Part of our Banking Products guide

Line of Credit Meaning

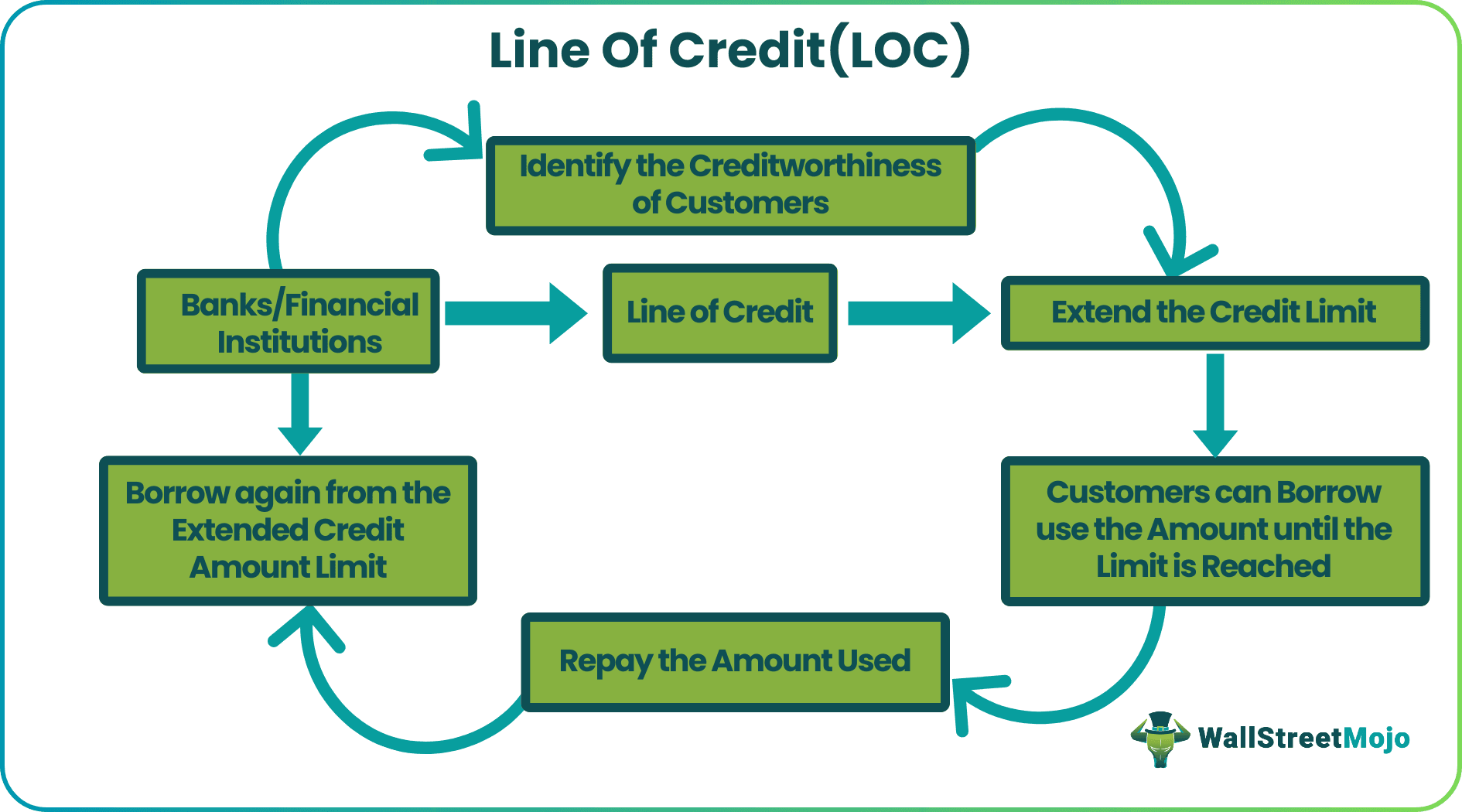

Line of Credit (LOC) refers to an extended credit limit that individuals receive for their creditworthiness. This amount is available for both personal and business purposes at any point in time. LOC is a revolving plan whereby individuals can use funds until the credit limit is reached, and once the used amount is repaid, they can borrow from the extended credit limit again when required.

A line of credit loan can be secured or unsecured. A secured LOC is backed by collateral and available at a lower rate of interest, given a lesser degree of risk involved. On the other hand, an unsecured LOC offers an extended credit limit at a higher rate of interest as the risk involved is high.

