What Is Earnings Management?

Earnings management refers to deliberate intercession by the management in reporting to deceive the stakeholders on the company’s economic and financial position or with the personal intention to gain income from contracts with these manipulated financial reports. Earnings management accounting can be excellent and evil; it is considered good when there is no personal intention.

The financial manager or management of a company chooses to exhibit only things in their financial reports that project their company in good status to gain profit from that. Earnings management is bad as most of the calculation of profit showed in the reports will be either fake or prepared based on uncertain future judgments.

Earnings Management Explained

Earnings management refers to the strategic manipulation of a company’s financial statements by its management to achieve specific financial objectives. While not inherently illegal, it can raise ethical concerns when used to mislead investors or portray a false image of a company’s financial health. Earnings management typically involves adjusting accounting policies, reserves, or other financial metrics to present financial results in a more favorable light.

One common form of earnings management involves smoothing income over multiple periods, making a company’s financial performance appear more consistent than it might be in reality. Managers may defer the recognition of expenses or accelerate revenue recognition to achieve this smoothing effect. Another method is the use of discretionary accruals, allowing management to adjust estimates of future expenses, revenue, or reserves.

While some level of discretion is inherent in financial reporting, excessive or inappropriate earnings management can erode the trust of investors and stakeholders. Companies must maintain transparency and adhere to ethical accounting practices to ensure the integrity of financial information.

Regulatory bodies and accounting standards, such as the Sarbanes-Oxley Act and the Generally Accepted Accounting Principles (GAAP), aim to mitigate earnings management theory by establishing guidelines for accurate and transparent financial reporting. Investors and analysts scrutinize financial statements to detect signs of potential earnings management and assess the actual financial performance of a company.

Purpose

The purpose of earnings management accounting cannot always be wrong; there are also some good reasons. Generally, it is bad as it is done for Personal gain from such activity as earning commission from obtaining a contract from a false report or increasing the stock value in the market by showing the company is highly profitable. A good reason can be moving the money for next year so that the company will be showing consistent profit instead of fluctuating between profit and loss.

