What Is Commercial Credit?

Commercial credit is an on-demand loan credit facility pre-approved by the bank or the lender and availed usually for urgent cash or working capital needs. Unlike loans where the borrower charges interest on the entire loan, such a credit feature helps borrowers pay interest only on the amount withdrawn.

In addition, most commercial credits are revolving; there is a limit. Once the amount is paid back, the credit is free again. It is mostly used to meet short-term requirements and day-to-day expenses. It is also known as business credit and can be either secured or unsecured and is very useful for the business in case enough cash is not available immediately.

- Commercial credit refers to an on-demand loan credit facility pre-approved by the bank or the lender. It is usually available for urgent cash or working capital needs. The two types of commercial credit are secured and unsecured.

- It is unlike loans. The borrower charges interest on the entire loan. This credit feature helps borrowers pay interest only on the amount withdrawn.

- Moreover, most commercial credits are revolving; there is a limit. Once one removes and pays back, the distinction is free again.

- It is a privilege provided to companies, and one must use it cautiously.

Commercial Credit Explained

Commercial credit services are credit facilities pre-approved by banks to specific companies to meet the day-to-day expenses of the business or any urgent and immediate requirement. It compensates for lack of cash, which might result in missing opportunities.

It is a privilege given to companies and should be used cautiously. The money withdrawn is not interest-free, so it should only be used when required. On the other hand, it helps companies to operate optimally as a sudden liquidity requirement does not stop the operation.

