Part of our Cost Classifications guide

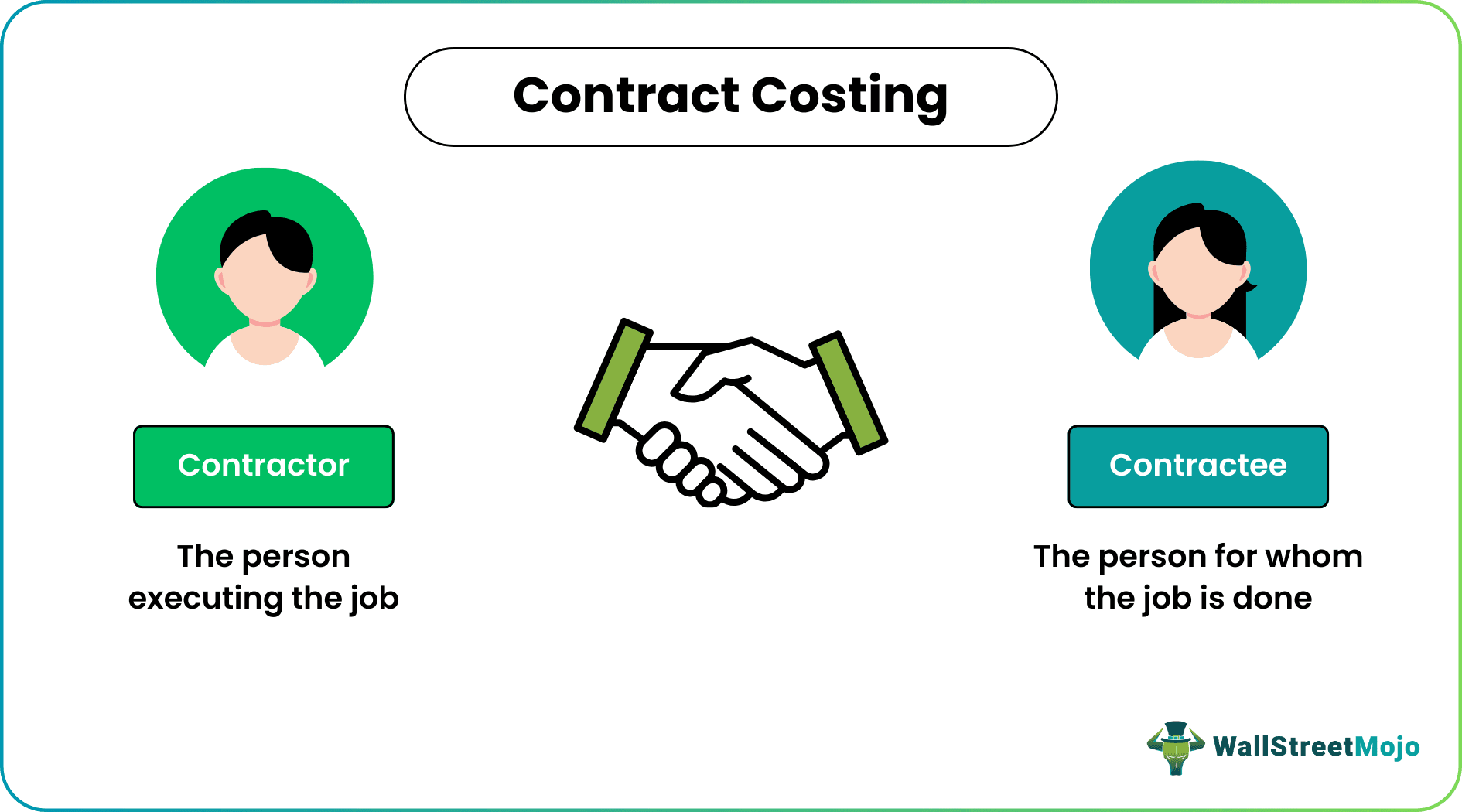

Contract Costing Meaning

Contract Costing is a contract made between two parties known as a contractor (i.e., the person executing the job) and contractee (i.e., the person for whom the job is done), wherein specific job orders are undertaken for a relatively larger time frame, which may take years to complete, and the billing for the same is done after completion of each milestone in the contract.

