Part of our Banking and Financial Institutions guide

What Is A Commercial Bank?

Commercial Banks are profit-seeking financial institutions. They receive deposits from customers at a lower rate of interest and offer business loans at a higher interest rate. They serve individuals, small-scale businesses, and medium-sized businesses.

Commercial banks augment their profits by offering additional investment products and banking services—current account deposits, savings accounts, fixed deposits, cash credit, advances, overdrafts, locker facilities, and investments. Due to competition, they need to innovate continuously, adapting to automation, data analytics, digitization, artificial intelligence, faster transactions, and quicker responses to market changes.

- Commercial banks are licensed financial institutions that provide banking solutions to their clients—individuals, small businesses, and medium-sized firms.

- Commercial finance institutions serve both individuals and businesses. Retail banks on the other hand extend services only to individuals.

- These institutions also execute various secondary functions for their client—overdraft facility, agency services, discounting bills of exchange, traveler’s check, investments, and locker facility.

How Do Commercial Banks Work?

Commercial banks play a part in economic growth and liquidity by catering to a multitude of customers. Their clientele comprises individuals and small to mid-sized corporates. The customers obtain low rates of interest on bank deposits but the bank loans funds at a higher interest rate to earn a margin—also known as the spread. Recently, some of these banks introduced investment banking divisions—Citibank and JPMorgan Chase. But banks like Ally operate only on commercial aspects of the business.

These banks mainly offer loan facilities and accept deposits. But in addition to that, they provide saving accounts, merchant services, commercial loans, global trade services, treasury services, lending services, current or cash management services, corporate loans, and online banking services.

In the contemporary digital era, most commercial banks function online—customers carry out electronic banking transactions without visiting their bank’s branch office. As a result, operating profit margins for “virtual” banks have increased. The Internet has brought down operating expenses (OpEx) – banks do not have to maintain physical branches – ancillary charges on rent, property taxes, and utilities have gone down.

