What Is Internal Rate of Return (IRR)?

Internal rate of return (IRR) is the discount rate at which a project’s returns become equal to its initial investment. In other words, it attains a break-even point where the total cash inflows completely meet the total cash outflow.

The internal rate of return is commonly used to compare and select the best project. The project with an IRR above the minimum acceptable return (hurdle rate) is selected. The IRR is more helpful in comparative analysis than in isolation as one single value.

- Internal rate of return (IRR) is the percentage of returns that a project will generate within a period to cover its initial investment. It is attained when the Net Present Value (NPV) of the project amounts to zero.

- An IRR higher than the discount rate signifies a profitable investment opportunity.

- It facilitates the comparison of different investment options and projects. Based on the IRR, the most feasible and profitable options are chosen.

Internal Rate of Return (IRR) Explained

The internal rate of return (IRR) determines the worthiness of any project. In addition, the IRR determines the efficiency of a project in generating profits. Therefore, companies use the metric to plan before investing in any project. The hurdle rate or required rate of return is a minimum return expected by an organization on its investment. Any project with an internal rate of return exceeding the hurdle rate is considered profitable.

The internal Rate of Return is much more helpful when it is used to carry out a comparative analysis. When IRR is used in isolation as one single value, it is less effective. It is often used to rank multiple prospective investment options that a firm is planning to undertake. The higher a project’s IRR, the more desirable it is. That project becomes potentially the best available investment option. The actual internal rate of return obtained may vary from the theoretical value calculated. Nonetheless, the highest value will surely provide the best growth rate among all.

The IRR of any project is calculated by keeping the following three assumptions in mind:

- The investments made will be held until maturity.

- The intermediate cash flows will be reinvested.

- All the cash flows are periodic, or the time gaps between different cash flows are equal.