Methods

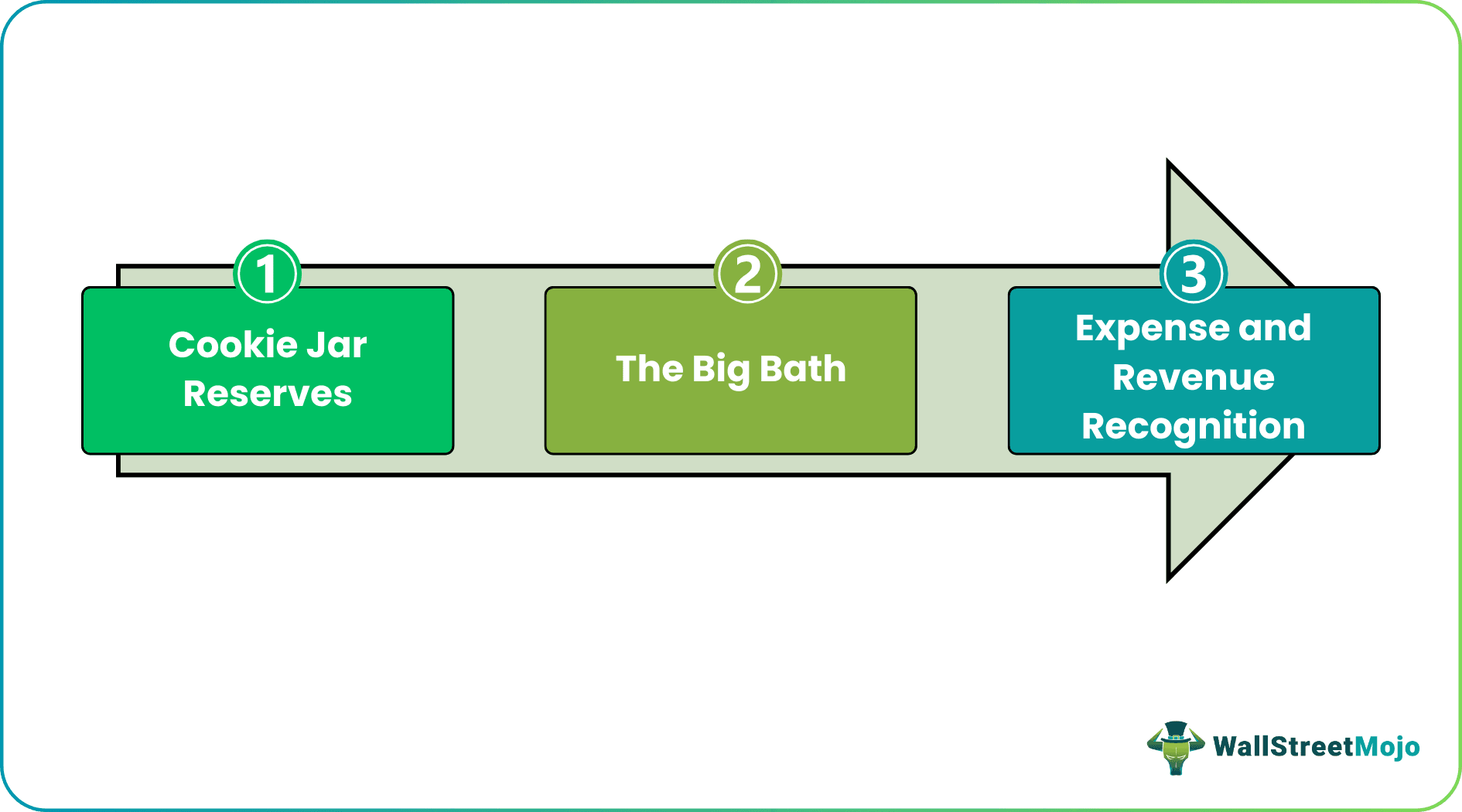

There are many methods of earnings management theory based on the size of the company and its financial status; commonly used models are as below:

#1 – Cookie Jar Reserves

Cookie jar reserves come under the technique of aggressive accounting. It deals with creating a significant reserve in the profit year and drawing down when the company faces a bad year, or bad debts can be underestimated in a year to show the company is making a profit.

#2 – The Big Bath

When a company is facing a stormy period due to external factors, it will affect its profit. It has to show it in its reports. Still, the company will make it even worse by writing off all bad debts, overvaluation of assets depreciation, restructuring costs, other expenses in the same year to show more loss and evade tax.

#3 – Expense and Revenue Recognition

It can also be called “Income Smoothing” This comes under fraudulent accounting as the company records its expenses before it incurs or does not show the profit and sales when earned. They can even accelerate the sales showing extra revenue, or they don’t recognize a bad debt in the current year and shifts it to next year as it reduces this year’s profit.

Revenue vs. Earnings Video Explanation

Examples

Now that we understand the basics, purpose, and methods of earnings management accounting, let us delve into the practical aspects of the concept through the examples below.

Example #1

If a company has $20,000 as bad debts and it is not recoverable, it has to be written off during this financial year. Still, the financial manager says to show $10,000 as debtors and write off the balance in the next financial year as this year’s profit is low. It comes under the type of expense and revenue recognition as an expense is not recognized correctly to inflate profit.

Example #2

The market is not stable due to external factors like high pricing, low demand, etc. a company can face losses. The company’s CEO asks to show all the losses in the same year, like unrecoverable debts, depreciation, high reserves, etc., as already the company is in a loss. So that the next financial year will be profitable, this is an example of The BIG BATH type of earnings management.