- Line of Credit (LOC) refers to the extended credit limit that financial institutions or banks offer individuals, and business is given their creditworthiness.

- The amount obtained can be used to serve both personal and business purposes.

- A secured LOC is collateral-based, and hence, it is available at a lower interest rate with minimal or no significant paperwork.

- An unsecured LOC is offered to fund seekers with a significant income with considerable credit scores and history. These are available at higher interest rates as the risk involved is more.

How Does a Line of Credit Work?

Line of Credit (LOC) allows fund seekers to have extended credit limits for use irrespective of the type and nature of the purpose. Most of the time, it is a revolving credit option that allows fund seekers to use the extended credit limit over and over again once they repay the previously borrowed or utilized amount. However, it is only applicable to an open credit account. On the contrary, when it’s a closed credit account, LOC is a non-revolving option with fund seekers using the extended credit limit only once without an alternative to borrowing any amount after repayment.

The customer can withdraw any amount as per the needs within the preset limit. Interest is charged only on the amount spent instead of the whole preset sanctioned limit. Furthermore, the customer can also schedule the repayment of the withdrawn amount either in a lump sum or monthly installments as per their convenience.

Such arrangements are usually available for a shorter period and are renewed periodically based on the satisfactory track record of the customer. Therefore, it is popularly used as a short-term financing instrument, helping individuals and businesses meet their personal and working capital needs.

LOC is an alternative recommended when something necessary is stuck because of the lack of funds. Thus, someone whose project implementation is on hold can surely opt for these credit options, given they know they would be capable enough to pay back conveniently. However, it is recommended not to opt for LOC for loan seekers for something that they can manage without. This is because it increases the following month’s expenses while making current purchases easier.

Types of Line of Credit

LOC is classified into two broad categories – Secured and Unsecured.

A. Secured Line of Credit

A secured LOC is an extended credit limit offered to individuals against collateral. Like a loan, the financial institutions or banks back the credit with security, which the former can claim in the event of non-repayment. As the borrowed amount remains secured, the interest rate at which the lenders offer the extended credit is pretty low. Plus, there is minimum or no paperwork or verification involved. Some of the types of secured LOC include:

#1 – Home Equity LOC

Home Equity Line of Credit (HELOC) is backed by the difference between the market value of the property involved and the amount borrowed. This differential amount becomes the major factor in determining the limit to which the credit extends. In addition, these LOC alternatives have a predefined period until which individuals or businesses can access the extended credit facility.

#2 – CD-backed LOC

A CD-backed line of credit remains secured against the money that fund seekers deposit in a Certificate of Deposit (CD). Like personal lines of credit, these options also remain accessible for three to five years.

#3 – Securities-backed LOC

It is a special line of credit backed by the securities the borrowers own. Under this scheme, investors can borrow between 50% to 95% of the value of assets they possess. The lender may not allow the borrowers to use the amount to trade securities. However, they have the liberty to choose how they want to spend it otherwise. The one opting for SBLOC has to make interest-only payments every month until the borrowers repay the total amount is repaid.

B. Unsecured Line of Credit

An unsecured LOC has nothing to do with the belongings of the fund seekers. There is no security or collateral required against the extended credit limit. However, the documentation and verification process is stricter to check if borrowers are capable enough to repay. Based on the creditworthiness, the approval is done. Some of the types of unsecured LOC are as follows:

#1 – Personal LOC

The approval of a line of credit personal completely depends on the seekers’ income, credit score, and credit history. If the financial institutions or banks are sure of the borrower’s repayment capability, they instantly approve the LOC. These finances best serve borrowers during medical requirements and other emergency needs. People having scattered debts can use the amount to close all outstanding loans and have only a single financial LOC obligation.

#2 – Demand LOC

It is the financial instrument that allows individuals to borrow an amount at any time. The borrowers have to repay either as interest-only payback or interest plus principal payback. The lenders or banks determine the repayment option based on the LOC terms. Moreover, when this demand LOC is collateral-based, it becomes an SBLOC.

#3 -Business LOC

The line of credit for business is for companies that require finance instantly. The lenders evaluate the market value of the firm and its profitability. In addition, they also check the level of risks associated with the businesses. They determine the extended credit limit for borrowers based on their evaluation.

