ACH Debit Meaning

An ACH Debit is a kind of electronic transaction that allows a receiver the authorization to directly pull money from a payer’s account. So, for example, a customer who needs to make payments for recurring supplies can opt for this service to pay with fewer hassles.

ACH or Automated Clearing House is a network that enables the electronic transaction of money across the United States. The ACH payments are electronic forms of payments that can make money transfers automatically without having to write out paper checks or initiate credit or debit card transactions.

- With an ACH debit transaction, the money moves automatically from the payer’s account to the payee’s account rather than writing out the paper check or initiating some debit or credit card transaction.

- ACH debits are most commonly used for recurring or monthly payments to a frequent biller.

- Several kinds of fees are associated with ACH Debits, such as transaction fees, debit return charges, account setup charges, etc.

- While in an ACH credit transaction, the bank would instantly initiate the transfer, in an ACH debit transaction, the bank would send the money only when it receives the request from the receiver bank.

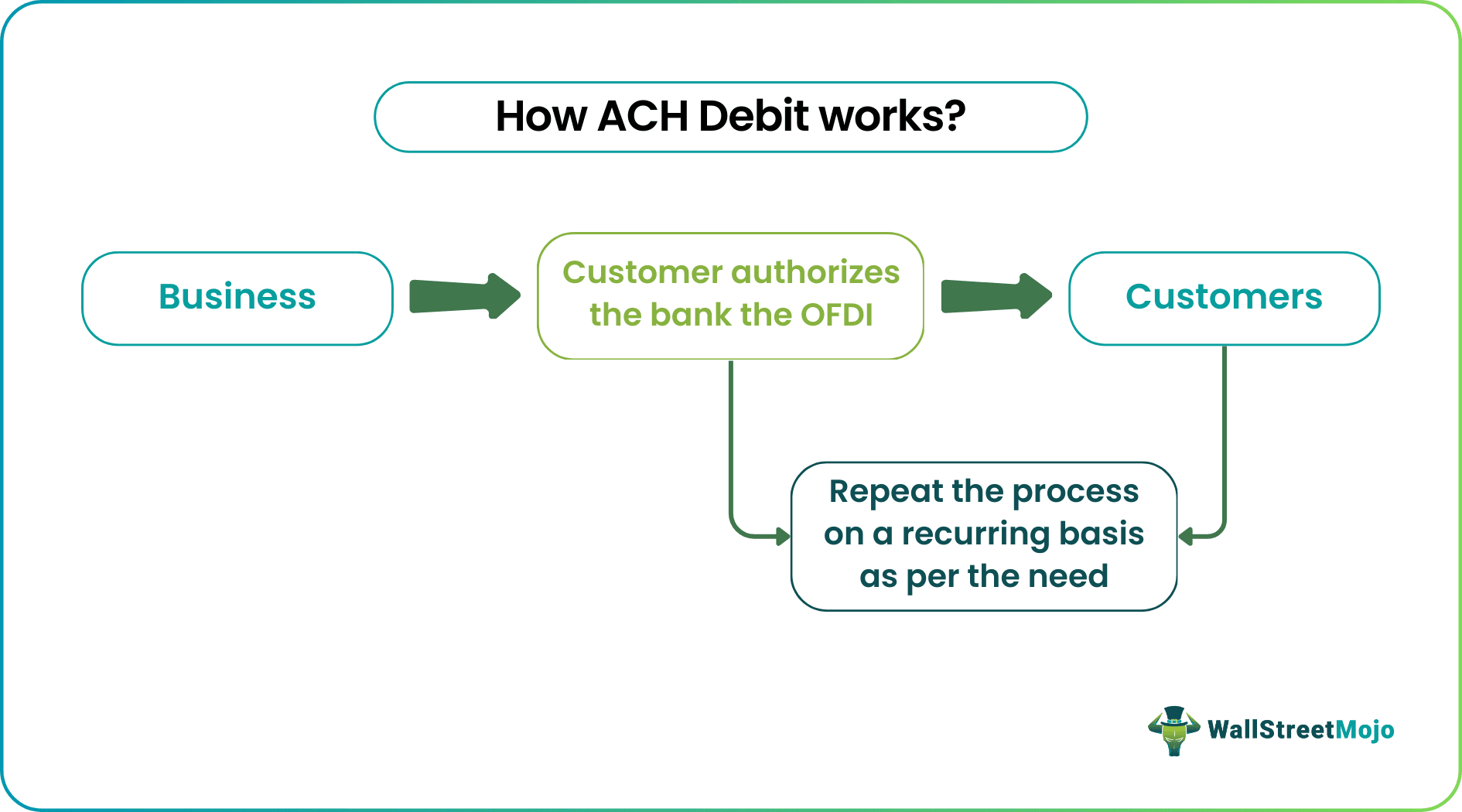

How does it Work?

