Part of our Derivatives Basics guide

What is Covered Interest Rate Parity?

Covered interest rate parity says that investment in a foreign instrument that is completely hedged against exchange rate risk will have the same rate of return as an identical domestic instrument. Therefore, this implies that the forward exchange rate can be determined depending upon the interest rate earned on the domestic and the foreign investment and the Spot exchange rate between the two currencies.

Covered interest rate parity theorem is crucial in global finance to ensure currency and interest rate stability. It states that the forward exchange rate and interest rate differentials between two currencies should align to prevent risk-free arbitrage opportunities. This equilibrium is vital for efficient international trade, investment, and risk management, promoting economic stability across borders.

- Covered interest rate parity asserts that investing in a foreign asset, hedged against exchange rate fluctuations, yields equivalent returns to a comparable domestic asset. It facilitates calculating forward exchange rates through interest and the present spot rates.

- Various parity conditions link metrics like spot rates, forward exchange rates, expected future spot rates, inflation differentials, and interest rate differentials.

- Unrealistic assumptions in quoting forward rates can create arbitrage opportunities, while interest rate differences may not always offset as expected.

Covered Interest Rate Parity Explained

Covered Interest Rate Parity is a fundamental concept in international finance that establishes a relationship between exchange rates, interest rates, and forward contracts.

As per the international parity conditions, it is theorized that if the required preconditions are met, then it is not possible to make a risk-free profit from investing in a foreign market that gives a higher rate of return, one such condition for covered interest rate parity, the foreign security should be completely hedged.

There are various kinds of parity conditions that deal with the interlinking of measures such as the Current Spot rate, Forward exchange rate, Expected future spot exchange rate, Inflation differential, and Interest rate differentials.

Consider two countries: Country A and Country B, each with their own currency. The covered interest rate parity condition suggests that the interest rate differential between these two countries should be reflected in the forward exchange rate between their currencies. If the interest rate in Country A is higher than in Country B, according to this theorem, the forward exchange rate should incorporate this difference to prevent traders from exploiting the discrepancy and making risk-free profits.

To achieve this equilibrium, financial institutions engage in covered interest arbitrage. They borrow funds in a currency with a lower interest rate, convert them to a currency with a higher interest rate, and simultaneously enter into a forward contract to sell the borrowed currency and buy back the original currency at the agreed-upon forward rate. This process ensures that the potential profit from interest rate differentials is nullified.

Its significance lies in its role in maintaining stability in international financial markets. Any deviations from covered interest rate parity can signal market inefficiencies, leading to capital flows and affecting exchange rates.

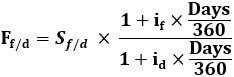

Formula

Let us understand the formula that shall act as a basis for our understanding of the covered interest rate parity theorem through the discussion below.

- Ff/d = Forward exchange rate, i.e., the exchange rate of a forward contract to buy one currency for another at a later point in time,

- Sf/d = Spot exchange rate, i.e., the exchange rate to buy one currency for another in the current period,

- id = Domestic interest rate and

- if = Foreign interest rate

- 360 days a year is used as a convention; we may use 365 days also

This actually implies that if the investor is aware of the domestic and foreign exchange rate and the current spot rate, he can determine the forward exchange rate, and if the actual forward exchange rate in the market is different from the one calculated by him, there is a chance of arbitrage profits and the CIRP will not hold.

Assumptions

Let us discuss the assumptions that are an integral part of covered interest rate parity conditions through the detailed explanation below.

#1 – Perfect Information

- All market participants are aware of and alert about market inefficiencies so that as soon as any such efficiency occurs, they act to drive it away.

- For example, suppose the return in one market is lower and higher in another market; in such a situation, the market participants will exchange the low return currency and invest the money received from this transaction in an instrument denominated in the higher return currency.

- At the time of maturity, the money invested in the higher return currency will be taken out along with interest and converted back to the lower return currency leading to an arbitrage profit. As more and more investors start making such profits, the higher interest rate currency will depreciate, and the lower interest rate currency will appreciate offsetting the increased returns from interest-rate disparity, and the parity will be in place again

#2 – No Transaction Cost

The parity condition assumes that there are no transaction costs related to investment in the foreign or domestic market, which could nullify the no-arbitrage situation

#3 – Identical Instruments

The domestic and foreign instruments should be identical in aspects such as default risk, maturity, and liquidity, etc. Capital should flow freely between markets to avoid liquidity constraints.

#4 – Stable Markets

The financial markets should be not facing any kind of regulatory pressures or stress and must be working freely and efficiently.

Examples

Now that we understand the basics, formula, and assumptions of the covered interest rate parity theorem, let us apply the theoretical knowledge to practical application through the examples below.

