Part of our Banking Services and Operations guide

What Is Digital Remittance?

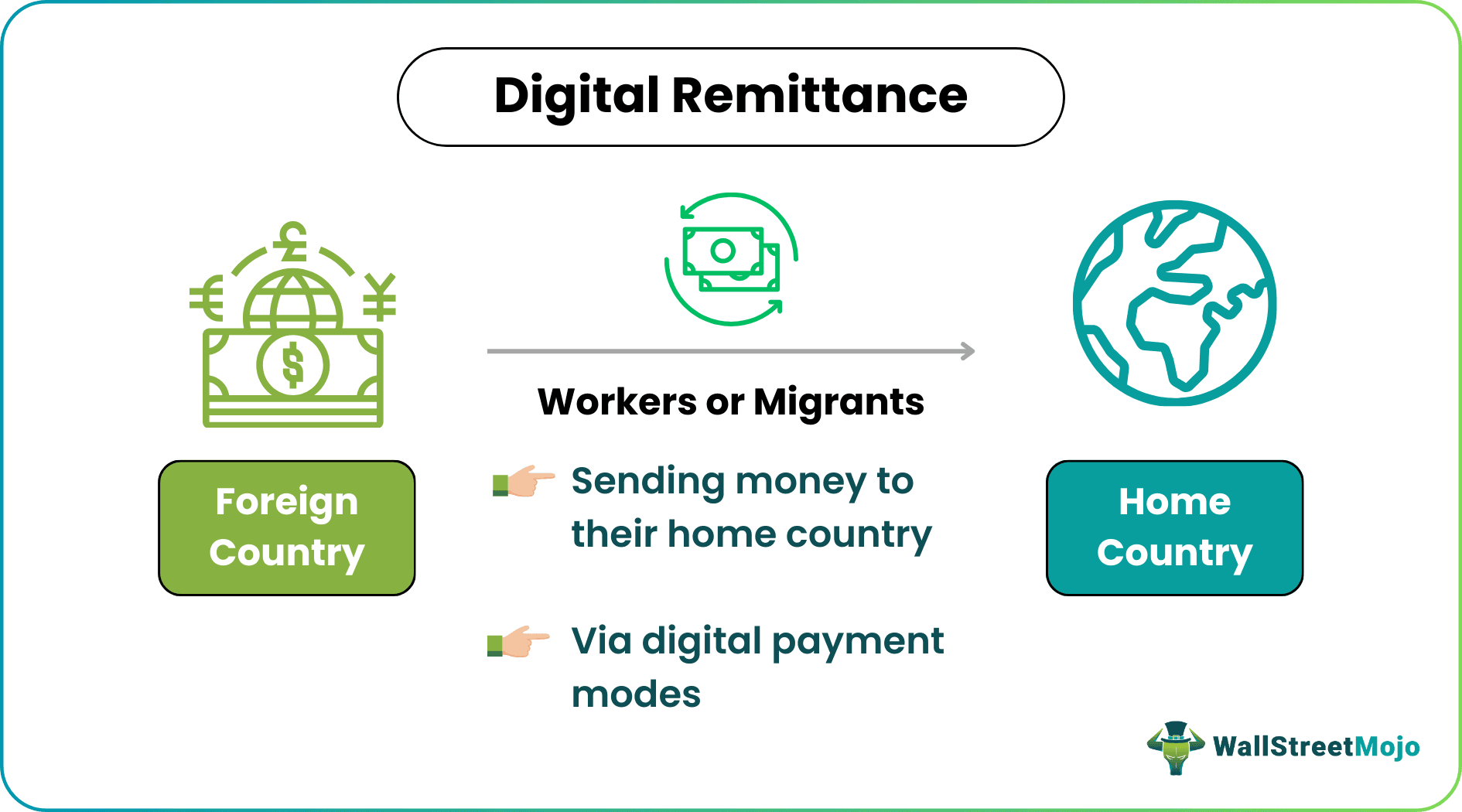

Digital Remittance is the process using which workers, who have migrated to foreign countries for work, send money to their home countries using electronic modes of payment. It is done via online payment modes or through mobile applications connected with bank accounts or digital wallets. These are international transactions that do not involve the transfer of cash.

