What is Transfer Pricing?

Transfer pricing is the price determined for the transactions between two or more related entities within a multi-company organization. This price is also known as the cost of transfer which shows the value of such transfer between the related entities in terms of goods or even transfer of employees or labor across different departments.

The introduction of this concept has eliminated improper pricing of related party transactions between associate enterprises, making way for the elimination of tax evasion through such methods assisting the government and tax authorities. However, as this concept is relatively new, various changes need to be made to provisions over time based on its nature of the use to make it a globally accepted principle.

Transfer Pricing Explained

Transfer pricing at a corporate level refers to the transactions of goods and services between two entities owned by a single parent company. Multinational companies take advantage of different tax regimes in different countries of their operations and to allocate their profits at the end of a financial year to boost their retained earnings after tax.

Article 9 describes the rules for determining the arms-length transaction prices for related party transactions between associated enterprises in the OECD Model Tax Convention. Such an arm’s length price is fairly a market price for such a commodity or service. This price is widely accepted by tax authorities and users of financial statements. It assists entities in determining their real income.

The transfer price agreement is vastly related to the market price of the product or service involved in such related party transactions. This will eliminate the entities purchasing or selling such products or services in the market as they can buy or sell them between the related parties at the market price itself; this is the reason it is more of an accounting concept that accounts for the transaction between such related entities at a correct and fair price.

This is determined based on a few widely accepted methods such as comparable uncontrolled price, cost-plus pricing, resale price, Transactional Net margin, and transactional profit split methods.

The above-listed methods are used based on the transaction, such as if there are comparable products or services in the market for which there is a market price determined, then such price could be used to determine Transfer Pricing. Similarly, if the product is resaleable and such resale price is determined along with profit on such sale, then the resale price method can be utilized. Related entities use other methods.

Objectives

Let us understand the transfer pricing agreement through getting to know their objectives from the explanation below.

- True and fair reporting of financial statements

- Better estimation of profits generated by entities from associated transfers

- Avoidance of double taxation and avoiding tax evasion by entities

- Promoting competitiveness among the associated enterprises.

Examples

Let us understand different transfer pricing methods with the help of a couple of examples.

