Notional Value Meaning

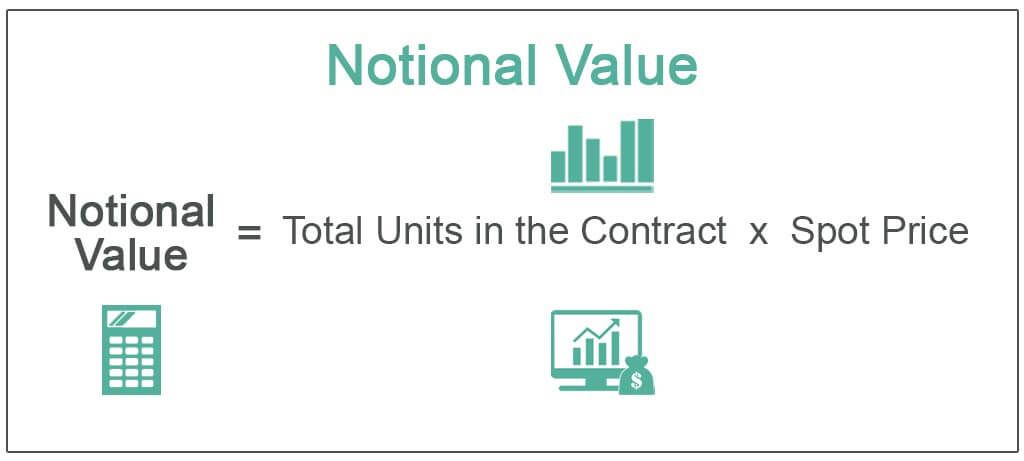

The notional value of any financial instrument means the total value of the derivative contract it holds and calculated by multiplying the total number of units that are there in the contract with the spot price of the said units prevailing in the market.

- Notional value refers to the nominal or face value assigned to a financial contract or instrument. It represents the underlying value on which calculations, such as payments or obligations, are based.

- Notional value is particularly significant in derivative contracts, such as options, futures, and swaps. It helps determine the size or scale of the contract and is used to calculate contractual payments, margins, or collateral requirements.

- Notional value provides a basis for evaluating the risk exposure associated with derivative positions. It allows investors and institutions to assess the potential impact of price fluctuations in the underlying asset on their financial situations.

- Notional value enables the comparison and aggregation of different derivative contracts. It allows market participants to analyze and manage their exposure to specific asset classes or markets.

Examples

Example #1

An options contract consists of 100 underlying shares. The call option is trading for $1.80. The underlying shares are selling for $25 each. The call option is opted by the investor for $1,800 ($1.80 * 100 shares).

Solution

Calculation of Notional Value

- = 100 * $25

- = $2,500

Thus, the nominal value of the derivatives contract comes to be $2,500.

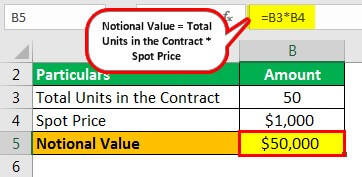

Example #2

An index future contract consists of 50 units of the index. One unit of the index is selling for $1,000.

Solution

Calculation of Notional Value

- = 50 * $1,000

- = $50,000

Thus, the nominal value of the future index contract comes to be $50,000

Relevance and Uses

#1 – Interest Rate Swaps

An interest rate swap is a contract in which the parties agree to exchange future interest payments with each other. The calculation of interest is done on a notional principal amount, which is determined well in advance. The interest amounts are calculated by multiplying applicable interest rates with the notional principal amount. Thus, this value serves as a base for interest calculations. The diagram below specifies how the interest rate swaps take place. It is a widely used process in the case of markets that are not regulated. Banks dealing with the process can estimate the extent of the credit risk that they need to bear. While pricing a swap, the trader has to find the value of the fixed and floating leg of the swap contract. The calculation of the fixed leg is easy and set at the starting point of the contract, but the floating leg calculation is complex because it depends on future rates of interest.

#2 – Currency Swaps

The currency swap is a kind of contract in which the parties agree to exchange the principal amount as well as the interest payments in the future represented in separate currencies. As in the case of interest rate swaps, it helps in the calculation of interest payments on the predetermined notional principal in currency swap contracts.

The diagram below shows the foreign currency swap process. In the example, the US company takes a loan from a US bank at 6%, and the Indian company does the same from an Indian bank at 7%. The principal of the US company is $10 million, and the Indian company is Rs. 450 million. Then, both exchange their principles. Then, following the interest payment schedule, they will exchange their interest. In the end, the companies will once again exchange their principal amount. A dealer facilitates the deal in return for a commission.

#3 – Equity Options

In an equity option, a holder of the option gets the right to buy or sell the underlying security at the strike price in the future, though he is not obligated to do so. The nominal value of the option represents the total value of the option that an investor holds. However, the curve of the equity option, as shown below, represents or indicates that an option of low strike will have more volatility as compared to options with higher strike prices. In conclusion, it can be said that traders estimate or believe that an up move is less probable than a down move.

Notional Value vs. Face Value

Notional value is the total value that a financial contract holds at the current spot price. It is calculated by considering the spot value of all the underlying assets of a financial contract.

On the other hand, the face value of a security is the value set by the issuer of the said security. It is mentioned on the certificate of the security such as the share certificate. All the interest payments are done based on face value and not based on notional value. Also, the face value of a particular security is fixed, but the notional value keeps on fluctuating based on market conditions.

Why is Notional Value Irrelevant?

It is just an imaginary figure and maybe irrelevant due to the below-mentioned reasons:

- It doesn’t take into account the risk that the parties to a financial contract bear.

- In the case of contracts relating to interest rate swaps, it is not the notional value that plays an important role. Instead, fluctuation in the LIBOR rate acts as a real game-changer.

Conclusion

As explained in the article, the notional value of a financial instrument represents the total value that the underlying securities hold based on the spot price. The same is used in various kinds of derivative contracts such as interest-rate swaps, currency swaps, stock options, and so on.

Frequently Asked Questions (FAQs)

Is notional value the same as market value?

No, notional value and market value are different concepts. The notional value represents a financial contract’s face value or size, while market value refers to the current price at which the contract could be bought or sold in the market.

How is notional value used in options?

In options trading, the notional value is the value of the underlying asset on which the option contract is based. It helps determine the size of the position and is used in calculating the premium, margins, and potential profits or losses.

Does the notional value represent the actual amount of money involved?

Notional value does not represent the amount of money exchanged or at risk in a contract. It is a reference value for calculating contractual obligations, such as payments or margins, based on the underlying asset’s value.

Recommended Articles

This has been a guide to Notional Value and its Meaning. Here we discuss formulas, examples, why the notional value is irrelevant along with its differences from face value. You can learn more about financing from the following articles –