The process of money transfer from one country to another is riddled with several legal complications and compliance issues. Hence, to streamline the money transfer activity, the migrant population in various countries uses digital remittance services to send a percentage of their earnings back to their home countries. This is because these services offer convenience and security. Such facilities make providing remote family support possible despite various cross-border money transfer challenges.

- Digital remittance enables convenient, fast, and cost-effective cross-border money transfers. It promotes financial inclusion and makes money transfers transparent and reliable.

- Navigating legal and regulatory environments is vital to ensuring effective digital money transfer processes.

- Online remittance procedures differ from traditional remittance in terms of mode, speed, convenience, cost, and accessibility, among others.

- The advantages of using online modes of money transfer include convenience, speed, low costs, and accessibility. The disadvantages include reliance on digital infrastructure, security risks, and regulatory challenges.

- The economy benefits from digital remittance because it lowers transaction costs, promotes financial inclusion, improves the flow of money, and helps economies grow.

Digital Remittance Explained

Digital remittance refers to electronic money transfers across nations, eliminating the need for hard currency or paper-based transactions. People can safely send money to family, friends, or business partners through mobile applications or via online payment portals or platforms. Sending money is easy and convenient with online remittance options, as trips to banks or remittance centers are not required.

Recipients swiftly receive funds because transactions are often faster than conventional payment methods. The fees and currency rates associated with digital remittance services are lower than traditional remittance services, which lowers the overall expense of sending money across international borders.

International money transfers are becoming simpler and quicker because of fintech and digital payment technologies like blockchain, mobile wallets, and immediate payment services. However, regulatory issues and compliance standards are major barriers to the digital remittance market. For instance, Know Your Customer (KYC), Anti-money Laundering (AML) guidelines, and transaction screening are crucial steps for successful money transfers on an international scale.

Governments, financial authorities, and regulatory agencies enforce regulations to deter entities from engaging in terrorist financing, money laundering, smuggling, and other illegal activities. For remittance service providers, ensuring compliance with these stipulations proves expensive and challenging. This is because they need solid, almost impenetrable processes for end-to-end compliance.

Overall, the economy benefits from these services due to lower transaction costs, higher financial inclusion, easier money flow, and more all-round growth compared to other payment methods. Such services make financial services accessible to everyone, empowering individuals at all levels and promoting comprehensive economic growth. The expansion of these services is essential to building robust and inclusive economies.

Examples

Let us study a few examples to understand the concept better.

Example #1

Suppose Laura is a foreign worker in the US. She lives away from her family based in the Philippines. Usually, she brings the money she saves to her family when she visits them. However, Laura received a call from her family telling her that her mother was hospitalized. She could not fly back to them immediately, but she needed to send funds as soon as possible.

Laura decided to use a mobile app to send money back to her family. She found this method convenient, cost-effective, and secure, as she could execute the money transfer without incurring exorbitant fees or exchange rate losses.

Example #2

A blog published in 2019 by the World Bank stated that the access to financial instruments and financial management tools have been improved for many countries worldwide, giving rise to a slew of digital services.

For millions of families, including those with modest or low incomes, remittances are crucial. In 2018, these services facilitated fund transfers to the tune of $600 billion worldwide, with $466 billion being sent to low- and middle-income nations.

This shows remittances improve financial health since they are frequently the first financial product used by those with low incomes. They also serve as a gateway to a variety of other financial services.

Advantages And Disadvantages

The advantages and disadvantages of these services have been discussed below:

Advantages

- Convenience and Accessibility: It is convenient and accessible since such transactions can be initiated and completed using mobile apps or online platforms from any location and at any time. Hence, physical visits to remittance centers have become redundant.

- Faster Transaction Processing: It offers faster transaction processing, helping recipients receive funds within a short time, particularly in emergencies.

