Part of our Valuation Methods guide

What is Liquidity Premium?

The liquidity premium is the additional return that the investors expect for not readily tradable instruments. Therefore, one cannot easily convert it to cash by selling it at a fair price in the financial market.

The terms – liquidity premium and illiquid premium – are interchangeably used as both terms mean the same. Therefore, any investor is entitled to receive an additional premium if they are looking into a long term investment.

Key Takeaways

- The liquidity premium refers to the additional return investors anticipate for not readily tradable instruments.

- Examples of liquid instruments in nature are stocks and treasury bills. One may sell these instruments at a fair value, the prevailing market rate.

- Examples of lesser liquid instruments are debt instruments and real estate.

- The terms liquidity premium and illiquid premium are interchangeably used as both terms mean the same. Hence, one can obtain extra compensation if they are into a long-term investment.

- Examples of liquid instruments in nature would be stocks and Treasury bills. One can sell these instruments at any time at a fair value, which can be the prevailing market rate.

- Examples of lesser liquid instruments can be debt instruments and real estate.

Liquidity Premium Theory on Bond Yield

The yield curve is the investors’ most common and closely examined investment pattern. These yield curves can be created and plotted for all types of bonds, like municipal bonds, corporate bonds, and bonds (corporate bonds) with different credit ratings like BB Rated Corporate Bond or AAA Corporate Bond.

This liquidity premium theory shares that investors prefer short-term debt instruments as one can quickly sell them over a shorter period. That would also mean lesser risks like Default risk, price change risk etc., to be borne by the investor. Below are some examples of the same.

Example #1

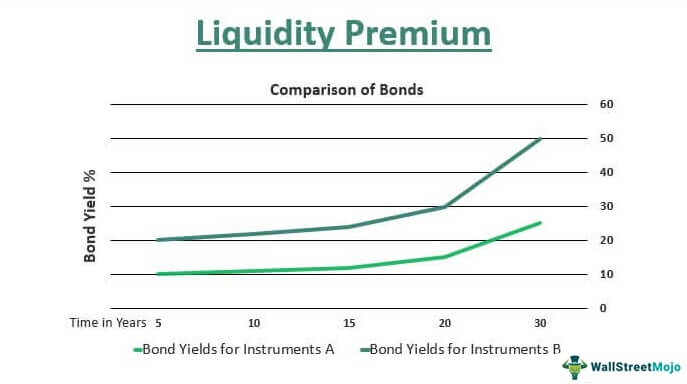

One made investments in two government bonds – Bond A and Bond B. The below graph shows the effect of the maturity period or the duration of an asset held for several years.

| Time in Years | Bond Yield for Instrument A | Bond Yield for Instrument B |

|---|---|---|

| 5 | 10 | 10 |

| 10 | 11 | 11 |

| 15 | 12 | 12 |

| 20 | 15 | 15 |

| 30 | 25 | 25 |

Instrument A is a government bond with a longer maturity period than instrument A, a government bond investment. Instrument A has a maturity period of 20 years, while instrument B has 15 years only. In this case, Bond B has a coupon rate or bond yield of approximately 12%. In comparison, Bond A enjoys the additional 3% enjoys.

This additional benefit in your investment returns is known as the liquidity premium. The graphical representation above shows that one can provide this premium if the bond holds for a longer maturity period. This premium gets paid to the investor only on the maturity of the bond held.

The above example perfectly explains the rising yield curve, supporting the liquidity premium theory. The same stands true in the case of the U.S. government, which pays progressively higher rates to its investors for their investments in debt instruments with longer to much longer maturities.

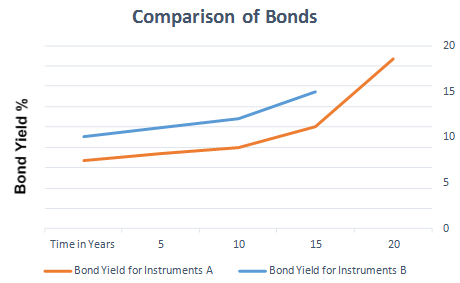

Example #2

Liquidity premium might be a more prevalent concept for government bonds. At the same time, there are corporate bonds that provide the premium. For example, suppose an investor has planned to purchase two corporate bonds simultaneously to maturity and the same coupon rates or coupon payments. However, if only one is trading on a public exchange and the other is not, the bond not trading on the interchange is exposed to different risks.

Since this is a non-public bond, the bond attracts a premium on maturity, the liquidity premium. This premium is clear and defines the only reason and consequence of the difference in the. Since this is a non-public bond, the bond attracts a premium on maturity, termed the liquidity premium. This premium is clear and defines the only reason and consequence of the difference in the prices of the bonds and yields for the same.

Video Explanation of Liquidity

Advantages

- It offers a premium to the investors in the case of illiquid instruments – which means attracting certain investors and having them invest for a longer period and duration.

- Sense of satisfaction among the investors about the government-backed instruments about their will, longevity, assurance, and constant and safe returns.

- Offers a direct correlation between risk and reward. For example, in the case of illiquid debt instruments, the various risks will be borne solely by the investor. Hence, providing the premium component at maturity is the reward one expects for the risk undertaken.

Limitations

- There can be cases where the liquidity premium can attract many investors to the illiquid market rather than the liquid instruments, which means a constant circulation of money/ money instruments in the economy.

- The reward for the risks undertaken might not be directly proportional to an investor.

- A low premium at the time of maturity might affect the investor’s emotions in a negative way toward the government or the corporate house issuing it.

- It is difficult for any issuing house or entity to define the premium and adjust to changing market and economic situations. Without a liquidity premium, it gets almost impossible to attract new investors or maintain the existing ones.

Conclusion

Debt instruments are subject to various risks like event risk, liquidity risk, credit risk, exchange rate risk, volatility risk, inflation risk, yield curve risk, etc. The higher the duration of the debt holding, the higher the exposure to these risks. Therefore, an investor demands a premium to manage these risks.

However, it is up to investors to understand that liquidity premium could be only one of the factors for the slope of the yield curve. The other factors, for example, can be the investor’s investment goals, the bond’s quality, etc. Also, for our point before we conclude, as these are the factors, the yield curve might not always be upward sloping – it might go zig-zag, flattening, or even inverted at times.

Therefore, as much as liquidity premium is essential for an investor, other theories affect the yield curve and reflect the future expectation and the varying interest rates.

Frequently Asked Questions (FAQs)

How to calculate liquidity premium?

One may calculate the yield curve, or realized return, of two investments with different liquidity levels to obtain liquidity premiums. However, to estimate the liquidity risk premium for an investment, one must compare two similar investment options, one liquid and the other illiquid.

Can liquidity premium be negative?

The liquidity premium gives the excess return sign. A negative excess return may indicate a negative liquidity premium. Hence, this would imply that investors are willing to accept a lower return for investing in relatively illiquid assets than the more liquid alternative.

What is liquidity premium in banking?

The liquidity premium refers to the additional return an investor may anticipate for not effortlessly tradable instruments. Therefore, one cannot easily convert it to cash by selling it in the financial market.

What is the liquidity premium theory’s fundamental assumption?

The liquidity premium theory assumes that investors view different maturities bonds as perfect substitutes and completely unsubstitutable. Therefore, one must always choose the bond with the highest expected return, regardless of maturity.

Recommended Articles

This article is a guide to what Liquidity Premium is and its definition. We discuss the liquidity premium theory on the yield curve and the examples. You can learn more about accounting from the following articles: –