Features of Contract Costing

- Due to a larger time frame (taking more than one year for completion) involved in each contract, the contractor undertakes a smaller quantum of contracts during the year.

- The execution of work is required at the work site.

- Each customer has a separate account maintained to track work done, progress billings & amounts received to date.

- Direct expenses include the cost of material, labor, electricity, telephone charges, insurance expenses, consumables, depreciation, or hire charges of machinery used for the contract.

- The certificate decides the progress billings from experts, wherein work completion is specified. The proportionate billing is done accordingly.

- It also has a special aspect of retention money given by customers to contractors after examining the quality of the overall contract.

- There is also a penalty clause in a few contracts, which is to be paid by the contractor to the customer if he cannot complete the contract within the time frame.

- Each contract is executed as per the customer’s customization or specifications, and hence, each contract is different.

- It’s not the cost of material & labor involved in the relevant contract, but the work completed to date is relevant.

- Substantial risk is involved in the contracts.

Example of Contract Costing

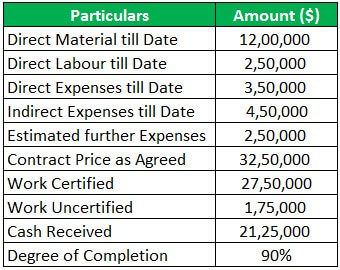

Let’s have following details for calculation purpose –

Solution

Explanation

- All costs incurred to date have been considered. The amount of expenses yet to be incurred is added to arrive at the total estimated cost.

- From an accounting point of view, we are more concerned with the total estimated cost. This is compared with the contract price to arrive at the estimated profit for the year.

- Revenue is recognized based on the degree of completion, as specified by the expert. Using the revenue & estimated total cost, we have arrived at a notional profit from the contract.

- Using the revenue figure, we calculated further billing to the contractor.

Types of Contract Costing

The three types of contracts are explained further –

Specific Aspects of Contract Costing

There are specific terms associated with contract costing that is usually helpful in calculating the cost involved in the contract:

- Work-in-progress is an important aspect of contract costing. This refers to the amount of pending work & not yet completed as on a specific date. In the balance sheet, the cost of completed & certified (by the expert) and the amount of profit earned in presented under the head “Certified Work-in-progress.” Also, the value of uncertified work includes the cost of work not yet certified, the cost of labor, material, and other expenses connected with the contract.

- The cost of certified work is decided per the milestones set in the contract. Thus, experts such as architects, engineers, surveyors, etc., are appointed to certify the work completed. As per the work completion, the revenue is recognized by the contractor.

- As per the work completion criteria, the contractor is set to receive the progress payments from the customer. The contract longs for a considerable period & the working capital is invested in the contract by the contractor. Thus, it is always suggested to have a policy of progress payments.

- The contractor/customer keeps some amount of money with himself as retention money (or security deposit), ensuring that the work is carried out as per the plan decided in the contract & the end work is defect free. The amount is used to settle any discrepancies between the two parties.

- Profits are estimated at two stages. When work certified by the contractor is called a notional profit, one at a time. After completion of the whole contract, the actual profit is calculated.

Advantages

- The contractor controls the costs involved in the contract for labor, material, other fixed expenses, etc.

- A contract account is prepared for each customer, identifying the cost incurred to date & work completion.

- Control is also maintained over the defects arising out of quality deficiency.

- Expert advice is helpless in completing a contract & he also helps to identify defects before completing the whole contract.

- Retention money becomes a reason for inspiration to provide quality work.

- A team spirit is built.

vantages

- The biggest disadvantage is that it is time-consuming.

- Each customer may not agree with the escalation clause.

- Lack of accounting may lead to improper calculation of profits.

- Lack of control may make the contract lose-making for the contractor.

- A continuous eye on market conditions is required.

- Larger time gives rise to complications in the completion of work.

Recommended Articles

This has been a guide to Contract Costing and its meaning. Here we discuss features, types of contract costing, an example, importance, advantages, disadvantages, and differences. You can learn more about financial analysis from the following articles –