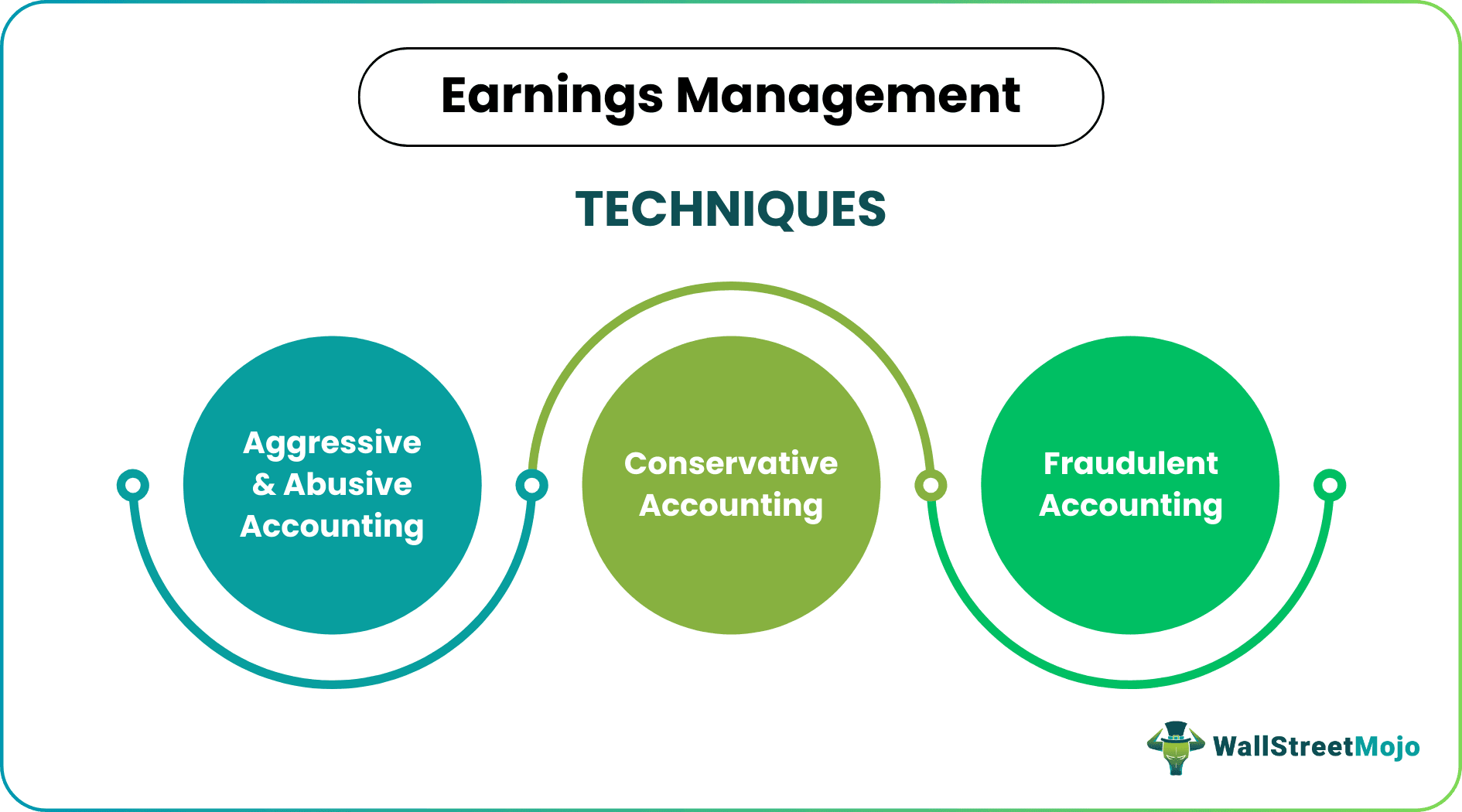

Techniques

There are three types of techniques in the earnings management theory they are;

- Aggressive & Abusive Accounting – refers to the aggressive escalation of sales or revenue recognition. Abusive accounting includes cookie jar, big bath, etc., to show there is a high profit that year.

- Conservative Accounting – Conservative accounting refers to writing off all the expenses and losses in the same year if the company makes a high profit and evades tax.

- Fraudulent Accounting – If revenue and losses are not shown in the reports to deceive stakeholders, or if high profit is shown to earn contracts, it comes under fraudulent accounting. It also violates the GAAP (Generally Accepted Accounting Principles).

How to Detect?

The Healy model (1985) is used to calculate the estimation of discretionary accruals used in earnings management.

- Where: NDA = Estimated non-discretionary accruals

- TA = Total accruals scaled by lagging assets

- t = 1, 2… T refers to years included in the period of estimation;

- t = year in the event period.

One method of detecting earnings management is shown above; there are other methods as well.

Consequences

Let us understand the consequences of businesses incorporating techniques of earnings management theory through the points below.

- Earnings management can mislead investors by presenting a distorted picture of a company’s financial health, leading to misguided investment decisions.

- Excessive manipulation erodes the credibility of a company’s financial statements, diminishing trust among investors, analysts, and stakeholders.

- Unethical earnings management practices may lead to legal consequences as regulatory bodies enforce penalties for fraudulent financial reporting.

- Inaccurate financial information can lead to mispricing of a company’s stock, affecting the valuation and creating volatility in the stock market.

- Consistent earnings management can result in long-term damage to a company’s reputation, impacting its ability to attract investors and partners.

- Investors may become wary of engaging with a company that practices earnings management, straining relationships and hindering capital-raising efforts.

- Earnings management can distort market perceptions, affecting overall market efficiency and the allocation of resources.

- In cases where widespread earnings management practices occur, there can be adverse effects on the broader economy, impacting investor confidence and economic stability.

Advantages And Disadvantages

Let us discuss both sides of this highly controversial topic of earnings management accounting through the advantages and disadvantages below.

Advantages

- Helps companies meet market expectations and analyst forecasts, maintaining or boosting investor confidence.

- Allows for the presentation of more stable and consistent financial results, potentially reducing stock price volatility.

- Assists in meeting debt covenant requirements, preventing potential financial penalties or adverse consequences.

Disadvantages

- Excessive manipulation undermines the credibility of financial statements, eroding trust among investors and stakeholders.

- Unethical earnings management can lead to legal consequences, including fines and penalties imposed by regulatory bodies.

- Distorted financial information can result in misinformed investment decisions, leading to the misallocation of resources in the market.

- Sustained earnings management can cause long-term damage to a company’s reputation, affecting its ability to attract investors and partners.

Recommended Articles

This has been a guide to what is Earnings Management. Here we discuss its techniques, methods, examples, purposes, advantages, and disadvantages. You can learn more about it from the following articles –