Line of Credit Examples

Let us consider the following examples to understand how the concept of Line of Credit works:

Example 1

Suppose customer A is provided with a $10,000 LOC to purchase a home secured against the house by Baseline Bank. The bank sets a loan term of 5 years and allows customer A to use the funds within the overall limit ($10,000). It charges an interest rate of 10%. So, customer A spends $3,000 and has to pay only 10% of the amount as interest, not the entire $10,000 LOC.

Further, Baseline Bank allows customer A to make payments on the line of credit either in the form of monthly installment on interest and principal or payment towards interest and payback principal at the end of the loan term.

Example 2

Though the LOC is one of the best forms of obtaining funds, over-borrowing might make financial institutions make a tough decision sometimes.

Recently, Wells Fargo & Co shut down all its personal lines of credit as customers used them to convert their scattered debts and financial obligation into consolidated loans. Many of them used the LOC amount, ranging between $3,000 to $100,000, for renovating the home or avoiding overdraft fees on linked checking accounts. The institution, therefore, stopped offering LOC while notifying its customers about the same.

Advantages

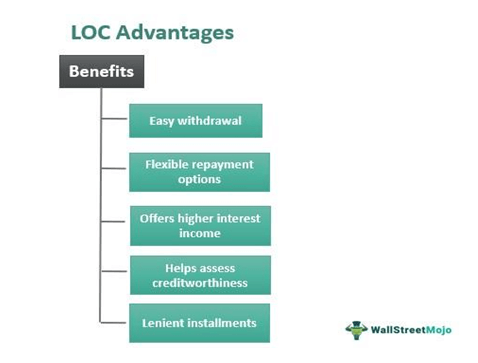

Line of Credit offers many benefits over traditional loans that individuals apply for to serve their personal and business purposes. Some of them are as follows:

- It allows customers to withdraw money as and when required without complying with loan formalities. Further, lenders charge interest only on the amount spent.

- The customer can pay back in a lump sum or through installments depending on their repayment ability.

- An unsecured line of credit is usually charged a higher interest rate and is a good source of higher interest income for banks and financial institutions.

- Prepayment or part payment cost is comparatively less in the LOC than mortgage loans.

- It helps assess the creditworthiness of borrowers based on how timely they pay off their loans.

Disadvantages

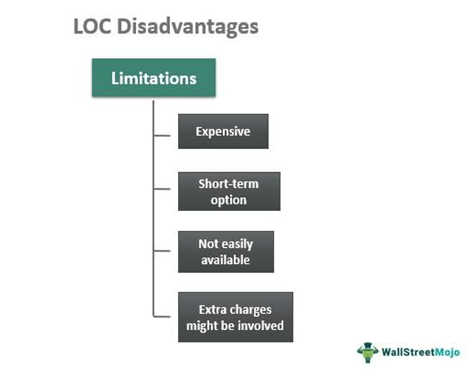

Let us also have a look at the limitations of LOC:

- The LOC is usually available for a shorter period and hence, people consider it as a short-term financing option.

- Though the higher interest rates for unsecured LOC help financial institutions accumulate more funds for financing, the same hampers borrowers who wish to take up the LOC option.

- Not every financial institution or bank offers the LOC option.

- When people get a chance to spend an extended amount, they overspend, which hampers their financial stability.

- Some lenders or financial institutions might charge a commission or fee for finance seekers to enjoy an extended credit limit facility.

Frequently Asked Questions (FAQs)

What is a line of credit?

LOC refers to a financing option whereby financial institutions or banks offer extended credit limits to borrowers to use, given their creditworthiness. It can be secured or unsecured. While the latter involves a higher rate of interest for repayment as the risk involved is higher, the former is collateral-based and offered at a much lower rate. This financing alternative can be used to serve both personal and business purposes.

Is the line of credit a loan?

Yes, LOC is a kind of loan that individuals can obtain from financial institutions or banks. It comes as a reward for loyal customers. The lenders offer an extended credit limit to the creditworthy customers, allowing them to borrow money up to the permitted limit.

Does a line of credit affect credit score?

Yes, the LOC affects the credit score as timely repayments of the extended credit amount let lenders gain more confidence in those customers. In addition, the timely repayment takes their credit score to another level, resulting in an even more extended credit limit offering the next time.

Recommended Articles

This article is a guide to Line of Credit & its meaning. Here we explain how it works, its types, advantages & disadvantages along with proven examples. You may learn more about corporate finance from the following articles: –