ACH debit mode can improve the ease and convenience of making regular payments. The Automatic Clearing House network is responsible for connecting over 25,000 banks and other financial institutions for enabling money’s electronic movement between different accounts throughout the country. Most of the transactions in the respective ACH network tend to be ACH debits. It is also referred to as direct payments. People use them most frequently for setting up a recurring bill between the biller and the customer.

The transactions involving ACH debits tend to occur when the transaction’s originator would authorize the recipient to take out or pull funds from the respective account.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Example

For instance, let us assume that a customer would want to ensure the payment of the electricity bill with the help of ACH debit. Here, the customer serves as the transaction’s originator, and the bank is the OFDI (Originating Financial Depository Institution). The customer would authorize the bank, the OFDI, to transmit or transfer money from the respective account to the recipient’s account upon the recipient’s request.

The transaction would then follow the given set of steps. The bank of the electricity company, known as the RFDI (Receiving Financial Depository Institution), uses routing the customer along with the respective account number for sending requests via some clearing house like the Federal Reserve. Then, they make the request to contact the OFDI while transferring the funds. As the OFDI has already received the respective authorities to carry out the transaction from the given customer, the funds are then extracted or pulled out from the customer’s account to the account of the electricity company on the stipulated date.

If the customer sets up recurring billing, then he or she has given authorization for the regular pulling out or withdrawal of the available funds from the account. As such, the given process would continue every month.

ACH Debit Return Charges

ACH debit payment involves several kinds of fees to make the process smooth and seamless. Two of them are the fee to set up the recurring transaction and the debit fee for the transaction. Yet another charge is the returned payment fees. Automatic payment transactions can fail due to several reasons. One of them is insufficient funds in the sender’s bank account. Providing wrong bank account details, account freezing, stopping payment, etc., can be other reasons for unsuccessful transactions. The RDFI, in this case, notify the ODFI of the return. The fee in this case is the ACH debit return charge.

Advantages & Disadvantages

Some of the benefits of ACH debits are:

- Time-saving – by not having to manually pay for a recurring expense each time, and instead of taking the help of an automatic process, it saves a lot of time for a business or a customer.

- Timely payments – It ensures that you don’t need to remember to make the payment every single time. Moreover, payments by check take time to get credited to the receiver’s account.

- Low-cost – it reduces processing fees that could come off by making payments through cards.

- Comfort – It all increases overall comfort with comes from not worrying about the payments.

While ACH debits tend to feature a myriad of benefits, there are some drawbacks to it as well. Some points are:

- The person is handing over information about the respective bank account, including the bank account number. Thus they are essentailly providing other parties access to their account information.

- A single bill error that might occur by accident could be a costly and timely problem.

- One may lose track of ACH payments and not have enough funds in their account once the ACH clears.

ACH Debit VS Credit

The main difference between the two types of transactions is this; In the case of an ACH credit transaction, the bank would instantly transfer funds upon the payer’s request. But, in the case of ACH debits, the bank will proceed with sending the funds upon the recipient’s request. The ACH credit transactions get “pushed” into the respective account, and the ACH debit transaction involves the “pulling out” of the funds from the respective account.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What are ACH debit return charges?

When a payment is bounced or insufficient funds in the bank account, the bank or service provider can charge a return fee. The transaction can also go uncompleted due to incorrect bank information.

How does ACH debit works?

An ACH debit allows a customer to make recurring payments of bills with the help of easy electronic transfer. First, the customer can authorize their bank to allow ACH transfer. Then, the receiver bank can send a request to the customer’s bank account when it is time for the payment. Upon receiving the request, the sender’s bank account confirms and initiates the money transaction. This process can repeat itself as long as the customer intends to.

How to stop ACH debit?

To stop an ACH debit payment, the person can initiate a stop order to the sender bank. Thus, the person can revoke the authorization by letting the bank and the biller know that he/she no longer intends to continue the payment. They should notify this several days before the payment as per the bank proceedings.

Recommended Articles

This has been a guide to ACH debit payment and ACH debit transaction. We discuss how it works with an example, return charges, and ACH debit vs credit.You may learn more about financing from the following articles –