Example #1

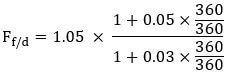

Let’s say we are dealing with the USD/EUR currency pair for a European investor. For whom the EUR is the domestic currency and USD is the foreign currency, and we are given the following information:

- 05, which implies that USD 1.05 is required for every EUR 1

- Domestic interest rate – 3%

- Foreign Interest Rate – 5%

- The investment period is one year or 360 days

- We need to calculate this

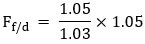

Using the covered interest parity formula, we can solve for the forward rate.

So if the forward rate is the same as that calculated above, there won’t be any profit in investing at the higher interest rate abroad. Now suppose if the forward rate in the market is misquoted and is 1.09, there is a possibility of arbitrage profit.

Under covered interest arbitrage, we hedge our position, and therefore we take the following steps:

- We are assuming that the forward rate should be 1.0704 while the actual forward rate is 1.09

- Borrow USD 1.05 at a higher interest rate

- Sell the borrowed USD at the spot rate of EUR 1

- Now the exposure is that we have to return the USD 1.05 and 5% interest on the same. Therefore, we hedge this exposure by entering into a forward contract in which we will exchange EUR for USD at the forward exchange rate of USD 1.09 per EUR

- We are left with EUR 1, and we invest the same at a 3% interest rate.

- At the end of 1 year, we have EUR 1.03 with us.

- We are supposed to pay back USD 1.05 x 1.05 = USD 1.1025

- Converting the EUR 1.03, we get 1.03 x 1.09 = USD 1.1227 by fulfilling the forward contract we had entered into at the beginning.

- Hence, we make a riskless profit of 1.1227 – 1.1025 = USD 0.0202

Example #2

In July 2022, The Euro broke parity with the US dollar for the first time in over 20 years. Moreover, the Japanese Yen declined sharply by 30% since the beginning of the year. Large movements like these in the currencies of established economies of the world pose a grave threat to the global economy.

This dramatic movement in these currencies is extremely rare. It signifies the participants of the market and citizens to move or retreat to a safe haven.

Covered Interest Rate Parity vs. Uncovered Interest Rate Parity

Both the covered interest rate parity conditions and uncovered interest rate parity signify a relationship with foreign currencies. However, there are differences in their fundamentals and implications. Let us understand them through the comparison below.

- Under the CIRP, the risk is completely hedged, even in the arbitrage example explained above, we have hedged our position by entering into the forward contract in step 4, in case of uncovered interest rate parity, as the name suggests, we don’t enter into the hedge.

- Uncovered interest rate parity deals with the expected spot rate during the tenure of the investment. Moreover, it implies that the exchange rate movement will offset the interest rate difference.

- In the covered interest rate parity, both domestic and foreign interest rate returns are known in domestic currency terms because the forward rate is hedged. While in case of the uncovered interest rate parity, the foreign interest rate return in domestic currency terms is unknown and un-hedged and is approximated to

- Uncovered interest rate parity assumes that the forward rates are unbiased predictors of expected spot rates. However, such is not the case for covered interest rate parity.

Frequently Asked Questions (FAQs)

1. What is the basic principle behind covered interest rate parity?

Covered interest rate parity is a theoretical concept that suggests that the difference in interest rates between two countries is equal to the forward premium or discount on their currencies. It implies that investors can achieve the same returns by investing in domestic assets and then hedging the exchange rate risk through a forward contract or investing in foreign assets without hedging and allowing the exchange rate to adjust.

2. How does exchange rate risk affect covered interest rate parity?

Exchange rate risk, or the potential for currency values to change, is a critical factor in covered interest rate parity. The concept assumes that investors can perfectly hedge their currency exposure through forward contracts. However, forward contracts might not provide complete protection due to factors such as liquidity constraints, counterparty risk, and unexpected market movements.

3. What are the limitations of covered interest rate parity as a theoretical model?

Covered interest rate parity rests on several assumptions which may not hold true in real-world scenarios. These limitations include transaction costs, restrictions on capital movements, market frictions, and the availability of risk-free assets. Additionally, the model assumes that interest rates and exchange rates are solely influenced by economic factors, disregarding other significant elements like government interventions, speculative behavior, and geopolitical events.

Recommended Articles

This has been a guide to What is Covered Interest Rate Parity. Here we explain its formula, examples, and compare it with uncovered interest rate parity. You can learn more about from the following articles –

- Currency Peg

- Dollarization Definition

- Meaning of Transaction Risk

- What is Interest Rate Derivatives?

- Extrinsic Value

Recommended Articles

Continue with these closely related articles from the same guide.