Internal Rate of Return (IRR) – Explanation In Video

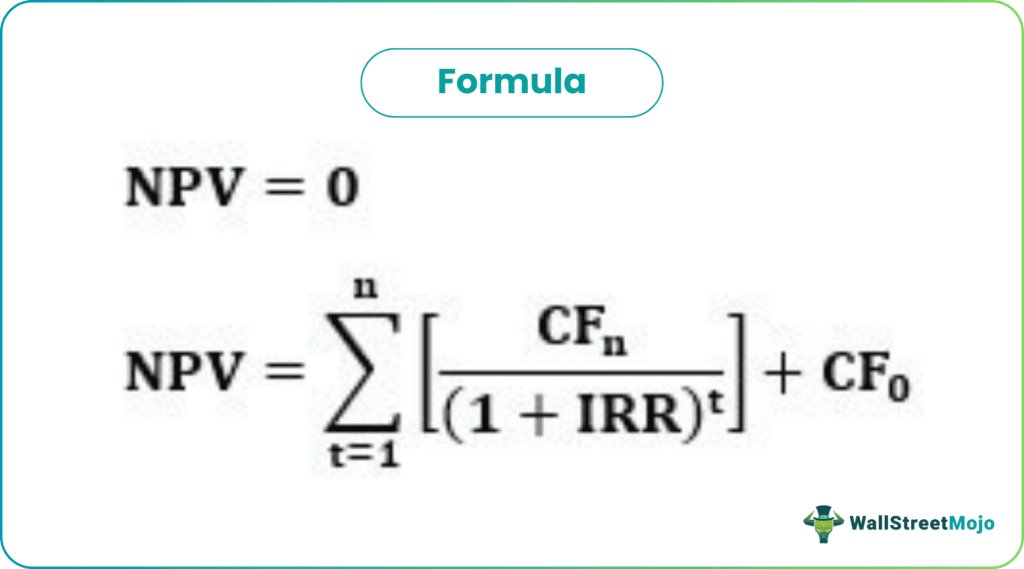

Formula

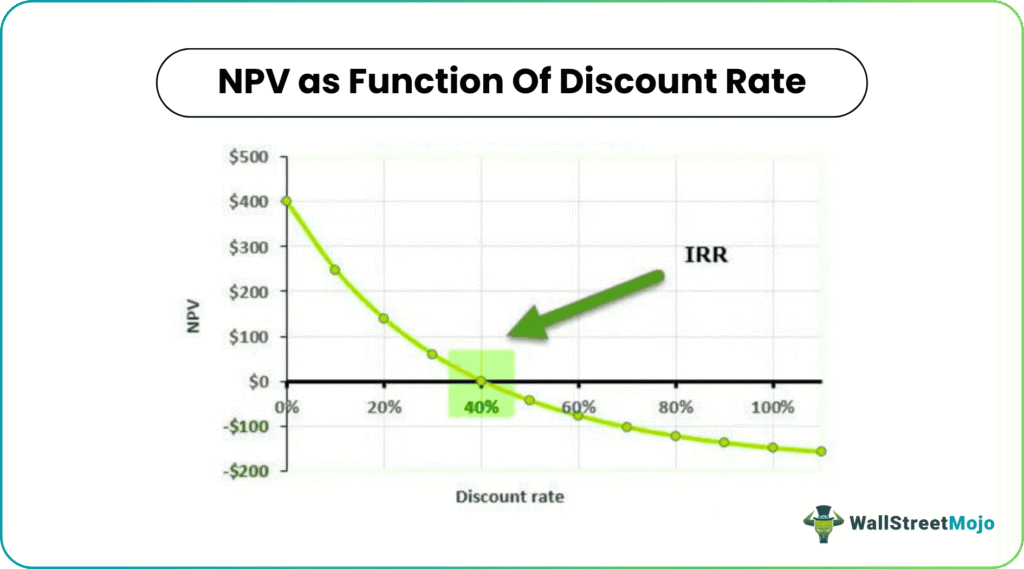

The internal rate of return gauges the break-even rate of any project. Therefore, at this point, the net present value (NPV) becomes zero.

Here,

The internal rate of return is the discount rate.

Calculation For IRR

Using excel is the easiest way to determine the internal rate of return. Alternatively, the trial-and-error method can be used. Here multiple discount rates are taken to get zero NPV.

Due to the character of the formula, however, IRR can’t be calculated analytically and should instead be calculated either via trial-and-error or by using software systems.

Discussed below is a step-by-step calculation guide for IRR:

- First, calculate the NPV by taking the given discount rate of the project and putting all the values in the given formula.

- See whether it is positive or negative. If it is positive, proceed further.

- For calculating the IRR, the NPV value is taken to be zero, and then by trial-and-error method, an assumed discount rate is filled in the formula, which provides the net present value closest to zero.

- Now, compare the Internal Rate of Return with the Discount Rate; if the former is higher than the latter, and the NPV is positive, the project is worth investing in.

Examples

Consider the following example to better understand the application of the internal rate of returns (IRR).

The DEF Group wants to diversify its business and plan to take up a new project that requires an initial investment of $400000. They will pay it off in 4 years. It will generate $40000 in the first year, $80000 in the second year, $1600000 in the third year, and $259600 in the fourth year. Find out the feasibility of this investment project if the discount rate is 8%.

Given:

- n = 4

- t = 0,1,2,3,4

- CF0= – $400000

- CF1= $40000

- CF2= $80000

- CF3= $160000

- CF4= $259600

- Discount Rate = 8%

Solution:

If the project’s internal rate of return is 8%, then the NPV is:

NPV = $23,451.06

Let us assume that the internal rate of return is 10% and that the NPV = 0.

NPV = 0

Thus, if the IRR is 10%, the project will be at a break-even point. This project generates a positive NPV, and the discount rate is lower than the IRR. In other words, the IRR is more than the project’s required rate of return; therefore, it is a profitable investment.

It is important to note that the value of CF0 is always negative as it is the cash outflow.

The above example clearly explains the process of determine internal rate of return in is a systematic manner using a suitable example which is very commonly faced by any company while making investment decisions.

Internal Rate Of Return In Excel

Given below is a systematic process of calculating the internal rate of returns (IRR) using excel:

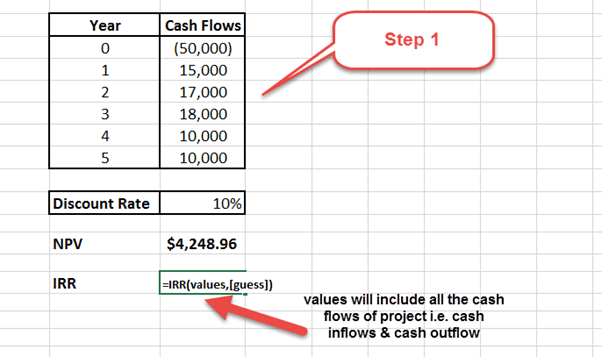

Step 1 – Cash inflows and outflows in a standard format

Below is the cash flow profile of the project. Now, we need to put the cash flow profile in the standardized format:

Step 2 – Apply the IRR formula in excel.

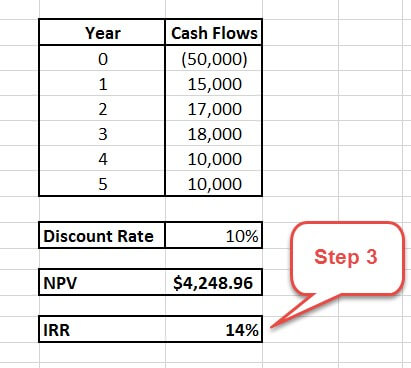

Step 3 – Compare IRR with the Discount Rate

- From the above calculation, you can see that the NPV generated by the plant is positive, and IRR is 14%, which is more than the required rate of return.

- If the discounting rate is at 14%, NPV will become zero.

- Hence, the XYZ company can invest in this plant.