Example #1

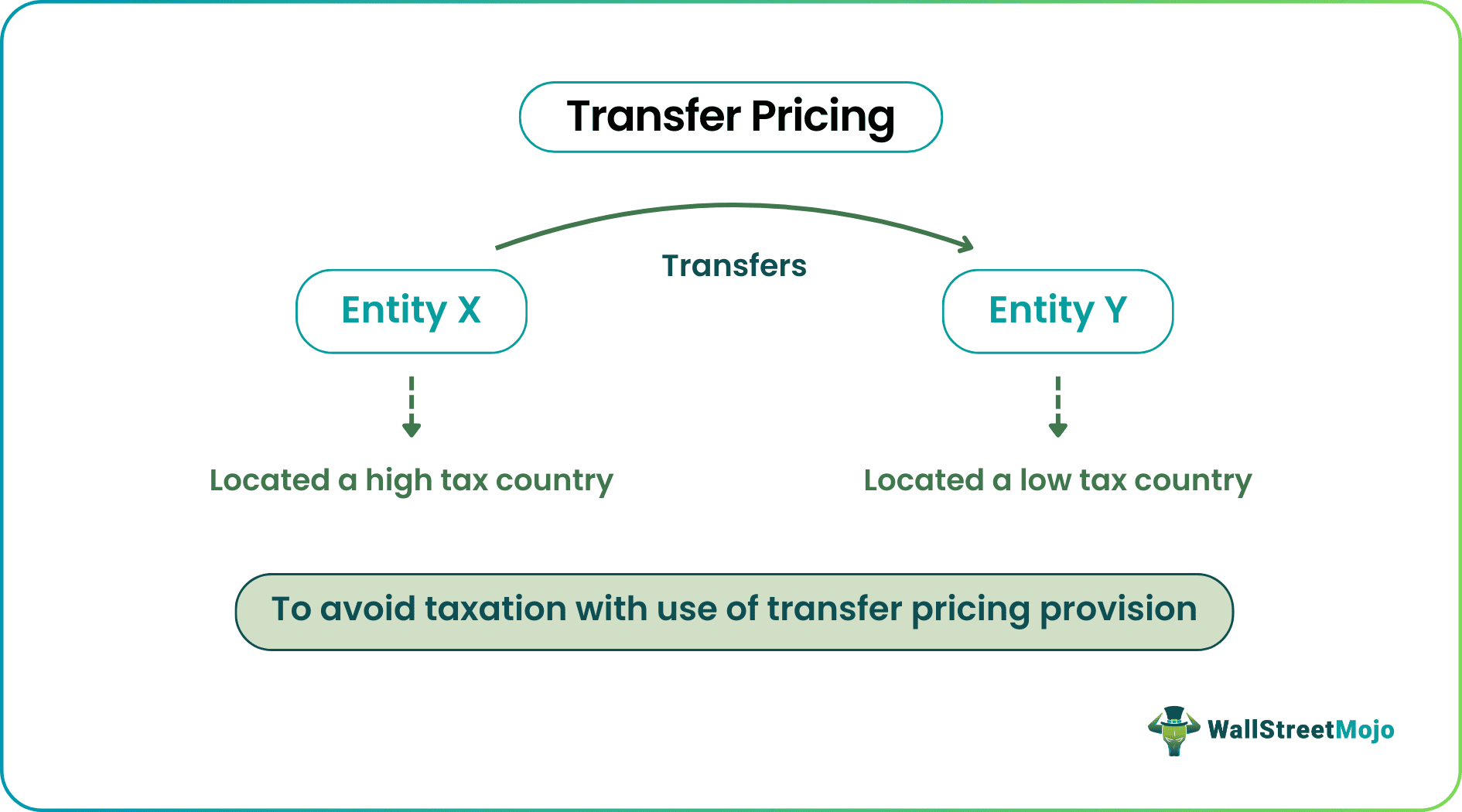

Two associated entities X and Y, where X is situated in a high tax country. On the other hand, y is located in a Low tax country which is a tax haven destination; in this case, X would shift most of the revenue generated to Y through means of some associated transfers to avoid taxation or reduce the incidence of tax for the company, with the use of these provisions, such type of tax avoidance transactions could be eliminated. Similarly, due to this, there will not be the eradication of revenue from one country to another by benefiting the country of source of generating such revenue.

Example #2

The assembly division of an automobile company, ABC Company, offers to purchase 50,000 tires from the tire division of the same company for $100 per unit. The production costs per tire at a volume of 200,000 tires per year are as follows:

| Item | Production Cost ($) |

|---|---|

| Direct materials | 50 |

| Direct labor | 20 |

| Variable factory overhead | 12 |

| Fixed factory overhead | 42 |

| Total | 124 |

The tire division typically sells 200,000 tires every year to arm’s length customers at $140 per unit. In addition, the capacity of the tire division is 300,000 batteries/year. The assembly division typically buys the tires from arm’s length suppliers at $125 per unit.

Now, the question is whether or not the tire division manager should accept the offer? If yes, how will the company benefit from this internal transfer?

The tire division has a surplus capacity of (300,000-200,000) = 100,000 tires per year. So the relevant costs to the tire division will be $82 / battery (total of $124 minus the fixed factory overhead of $42).

And the increased margin to the tire division would be 50,000*$(100 –82) = $0.9 million.

Due to the above benefits to the tire division, its manager must undoubtedly accept the offer.

The assembly division pays $125 to external suppliers for a tire that could be purchased internally at an incremental cost of just $82. So, the overall cost saved by the company would be 50,000 * $(125–82) = $2.15 million per year.

This is how the company will benefit from the internal transfer.

Now, what should be the price range in this case?

The transfer price should be kept between $82 and $125. If it goes below $82, the tire division will be at a loss, while if it goes beyond $125, the assembly division will be paying more than what it pays to the external suppliers.

On which legal entities should the practice of transfer pricing be applied?

The entities which can adopt this practice must be legally related entities. In other words, if two companies are owned wholly or with the majority by the parent corporation, then those companies can be considered to be under the control of a single corporation. And since they are under the control of a single corporation, they are also legally related entities, and hence, transfer pricing can be applied to them and can be practiced by them.

Under certain jurisdictions, entities are considered under common control if they share family members on their boards of directors even though they may not be related legally, as described in the above paragraph.

Importance

Transfer pricing methods prove to be extremely useful for individuals and multinational companies alike. Let us understand how through the discussion below.

- The critical importance of Transfer Pricing provisions is that there will be an equal and fair distribution of resources between associated entities leading to non-discriminatory trade transactions.

- This provides opportunities for associated enterprises to transact business between them as the transactions are valued at market price; this will enhance the scope of business and have a positive impact on the group company as a whole due to internal profits generated by these associated entities,

- Also, it is useful for the tax authorities to determine the actual value of such transactions and estimate the profits derived from such transactions taking place between associate entities. Without transfer pricing provision, there would be a reduction or avoidance of tax by misleading authorities and transferring or reporting profits based on the limitation presented in tax provisions.

- It is used not only by multi-company organizations but also by entities that satisfy the conditions of associated enterprises.

Purpose

Let us understand the purpose of a transfer pricing agreement through the discussion below.

- Determination of a fair and equitable price of a transaction that takes place between two related enterprises involving the purchase and sale of goods and services;

- Other purposes include accounting for a transaction as per its market price, avoiding any collusion among associated enterprises, and providing a base for estimating income generated from such transactions. Also, this concept is useful for true and fair reporting of transactions between associated enterprises in the financial statements of such entities.

Functions and Risks

Regardless of transfer pricing methods being useful for individuals and MNCs, it also has its share of risks and intricate detailing to it. Let us understand them through the discussion below.

- This concept functions basically on the principles of price determination that is available in the market for such commodities or services involved in the transaction.

- Due to such a function, there are few risks involved, such as the valuation of those transactions that involve the use of intellectual property, services that are highly valued, and transactions that are not of financial nature. The exchange of goods and services with unrelated goods and services between associated enterprises, etc.

- Also, there is a risk of mispricing a self-generated commodity or service that is not related to any other resource in the market due to limitations present in domestic pricing rules.

Benefits

Let us discuss the importance of inculcating transfer pricing methods through the points below.

- Assists the entities to transact at market prices eliminating inconsistency in pricing a transaction.

- It helps the tax authorities to determine taxes and helps reduce tax evasion.

- Fair presentation of financial statements

Drawbacks

To understand the transfer pricing agreement completely it is important to understand its drawbacks as well. Let us do so through the explanation below.

- This would require additional administrative costs and a time-consuming process.

- There are few limitations in determining arm’s-length prices as two products cannot be compared due to the homogenous nature of such commodities or services.

Recommended Articles

This article has been a guide to what is Transfer Pricing. Here we explain its examples, objectives, purpose, benefits, and drawbacks in detail. Also, discuss its advantages, disadvantages, and how it works. You can learn more about it from the following articles –