstanding post-financing.

4. Amount

The document should mention the amount of investment. Most of the time, the verbally discussed amount is negotiated greatly. As a result, the parties might get confused regarding the actual amount expected as an investment. Thus, specifying the amount clearly to avoid further confusion is a must.

5. Liquidation Preference

This section specifies the liquidation details. The liquidation preference is proportional to the amount invested. Therefore, it might be equal to or a multiple of the amount invested. This multiple can be thrice to five times the invested amount.

6. Stake in Percentage

It is the portion of the term sheet template that identifies what investors own in return for their investment. For example, if the percentage stake of company A is 25%, it will signify the investor’s ownership of the company. Based on the number of investors or the distribution of the rest 75% equity, A might have the chance of becoming the largest shareholder of the company.

7. Voting Rights

Based on the share of investment investors make, they get an opportunity to enjoy voting rights in the company. This section helps investors know the extent to which they can participate in the decision-making process of the company. When they have a say in the company, it makes investors more confident about choosing to help that particular company raise funds and capital.

8. Miscellaneous

- Investor commitment: It contains details about what is expected from investors’ end. The section includes information specifically on when the investors would have to remain vested.

- Founder’s obligation: This section displays the liabilities and responsibilities of the founder towards the venture.

- Time frame: Investors can take to go through the document properly. As a result, they can utilize the allowed time to decide whether to proceed with the investment.

- Non-disclosure requirements: This clause lets both the parties know the confidentiality required to maintain the deal once they sign it.

- Closing Date: This specifies the date of closure, which is normally a few days after the due diligence is accomplished.

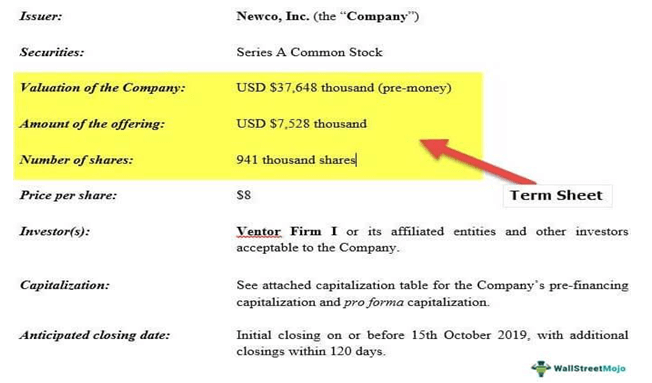

Example of Term Sheet

The following term sheet example in the form of a template has been shared. It shows what the contract looks like and the necessary information it contains.

Frequently Asked Questions (FAQs)

What is a term sheet?

It is a non-binding contract signed between two parties before they offer and accept investments to raise funds and capital, respectively, for a venture. Involving in the agreement is the first step towards beginning a collective journey of an investor and a company, especially a startup. Moreover, the contract contains all details concerning the investment, from who is the issuer and receiver to what liquidation preference it offers, etc.

Are term sheets binding?

No, it is not legally binding. As a result, even after the parties sign the document, they will have no obligation to obey the clauses. In short, either or both of them can step back from honoring the agreement if they do not wish to continue.

What is a term sheet in private equity?

In the context of private equity, a term sheet is defined as a non-binding contract that a private equity provider involves with a target company. Thus, it requires investment to raise capital to take its business venture forward.

Recommended Articles

This has been a Guide to Term Sheets & features. Here we discuss the format & check an example of what a sample term sheet investment template looks like. You may learn more about Private Equity from the following articles –