Advantages And Disadvantages

Every financial concept has its own advantages and disadvantages. Let us identify the same for IRR, as given below.

The best part of the internal rate of return (IRR) is that it considers the time value of money. Money received in the present is of higher worth than money to be received in the future. This is because the money received now can be invested, and it can generate cash flows leading to future enterprises. Moreover, unlike capital budgeting, the hurdle rate is not compulsory for IRR because companies can compare the IRRs of different projects to find the most suitable investment option. Thus, it is an easy-to-implement tool. A project can be deemed worthwhile merely by determining if its internal rate of return is more than costs.

The internal rate of returns (IRR) does have its limitations. It cannot be applied to every project. In certain scenarios, this metric is ineffective; this includes projects with a fluctuating life span and projects involving an unpredictable cash flow. Also, this tool cannot be applied in isolation; net present value (NPV) is required for proceeding with this method. It even ignores future costs and reinvestment rate of the cash flows, thus failing to provide the actual profitability. Remember, a project can have multiple IRRs in its lifespan when the cash flows fluctuate; therefore, the analyst cannot rely on a single IRR value. This particular drawback is overcome by using the modern methods of determining IRR.

At times, the initial investment gives a small IRR value but a greater NPV value. It happens on projects that provide profits at a slower pace, but these projects may benefit in enhancing the organization’s overall value. Thus, making decisions based on IRR values alone can be destructive. Moreover, individuals might assume that once positive cash flows are generated throughout a project’s life, the money will be reinvested at the project’s rate of return. But, that is seldom the case. Instead, once positive cash flows are reinvested, it’ll be at a rate representing the value of the total capital employed. When IRR is misread or misused, it results in a false positive. A project will come off as more profitable than it actually is.

It is necessary to clearly identify and evaluate the pros and cons of any financial concept so that they can be effective and efficiently used or implemented in the business for maximum output through optimum utilization of resources.

IRR Vs ROI

Both the above are two financial concepts that are frequently used by investors and analysts. However, there are some differences between them as follows:

- IRR is the percentage return at which the company will reap the returns equivalent to its cash outflow. In addition, it gives an overview of the yearly growth rate. In contrast, return on investment (ROI) is the overall earnings of an investor for the invested sum.

- The IRR is a suitable analytical tool for the long-term analysis of any investment project. It assesses whether the investment is able to meet the return required from the investment. In comparison, ROI is a measure that can be applied to determine the profitability of any investment. Thus, it measures the efficiency level of an investment.

- The former takes in to account the time value of money that is calculated by discounting the future cash flows. But the latter does not consider the time of the cash flows.

- The ROI typically focus on the initial investment made in a project and the ent profit earned. But the IRR focus on the cash flows. Even if the cash flows are irregular, it is possible to determine internal rate of return that can be used to calculate the suitability of a projects with different cash flows over a period of time.

- The former is a measure that is relative in nature. But the latter is absolute in number depicting the investment profitability as a percentage.

However, both are extremely valuable and useful in the financial market. They provide essential perspectives on project performances and helps in focusing on the profit targets by taking into account the time value of money. But whether to select ROI or IRR, depends on the type and complexity of the investment and its objective.

IRR Vs NPV

Both the above are again widely used financial market tools that helps in investment analysis and capital budgeting. They measure the viability of investment and projects made by a business. However, let us find out their differences.

- The net present value is the final cash flow that a project will generate potentially, i.e., positive or negative returns. Whereas the internal rate of return is the discount rate at which the NPV becomes zero or reaches the break-even point. A point at investment equals total cash inflow. NPV values are required for calculating IRR.

- The former is the method used to calculate the rate of return in terms of percentage while the latter measures how much value the investment adds for the business.

- Compared to the former, the latter is considered a better and more reliable measure while comparing project that are mutually exclusive in nature.

- Unlike NPV, IRR can result in complex and multiple answers.

Thus, both are equally valuable and useful metric for investment comparison and valuation. In reality, both are widely used in the financial markets to make informed business decisions.

Frequently Asked Questions (FAQs)

What is the Internal Rate of Return?

The internal rate of return (IRR) refers to that percentage of future earnings from a project at which the company can recover the initial investment. It is the break-even point of returns.

Following is the formula for IRR:

What does IRR tell you?

The internal rate of return indicates a project or investment’s efficiency. It is one of the measures that facilitate the comparison of different investment options. The one with the highest return potential is selected. Thus, it is an essential tool in capital planning and investment decision-making. This method is also used for stock buyback decisions.

What does a good IRR signify?

If the internal rate of return is high, it means the investment opportunity is better than other options. However, the amount of initial investment, hurdle rate, and period of achieving the break-even point is equally significant.

Recommended Articles

This article is a guide to what is Internal Rate of Return (IRR). We explain it in a video along with formula & calculation, example & excel calculation. You may also have a look at the following articles on Corporate Finance –