Part of our Economic Concepts guide

What Is An Enterprise Fund?

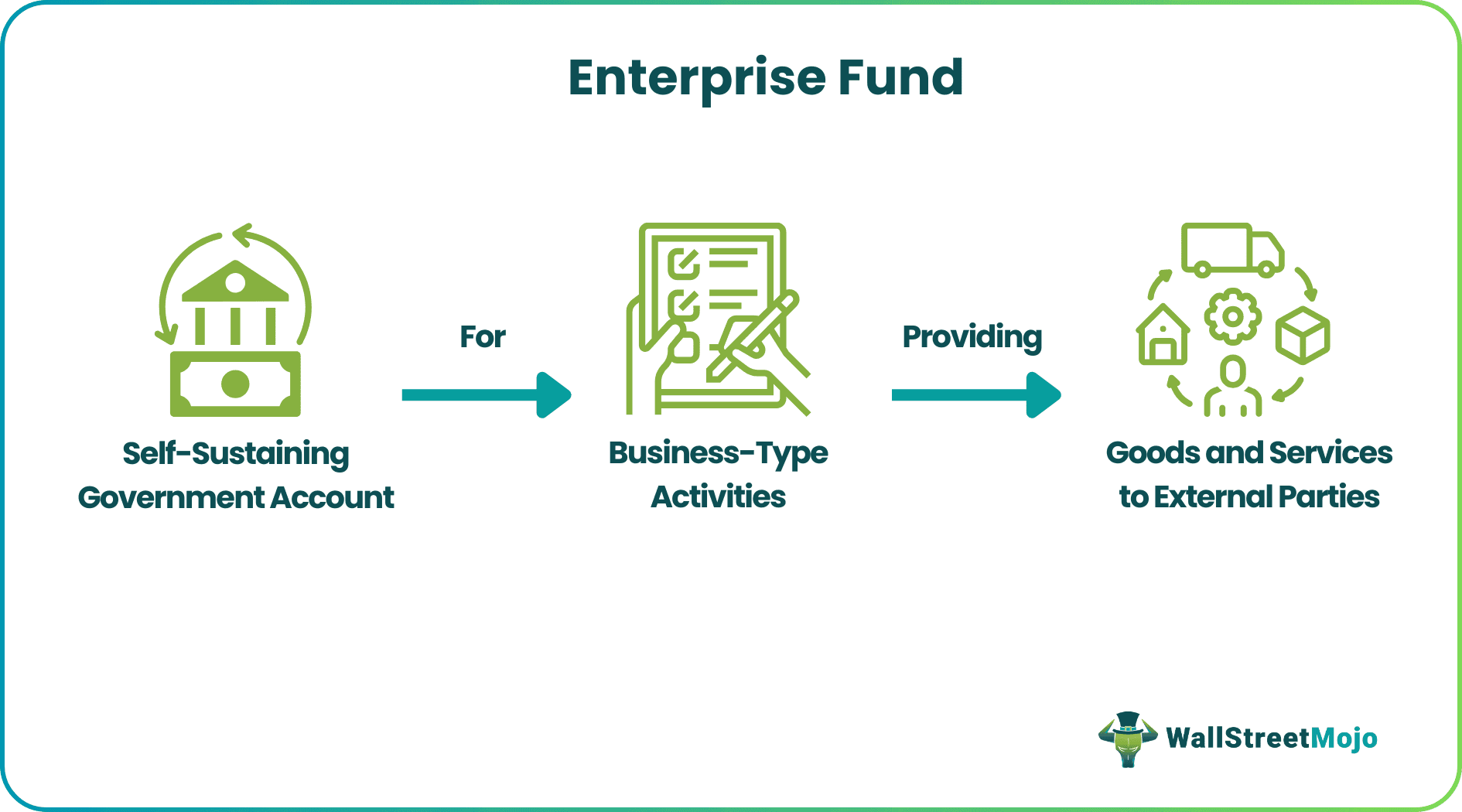

An Enterprise Fund pertains to the goods and services provided by government departments or units to the public for a fee. These funds are treated as business entities, with separate accounting for their revenues and expenditures from other departmental activities.

Examples of such funds include water, gas, electricity, sewer, security, etc. The community’s cost for these services is primarily recovered through user collection fees, and some of the expenditures may be subsidized by tax levies or other funds, reducing the burden on the public.

- An enterprise fund definition, within a government agency, states it as a process where citizens are provided goods and services for a user fee, effectively making the agency operate as a business.

- Accounting systems and procedures, as well as budgeting for this fund, are often separate because the revenues and expenditures for the services offered differ from other government activities. Agencies typically follow an accrual accounting basis.

- It may also be used to describe a financial fund, whether public or private, established to support a social cause or enterprise.

