Creative Accounting Definition

Creative accounting is a method used to make or interpret accounting policies falsely to misuse the accounting techniques and standards being set by the accounting bodies. It is an exploitation of loopholes in our accounting system and audit system after the accounts are finalized.

The purpose of doing this type of practice is to make profits by not reporting the exact figures. There are many ways of doing it. The most popular ones are to manipulate the profit figures to eliminate excessive taxation in the future. Often, the books of accounts through which these tax figures are found are generally incorrect; the manipulation is done from the very primary level.

Creative Accounting Explained

Creative accounting is an accounting practice that helps the company deviate from the profits and revenues for the year by following rules and regulations. It is a skill that experts use to manipulate the company accounts. The experts best handle the loopholes in the system through creative accounting solutions, and the method should be ethical; otherwise, it can be a severe problem for the company’s management.

The most important thing here is that investors should be cautious while choosing investment companies. They should know the financial arrangements, which are possibly done by understanding the notes to the accounts. The management should ask about any suspicious item, and if the management cannot answer the query, the investor should not invest their money in these bogus companies.

The main adjustments regarding the accounts the management wants to manipulate are made by adjusting the figures related to employee benefits or incentives. Some companies practice creative accounting to pretend that the financial condition of their company is sound and people can invest in our companies.

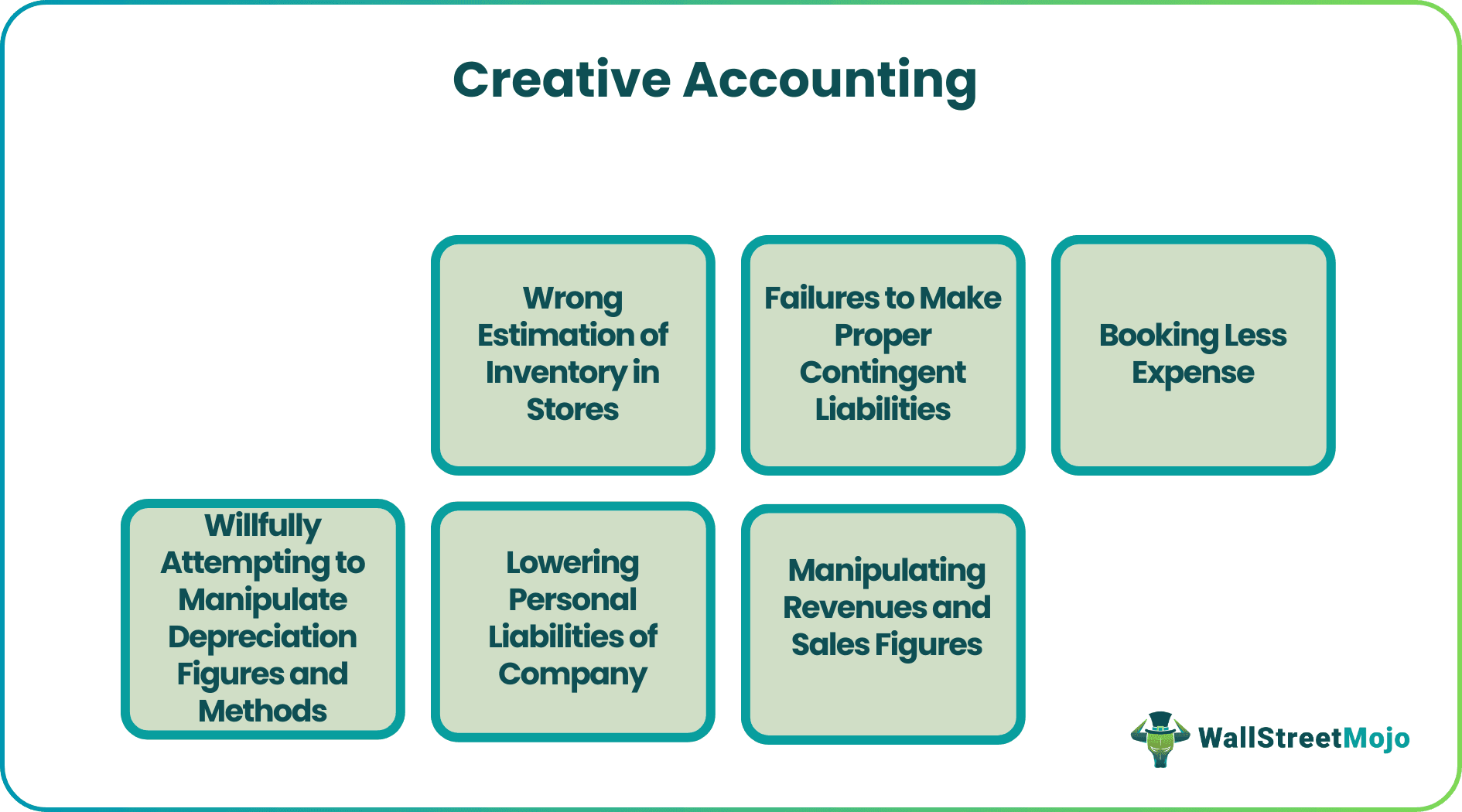

Methods

#1 – Wrong Estimation of Inventory in Stores

Some companies’ management does this type of practice to overstate the inventories’ valuation. They use creative accounting solutions to show that their cost of goods sold is understood and thus tries to show the increased profits their company will earn this year.

#2 – Failures to Make Proper Contingent Liabilities

It is a very technical method of creative accounting. The contingent liabilities are not shown properly in the notes to accounts; thus, it will give the impression that the company is not having any liability and thus is free from that.

#3 – Booking Less Expense

To show lower expenses, the company sometimes makes client payments by cash or an outdated cheque. It helps the management book the lower expenses per year, and their books of accounts will depict the fewer expenses figure, which may attract some investors.