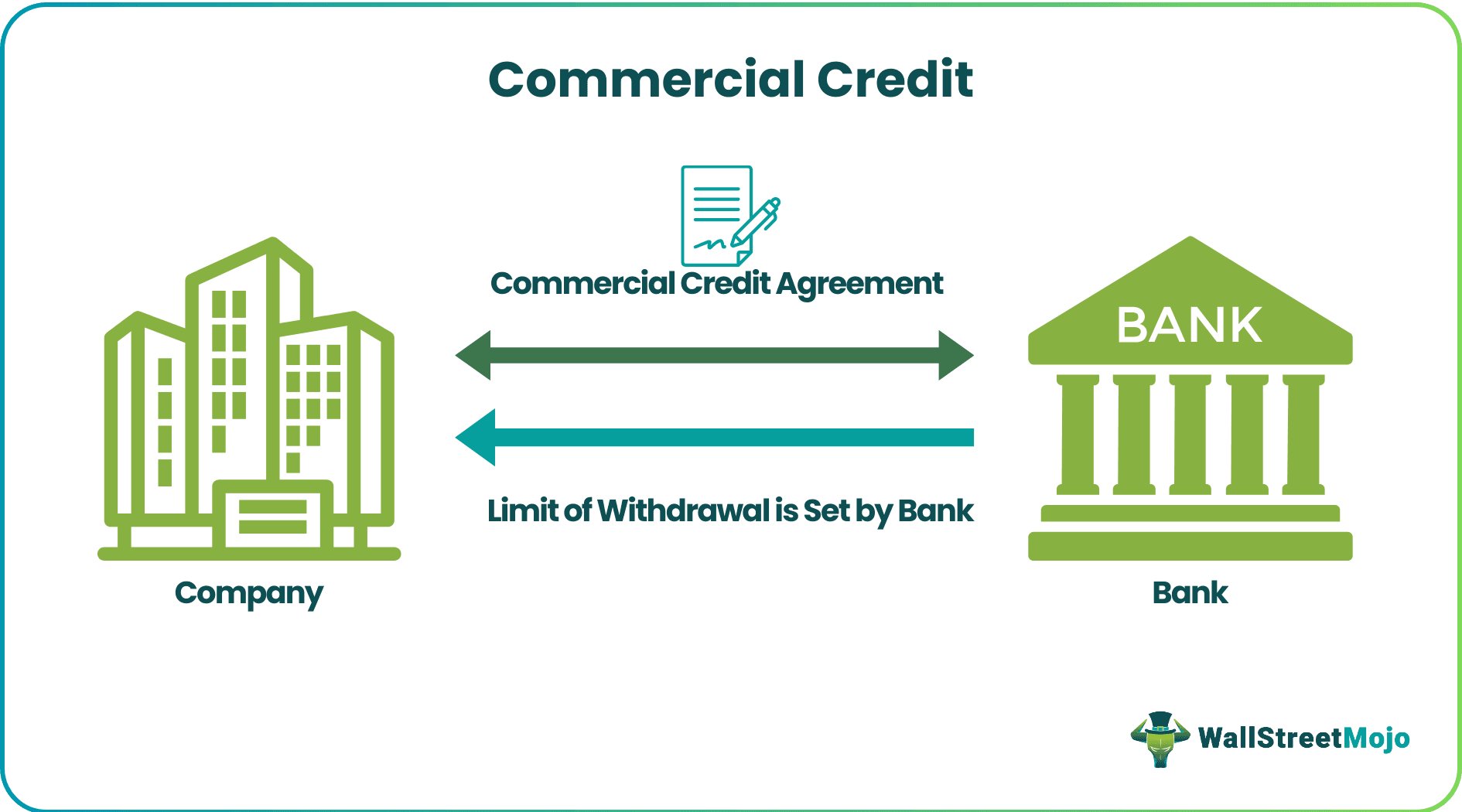

Companies require cash to deal with day-to-day expenses or sudden capital expenditure requirements. So, to avoid a cash crunch, they enter into a commercial credit agreement with banks. A commercial contract is a facility provided to companies by banks where the bank sets a withdrawal limit, which the companies can enjoy. No interest will be charged if the company does not withdraw any money. So, it is a pre-approved loan, but the interest is not charged on the absolute limit. It keeps on revolving when the company pays back the withdrawn money, the account refills, and allows companies to remove it again in the future.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

Commercial credit services can be of the following types.

#1 – Secured

In secured commercial credits, the bank charges collateral to agree with companies. So, if the company fails to make the payment, the bank has the right to liquidate the collateral and use the money to clear the outstanding amount. The credit is secured, so the interest charged is less, and the limit is high.

#2 – Unsecured

Collaterals do not back unsecured commercial credits. So, the credit line is risky. Banks usually charge higher interest rates in this case, and the credit limits are also less.

Example

XYZ Co. has entered into an agreement with a bank with a limit of $1,000,000. Due to the current COVID-19 situation, XYZ Co. is suffering a huge decline in sales. The fixed cost of the company is constant. So, to pay the fixed price, XYZ Co. must use its commercial credit and wait for the situation to recover. It is extremely helpful during emergencies.

Report

It is important for the commercial credit analyst to prepare a credit report to understand whether it is worth giving the facility to a business or not. Let us understand the points to remember during the process.

Ratios

Banks should analyse the following ratios from the financial statements of companies. while preparing the commercial credit report.

- Liquidity ratio

- Activity ratio

- Market ratio

- Profitability ratio

- Debt Service coverage ratio

Rules

The commercial credit analyst is responsible for understanding and identifying the rules, policies, and procedures that should be followed before deciding to give such credit to borrowers. Loans should be denied to customers who do not meet the requirements and standards.

Look For Exceptions

It is equally necessary to track the exceptions to the rules and policies and check whether such exceptions apply to the client. Such situations should also be followed and documented correctly for future reference while preparing the commercial credit report.

Advantages

It is important to understand the benefits of the process before making an application for commercial credit.

- It helps companies to meet the urgent requirement of cash. Moreover, that inculcates security in managers’ minds as they know it will not hurt daily operations due to cash requirements.

- As the interest rate is already fixed, it helps managers avoid taking high-interest loans during emergencies.

- Suppose there is a limited period discount on any asset the company needs. In that case, the company can use the commercial credit to buy the asset and increase productivity.

- It helps the company invest in long-term illiquid securities to earn more interest. As such, a credit takes care of sudden liquidity requirements, so they will not be required to liquidate illiquid assets. As a result, there is always a liquidity premium in illiquid assets.

- It helps to create a healthy relationship with the bank. In addition, consistent withdrawals and proper, timely interest payments may enable companies to achieve a high credit rating.

Disadvantages

Some disadvantages should be noted before making an application for commercial credit.

- Companies start to think it will protect them from meeting expenses, increasing the expenditure. So grows the risk of lower profit margin.

- If timely payments are not made, the interest burden rises, making it difficult for companies to pay back.

- Failure in payment may lead to poor credit rating, which will increase the cost of funding for the company.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What are commercial credit instruments?

Commercial credit instruments are bonds, loans, checks, or invoices. Governments, companies, and individuals use commercial credit instruments

What is a commercial credit bureau?

Credit reporting agencies gather information about the business used to estimate the company’s credit scores and ratings. Major business credit reporting agencies are Equifax Small Business, Experian Business, and Dun & Bradstreet.

What is a commercial credit bank?

Banks provide commercial credit to companies that access funds as required to help meet their financial responsibilities. For example, companies use retail credit to fund daily operations and new business opportunities, purchase equipment, or cover sudden expenditures.

What is a commercial credit underwriter?

Commercial credit underwriters are also known as insurance underwriters because they analyze risk on loan and insurance applications to examine the insurance coverage’s rejection or acceptance. In addition, they also form payment agreements and check all the data mentioned on the insurance applications.

Recommended Articles

This article is a guide to what is Commercial Credit. We explain how to make a report, with examples, types, advantages and disadvantages. You may learn more about financing from the following articles: –