- Reduced Fees and Exchange Rates: When compared to traditional remittance methods, digital remittance services often provide more competitive exchange rates and reduced transaction fees. This maximizes the value of the transfer itself for senders and recipients as transaction processing fees are lower than other forms of payment.

- Enhanced Financial Inclusion: It improves the socioeconomic status of workers and their families by giving them access to financial services and establishing financial histories.

- Transparency and Transaction Tracking: By providing digital receipts, these platforms improve transaction tracking and the transparency of money transfers. Through transaction status tracking, senders and recipients can ensure accountability and lower the possibility of mistakes or disputes.

Disadvantages

- Dependence on Internet Connectivity and Robust Digital Infrastructure: Digital remittances depend heavily on the internet and need a strong digital infrastructure. People in places with patchy internet connectivity or inadequate infrastructure may find it difficult to send or receive money via online modes. Also, people who are not comfortable with technology or are less tech-savvy find dealing with such platforms difficult.

- Potential Security Issues and Fraud: These transactions are digital. Fraud and security issues are definite concerns in this domain. Cybercriminals may try to gain unlawful access to private financial data, intercept transactions, or assume the identity of senders or recipients. In order to reduce these threats, strong security measures are essential.

- Restricted Availability of Services: Despite the global expansion of digital remittance services, certain geographical areas or regions continue to have limited access to these services. Some countries impose stringent regulations, and the adoption of digital financial services in some countries is slow or negligible.

- Possibility of Dependency on Outside Platforms: To facilitate transactions, service providers often use intermediaries or third-party platforms. This creates a dependence on external systems, and any malfunctions or interruptions in their functioning could affect the accuracy and reliability of remittance transfers.

- Difficulties with Regulation and Compliance: The regulatory environment in which digital remittances function differs depending on the country. Service providers may face difficulties in adhering to various rules, including those pertaining to AML and KYC requirements.

Digital Remittance vs Traditional Remittance

The differences between digital and traditional remittance are listed below.

- Mode of transfer: Digital remittance uses online platforms, such as apps or websites, while traditional remittance requires visiting banks, financial institutions, or other remittance centers in person.

- Speed: Online services are usually faster than traditional remittances. This is because traditional methods undergo many processes, including manual checks and approvals, to achieve the same result.

- Convenience: Digital remittance is more convenient because these transactions can be executed using mobile apps or websites.

- Cost: These are often cheaper with better exchange rates compared to traditional remittances.

- Accessibility: Digital remittance platforms are available to people who may not have a bank account, while traditional remittance services may require a base bank account with which transactions will be linked.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

1.What is the future of the digital remittance market?

<p>This industry has a bright future, with steady growth anticipated in the coming years. Its growth is attributed to a number of factors, including growing globalization, technological developments, and the demand for quick and easy cross-border money transfers.</p>

2.What are the key drivers of digital remittance services?

<p>The need for digital remittances is being driven by a number of factors, such as the increasing number of migrants, the globalization of businesses, better and faster internet connectivity, and the need for more rapid and affordable money transfer options.</p>

3.Which new opportunities did digital remittance bring to the market?

<p>With cutting-edge payment options, the following developments have taken place: <br/>- Financial inclusion for unbanked people,<br/>- Improved money transfer processes that promote economic growth,<br/>- Ease of cross-border commerce and investment.</p>

4.What is the role of technology in boosting the digital remittance market?

<p>The market for digital remittances is driven entirely by technology. Among the technologies used to improve the security, speed, reliability, scalability, accessibility, and efficiency of digital remittance services are mobile apps, internet platforms, blockchain, and artificial intelligence.</p>

Recommended Articles

This article has been a guide to what is Digital Remittance. We explain it with its examples, advantages, disadvantages, and comparison with traditional remittance. You may also find some useful articles here –

Recommended Articles

This article has been a guide to what is Digital Remittance. We explain it with its examples, advantages, disadvantages, and comparison with traditional remittance. You may also find some useful articles here –