#4 – Willfully Attempting to Manipulate Depreciation Figures and Methods

Many companies use this technique to make a good impression on their investors. The depreciation calculation method is sometimes changed by simply giving a disclaimer. No estimation increases the lifespan of the assets. The management attempts to set an arbitrary life span, usually more than expected. It thus can have a less depreciation calculated on the above and corresponding to that increases the salvage value of the assets company’s assets. Although depreciation is cashless, the calculation of the same greatly impacts the company’s finances.

#5 – Lowering Personal Liabilities of the Company

A company does not usually tend to show its liability, so it is also a great creative accounting technique.

#6 – Manipulating Revenues and Sales Figures

It is a very basic thing most companies are doing. Sometimes they lower the sales revenue in their books to get rid of taxes, and sometimes they increase the sales figure with some arbitrary transaction to show the company’s revenue to encourage their investors.

Examples

- The company raises invoices before the end of the accounting year to inflate its sales figures, but the actual transaction occurs on the post date. It is an example of creative accounting book where the company attempts to show the boosted revenue figures.

- The company sometimes gives loans to their known person to willfully hide the transactions made during the year.

- The company arbitrarily increases an asset’s useful life to get rid of the higher depreciation charged.

Objectives

Let us understand why this concept of creative accounting book is often adopted by organizations.

- Meet targets – Manipulation and misrepresentation of financial data in the books of accounts and showing high revenue and profits, create a picture of good financial performance. This helps the management meet targets expected by various stakeholders and make the company appear sustainable and strong.

- Rise in stock price – Good financial performance and strong balance sheet will boost the image of the business in stock market, among investors. This will lead to increased valuation and rise in stock prices, giving a sense of faith and confidence among shareholders.

- Minimise tax – The tax amount can be reduced by reporting underperformance and increase in cost, lower revenue and profits. Due to this the total income will go down, resulting in less tax implications. The company often saves funds in this manner, even though it does not depict a true picture.

