Part of our Cost Classifications guide

What Is The Cost Method?

Cost Method is one of the most conservatives methods of accounting for investments where the investment stays on the balance sheet at its original cost, unlike the fair value or revaluation method where the market factors and various internal management models are used for determining the fair value. This method is used for many financial instruments accounting such as investments and inventory/fixed assets.

- In investment accounting, the cost method is used when the investor holds less than 20% in the company, and the investment has no significant fair value determination.

- In inventory and fixed assets accounting, this method is used in the initial recognition of assets.

How Does The Cost Method Work?

The cost of investment/inventory/fixed assets is shown as an asset in thestatement of financial position. Once the asset is sold down, any gain/loss is recognized in the income statement.

All the above inflows and outflows also affect the cash flow statement, which impacts investing cash flows in the case of investments and fixed assets and operating cash flows in the case of inventory.

All these instruments are also tested for impairment when there are either external or internal indicators of impairment and written down to recoverable value in the balance sheet. The impairment allowance is recognized in the income statement immediately.

Cost Method Examples

Example #1

John PLC acquires a 10% interest in Robert PLC for £2,000,000. In the most recent reporting period, Robert PLC recognizes $200,000 of net income and issues dividends of £40,000. Under the requirements of the cost method, John PLC records its initial investment of £2,000,000 as an asset and its 10% share of the £40,000 in dividends. John PLC does not make any other entries.

Example #2

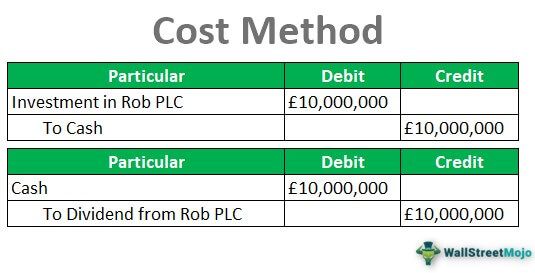

John PLC purchases 15% of Rob PLC for £10,000,000. At the end of the year, Rob PLC paid out a dividend of £100,000 to its shareholders.

Since the above purchase qualifies for cost method of accounting (less than 20% interest), the purchase of investment was recorded as an asset in the balance sheet as per the cost method of investment accounting. The Journal entries are shown below:

At the end of the year, John receives 15% of the £100,000 dividends as per its shareholding pattern:

Advantages

- There is much less paperwork with the cost method than with other accounting methods. Since most transactions are recorded only once until the asset is sold, the time and cost associated with the record-keeping compared to other methods are very less.

- The investment is recorded at a historical cost, which is the purchase price. It is a one-line entry on the balance sheet. No adjustments are made unless the value or recoverable amount of the asset decreases. Then a permanent write-off for the asset is recorded through impairment.

- Dividends received from the equity investment, and any direct payments received resulting from any distribution of net profits from the investee are recorded separately on the income statement. These are not deducted from the value of the equity investment.

- So, they do not affect the carrying value of the investment. The advantage of recording the dividends received or distributions received from the investee on the income statement is that the value of the equity investment is not decreased, and the amount received is considered income and affect cash flow.

- Undistributed earnings from the equity investors do not affect the balance sheet of the investing company because they have not been received and are not recorded until they are received. All data and records are supported by evidence in the form of sales/purchase receipts and invoices. There is no room for manipulation of facts.

Disadvantages

- The investing company records the investment at the original purchase price without adjustments for the change in fair value. This accounting system does not record fair value fluctuations or the current market value of the equity investment asset unless there is a substantial decrease in value below the purchase cost, which is recorded as impairment.

- This method does not record gains until the gains are realized. The original purchase price remains the value of the equity investment asset until it is sold when a gain or loss is realized. It can be a disadvantage when the value of the investment increases but does not affect the income side of the balance sheet.

- This method cannot inflate or deflate the income side of the balance sheet with unrealized gain or loss as the equity investments undergoes any changes in upward/downward movement in fair value.

- Any undistributed earnings or dividends not yet received from the equity investment are not recorded. They do not affect the investing company’s balance sheet or the final consolidated balance sheet of the investee and the investing company. It does not record the expected income. The earnings must be received before they can be recorded.

- This accounting method does not consider inflation. The cost method of accounting assumes that the value of the currency with which the equity investment was purchased remains constant over time.

Changes in Cost Method of Accounting

When we change the recognition of financial instruments from cost to equity/revaluation method or vice versa, the same is regarded as changes in accounting policy as per the provisions of IAS-8. When such change happens due to change in any standard, the standard’s transitional requirements need to be adhered to, but if such change is done voluntarily, the same needs to be applied retrospectively by restating and adjusting prior periods.

Recommended Articles

This article has been a guide to What is the Cost Method and its Definition. Here we discuss the cost method of journal entries along with practical examples. You can learn more about excel modeling from the following articles –

- Cost of Quality

- LIFO Method of Accounting

- FIFO Method of Accounting

- Investment in Associates Definition

Recommended Articles

Continue with these closely related articles from the same guide.