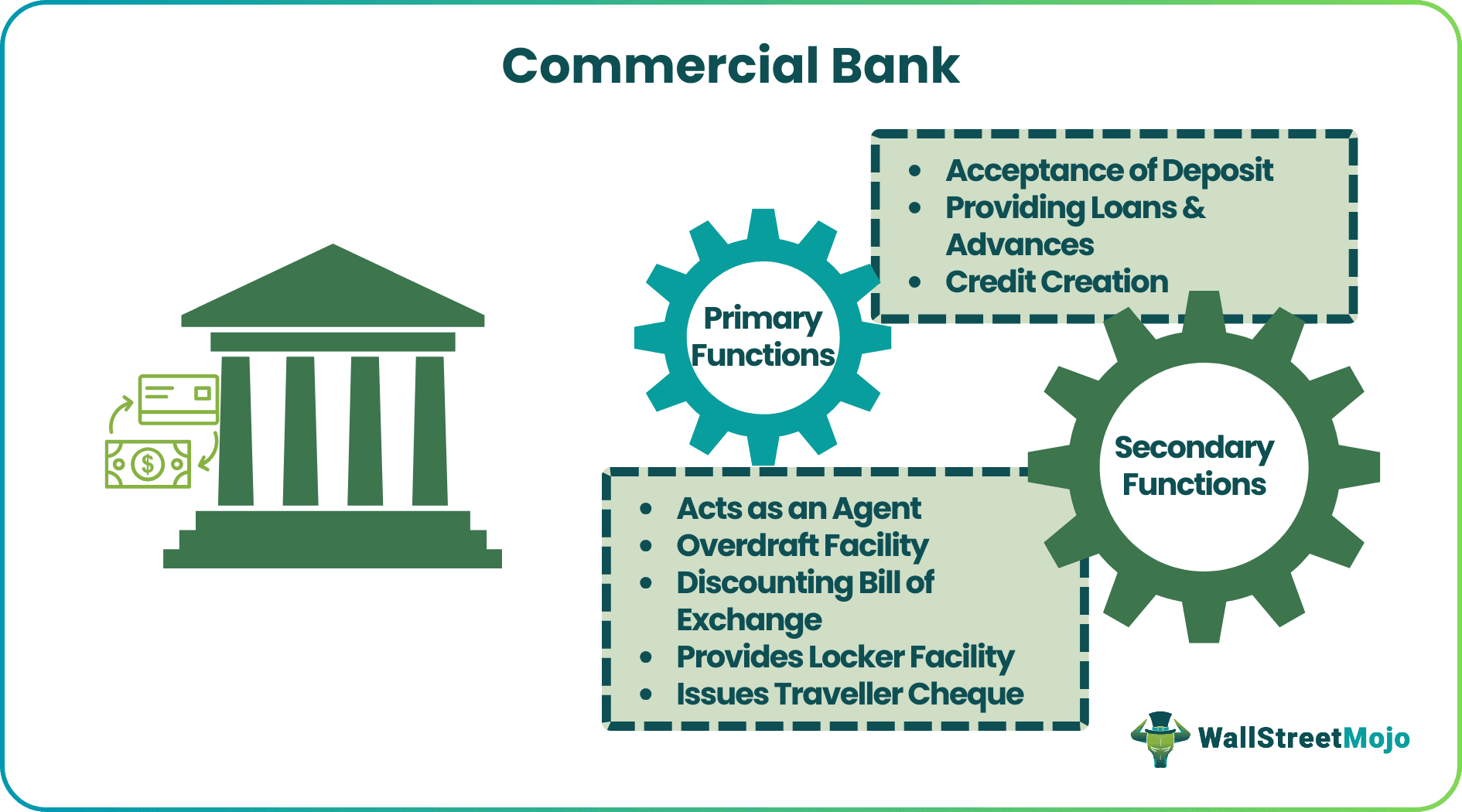

Functions of Commercial Banks

Banks survive on loans. Commercial banks are no different. Given below are the various functions:

#1 – Primary Functions

- Accepting current, demand, fixed, and savings account deposits from customers;

- Providing cash credit, auto loans, mortgage loans, short-term loans, and advances;

- Creating credit by expanding deposits.

#2 – Secondary Functions

Other miscellaneous services are enlisted below:

- Banks act as agents for funds transfer or collection—make payments on behalf of the clients;

- They extend overdraft facility to the current account holders;

- They discount the bills of exchange;

- Offer locker facility;

- Issue traveler’s checks.

Commercial Bank Video Explanation

Role of Commercial Banks

The banking industry as a whole runs the economy of a nation. The roles of a commercial bank are as follows:

- They aid in the successful implementation of monetary policies.

- They boost the industrial sector by offering short, medium, and long-term finance.

- They accelerate trade by offering agency services, overdraft facilities, and other solutions to wholesale and retail businesses.

- These financial institutions help lower and middle-class customers in procuring consumer products on loans—easy repayment options.

- Banks also operate on rural and regional fronts.

- The agricultural sector receives strong financial backing from commercial institutions facilitating crop cultivation, irrigation facilities, dairy farming, poultry farming, horticulture, and pisciculture.

- They adopt innovative ways to facilitate easy banking—automation, digitalization, and artificial intelligence.

- They ensure a superior level of data security for their clients.

Examples

According to a Federal Reserve Statistical Release report, JPMorgan Chase & Co is the largest commercial bank in the US. As of September 30, 2021, JPMorgan possesses consolidated assets worth $3,290,398 million. It is closely followed by Bank of Amer Corp and Wells Fargo & Co, with consolidated assets worth $2,400,819 million and $1,786,611 million, respectively.

JPMorgan Chase provides global financial solutions to its clients ranging from treasury payments, commercial real estate, international banking, credit, and financing. The bank also offers investment banking and asset management facilities.

Types of Commercial Banks

They are further classified into the following categories:

- Private Sector Banks: The majority stake is owned by private shareholders (individuals or corporates). They accept deposits and distribute loans to individual customers, small businesses, and medium-sized businesses.

- Public Sector Banks: For public banks, majority equity lies in the hands of the government. Nationalized banks provide financial services to mass customers at affordable rates.

- Foreign Banks: As the name suggests, these financial institutions operate in foreign countries but have head offices in the parent country. The bank’s foreign branches take deposits, extend loans, engage in securities trading, and facilitate foreign exchange functions.

Commercial Banking vs. Retail Banking

Commercial and retail banks are both categorized as depository banks. Commercial finance institutions serve both individuals and businesses. Retail banks, on the other hand, extend services only to the general public. Commercial finance is a huge sector operating in small and medium scale industries, whereas retail banking is the front for the common people.

In addition to primary functions, commercial institutions offer services like trade finance, corporate loans, cash management, treasury management facility, agency services, and overdraft facility. In comparison, retail banks offer services like mortgage loans, savings and checking accounts, line of credit, debit cards, and credit cards.

Frequently Asked Questions (FAQs)

How do commercial banks make money?

Commercial finance institutions offer various loans and advances—personal, mortgage, business, and auto loans. The banks earn interest on these credit services, and it is always less than the interest rate offered to the depositors. This margin between the interest rates acts as their source of income.

What are the different types of banks?

Financial institutions are classified as central banks, agricultural banks, cooperative banks, investment banks, savings banks, retail banks, rural banks, small finance, industrial banks, exchanges, and specialized banks.

What is the main purpose of commercial banks?

It is a licensed financial institution that provides various financial products and services—deposits, loans, credit, investments, locker facility, and overdraft facility. They provide banking facilities to individuals, small businesses, and medium-sized businesses. Banks make profits by charging interest on loans.

Recommended Articles

This has been a guide to Commercial Bank and its Meaning. Here we explain the functions of a commercial bank along with examples, types, and roles. You can learn more about accounting from the following articles –