- Meeting debt covenent – The companies may require to raise funds from lenders of investors who may ask want the business to meet some criteria, which are debt covenants. The business may manipulate the financial data using creative accounting practices to meet such restrictions and successfully be eligible for the loan amount.

- Attract stakeholders – Different stakeholders like creditors and investors analyse the financial statements before making investment decisions. A good and financially strong company, earning high profits, and incurring less cost and having good market valuation will be the ones stakeholders look for while investing, which can be achieved using creative accounting.

- Concealing negative condition – Overall, this method helps in covering up the negative condition of the company and project a picture of good financial health and profitability.

Implications

Here we study implications or impact of the above creative accounting practices on the company.

- Misrepresentation – The process actually misrepresents the financial condition and health of the company and misleads the stakeholders. This is harmful in the long run for both the parties.

- Stakeholders lose trust – The stakeholders lose trust on the organization once they find out that the books of accounts have been misrepresented through creative accounting practices. They may not plan to invest in the business any more.

- Legal issues- This method of inflating or deflating financial figures for the company’s benefit will result in legal problems because these method go against company rules and misguide people who have an interest in the company.

- Long term effect on stock price – It creates a negative effect on stock prices in the long run, when the matter is detected by regulators and policy makers of the economy. Since falsification of accounting can only help in presenting a heathy financial picture and high stock prices for short term, in the long term, it is bound to bring down the company valuation in the stock market.

- Fall in valuation – As suggested by the above point, the long term effect of the process on company valuation is very negative, and may result in bankruptcy or liquidation.

- Incorrect analysis – The financial data is widely used by investors and analysts for evaluation of company performance and taking investment decision so as to be sure of good returns. But if the data itself is not correct, the resuting analysis will also be affected by it.

- Inefficient resource allocation – The company may resort to such steps when it is not able to harness its resources to the optimum capacity and earn revenue and become financially strong. This proves its inefficiency in using the various resources available.

Thus, from the above points we see that this concepthas various implications on the business and it should be avoided as far as possible to maintain a good market reputation and remain sustainable.

Advantages

- The company can show a smooth and good growing graph of the company using creative accounting techniques. The management adopts this technique to show steady profits and good revenue to attract investors.

- Creative accounting helps the company set the required parameters, which is practically impossible.

- The company that makes losses can benefit from this creative accounting. Investors can be hopeful by seeing the future gains in the companies’ budgeted accounts, and often the company can cope with the situation.

- By adopting this method, the company can conceal the financial risk they may tend to suffer.

Disadvantages

- Although creative accounting is an ethical practice, sometimes it may be treated as illegal. When the values of the books of accounts are unethically or illogically misrepresented, it can call for some qualifications.

- The company will always be at a high risk of losing its investors because in case the investors get to understand the manipulations, it will not be good for the company. The investor’s interest might get hampered.

- The biggest disadvantage is that if an expert does the manipulation, it is fine, but if not, so the literate financial director or CEO decides to make a change, it will be a problem. Therefore, this may add to the cost of hiring a financial expert.

- In the long run, if it is disclosed that the company does a creative accounting practice, then the expectation from the company by their clients will also be at risk; thus, the company may lose its business.

Creative Accounting Vs Window Dressing

Let us analyse the differences between the two concepts as given below:

- The creative accounting techniques is a more aggressive step taking by the business for achieving its financial objective, whereas the latter is more of cosmetic changes undertaken by the company.

- The former leads to manipulation of accounting policies, and transactions, which leads to changes in figures and overall financial position, but the latter focuses more on temporarily changing the methods of accounting or timing of the same.

- The main intent of the former is to evade tax, show a strong financial health and increase stock prices and valuation but the latter may just aim to hold back creditors for some more time or increase cash flow temporarily.

- The effect of the former is irreversible and cause permanent damage to the business in the long run but the effect of the latter is not so negative fo the business and can be reversed.

Recommended Articles

This article has been a guide to Creative Accounting and its definition. We explain it with method, example, objectives, advantages, implications & disadvantages. You can learn more from the following articles –