Enterprise Fund Explained

Enterprise funds represent typical government services for which the government autonomously collects usage charges from the public, such as citizens paying for electricity, water, gas, etc. These units stand apart from other government activities, classifying them as proprietary funds, as mandated by statute in 1986.

A defining feature of these funds is their accounting methodology, which involves the separate maintenance of financial statements, revenues, and expenditures. This system operates on an accrual basis, recording expenses and income in real-time, adhering to generally accepted accounting principles (GAAP) or international financial reporting standards (IFRS). Proprietary fund budgeting is essential, forming a significant income and expense stream supported by subsidies and other funds. These funds excel in discerning direct (e.g., capital outlay, personnel) and indirect costs (e.g., insurance, fringe benefits) related to services, establishing them as best practices in financial management.

Government agencies overseeing proprietary funds can monitor the proportion of fund expenditure recoverable. Due to separate accounting, any income earned is primarily allocated for this purpose. Budgeting yields crucial insights into expenses and income, enhancing overall cash management.

Asset depreciation in these funds mirrors business practices, and units disclose both long-term and short-term financial liabilities. Government agencies can adjust user fees based on additional expenditures, such as increasing gas prices in response to elevated crude costs.

It is essential to highlight that the term enterprise funds extend beyond its conventional association with government services. This broader scope encompasses not only public but also private financial funds established to champion various social causes. Illustratively, initiatives supporting women’s empowerment and environmental conservation exemplify the diverse and impactful applications of these funds. This adaptability underscores the extensive reach and versatility of business enterprise funds, contributing to positive change across a spectrum of financial and societal contexts.

Examples

Let us study the examples given below for more clarity on the concept.

Example #1

Suppose City Arctic is located near the North Pole. Due to the harsh climate year-round, it purchases gas from other countries and distributes it to residents. Residents are charged based on their consumption. The local government manages the income and expenses for this purpose separately. Annually, the federal government allocates a $10 million relief fund to City Arctic, providing another source of cash inflow for the city. In conclusion, the city of Arctic demonstrates a resilient financial model by efficiently managing its gas supply service and receiving consistent support from the federal relief fund.

Example #2

DBS Bank and Singaporean investment platform Heritas Capital have raised $20 million in the first close of their community enterprise fund, Asia Impact First Fund. The fund’s objective is to support social enterprises across the continent. Heritas Capital, which will manage the fund, has estimated an internal rate of return (IRR) of 5-10%.

This collaborative effort between DBS Bank and Heritas Capital reflects a commitment to driving positive change by channeling financial support into social enterprises. The fund’s targeted goal of $50 million, with a substantial contribution of $10 million from DBS Bank, underlines a shared vision for impactful initiatives. By supporting 10-15 Asian social and environmental enterprises, the Asia Impact First Fund seeks to make a meaningful difference in addressing critical social and environmental challenges across the continent.

Enterprise Fund vs Internal Service Fund

It’s essential to note that both enterprise and internal service funds are proprietary funds, each adhering to its distinct accounting systems.

Let us compare the differences between an enterprise fund and an internal service fund based on various aspects:

| Basis | Enterprise Fund | Internal Service Fund |

|---|---|---|

| Nature of Operations | It offers goods and services to citizens. | Transfers goods and services between government departments. |

| Customer Base | Serves the general public. | Different government agencies act as customers at various times. |

| Revenue Collection | Collects user fees; may use tax levy subsidies and other funds. | It operates on a cost reimbursement fee basis. |

| Profit Utilization | It retains any profits as a surplus for subsequent operations. | It aims to break even. |

Frequently Asked Questions (FAQs)

1. What is the difference between a special revenue fund and an enterprise fund?

A special revenue fund pertains to a designated revenue source, such as a disaster relief fund, with proceeds allocated exclusively to predetermined accounts. The critical distinction is that, unlike enterprise funds, users pay for services in the latter but not in the former.

2. What is the test for determining whether an enterprise fund is a major fund?

The Governmental Accounting Standards Board stipulates criteria for a fund to qualify as significant: the total assets plus deferred outflows, total liabilities plus deferred inflows, revenues, and expenses of the governmental fund must either be at least 10% of the total assets and liabilities of all enterprise or governmental funds in that category or at least 5% of all governmental funds combined. If these criteria are met, the enterprise fund attains major fund status.

3. What is the statement of cash flows for an enterprise fund?

The statement of cash flows is a significant financial statement detailing the community enterprise fund’s cash inflows and outflows from operations. Ultimately, this statement reconciles the opening and closing balances.

Recommended Articles

This article has been a guide to what is an Enterprise Fund. Here, we explain it along with its examples and comparison with internal service fund. You may also find some useful articles here –