Part of our Financial Planning guide

What Is A Simple Savings Calculator?

A Simple Savings Calculator refers to the tool designed to calculate the maturity amount that shall be available to the individual wherein they have the options to invest, and choices for wherein they can maximize his return. Entering correct details while making the calculations is important to obtain accurate results.

Based on the figures obtained by this calculator, individuals and businesses assess the monetary benefits they are exposed to when they make an investment. With the help of the simple savings calculator, they learn about the investment growth over time and hence, they make their savings and investment decisions accordingly.

How Does A Simple Savings Calculator Work?

A simple savings calculator can be used to compare the different maturity amounts across the financial institution as a higher rate of interest doesn’t guarantee the highest absolute amount, as seen in the example above. Hence, one should calculate and compare the amounts across maturity and then take a decision. As the amount to be received over a period can easily be calculated using this tool, individuals and entities can decide where to invest and how much for better returns.

When a person earns, the motive is to meet the expenses smoothly, thereby also savings something for future. This simple calculator for savings allows users to find out which savings scheme would help them reap maximum returns. Based on this calculation, therefore, they decide to make fruitful investments with less risk involved.

As the name implies, it is a simple tool, which does not take into consideration factors, like inflation, taxes, or other determinants before calculating the returns. They simply want users to enter the initial amount of money they would deposit every month and then accordingly check the extent to which it would grow and offer return at maturity.

Elements

These calculators work on different elements, the values of which when entered, compute the returns on the savings one makes. Let us have a look at those components of the calculator:

- Initial amount: This is the amount that one starts with saving or investing. It is one of the most important factors that determine the pace at which the investment would grow.

- Monthly deposit: This marks the deposit that one can feasibly invest monthly in the scheme. Individuals decide this amount on the basis of their monthly budget.

- Number of years: This is the period until which the monthly deposits are to be made for the investment to mature. It is the time until which the investment grows and reaches its maximum level.

- Annual interest: This is the rate of interest that applies to the investment. There is a rate table provided by different authentic sources, referring to which helps individuals learn about the rate at which the investment would grow. Here, it is important to mention whether it is applicable monthly, quarterly, bi-annually or annually.

Formula

The formula based on which the simple savings calculator works is mentioned below:

Mathematically it can be calculated for one-time Simple Savings:

Secondly, if monthly simple savings is made, the calculation:

Wherein,

- M is the total amount at the end of the simple savings period

- I is the initial amount invested

- i is the fixed amount invested at regular intervals

- r is the rate of interest

- F is the frequency of interest is paid

- n is the number of periods for which simple savings shall be made.

There are a lot of banks and other financial institutions that are competing in the market to attract deposits so that they can do more business, i.e., lending of the money to corporates or high net worth individuals. Some banks would pay a higher rate of interest if the deposits exceed certain threshold limits and are maintained in the account, or else, they will pay a standard rate of interest. Further, there could be a difference in frequencies of the interest payout; for example, the interest could be compounded and paid out quarterly, semi-annually, or annually depending upon the bank. Therefore, with this calculator, individuals would be able to determine which financial institution they should choose to invest their money in by comparing the maturity amount or return earned on their principal amounts.

How to Calculate?

One needs to follow the below steps in order to calculate the simple savings.

Step #1 – Determine what amount would be invested, whether it’s in lump sum or there is a periodical investment as well, then the same should be considered in comparing savings rates calculations.

Step #2 – Figure out the rate of interest that is available in options for the individual, and that would be earned or is expected to be earned on the simple savings.

Step #3 – Now, determine the period for which it shall be invested, and mostly those will be for the long term and will depend upon case to case.

Step #4 – Divide the rate of interest by the number of periods the interest or the Simple Savings interest is paid. For example, if the rate paid is 5% and it pays monthly, then the rate of interest would be 5%/12, which is 0.416%.

Step #5 – Now use the formula that was discussed above in point 1) in case the Simple Savings is made lump sum and use formula 2) in case the Simple Savings amount is made at regular intervals along with any initial amount for all the options available.

Step #6 – The resultant figure will be the maturity amount that would include the Simple Savings income as well, and choose the one which has the highest payout in terms of interest.

Example

Let us consider the following instance to see how the calculator can be used:

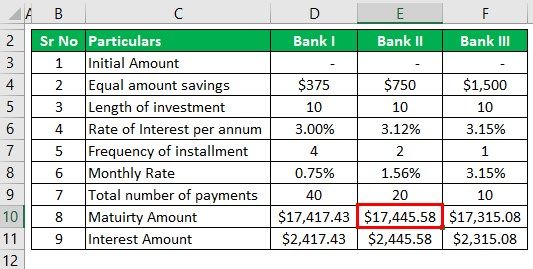

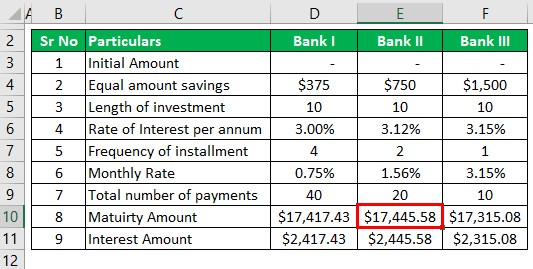

Mr. William is now an adult and is excited to open up his first savings account. He has searched for the financial institution, which provides a high rate of interest, but he is perplexed as he doesn’t know which bank will be providing him the highest return. Below are the quotes that Mr. William has shortlisted.

| Particulars | Bank I | Bank II | Bank III |

|---|---|---|---|

| Length of Investment | 10 | 10 | 10 |

| Rate of Interest per annum | 3.00% | 3.12% | 3.15% |

| Frequency of Interest Payout | 4 | 2 | 1 |

He wants to invest $1,500 in either one of the accounts, and he will invest the way the account is paying interest. For example, if the bank pays semi-annually, then the amount will be invested equally at the end of each period and will continue to do so for a period of 10 years.

Based on the given information, you are required to calculate the amount that he would be saving, and the interest earned on the same, and which Bank should he choose to invest in.

Solution:

We are given the below details:

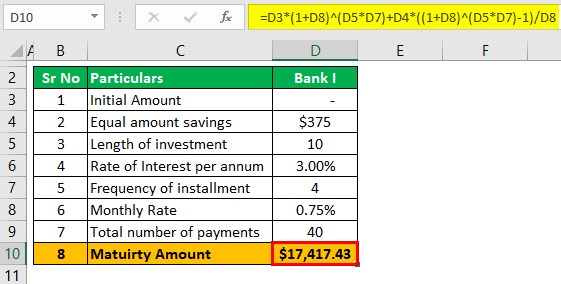

BANK I

- I = Initial amount will be zero

- r = Rate of interest which is 3.00% and Quarterly it will be 3.00%/4 which is 0.75%

- N = Frequency which is quarterly here; hence it will be 4

- n = number of years the Simple Savings to be made, which is 10 years here.

- i = It is the regular amount to be invested, which is 1500/4, that is $375

Now, we can use the below formula to calculate the maturity amount.

- =0 * ( 1 + 0.75% )10 * 4 + 375 * ( ( 1 + 0.75%)10*4 – 1 / 0.75%)

- =17,417.43

Maturity amount will be 17,417.43

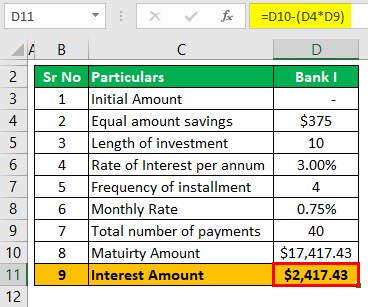

Compounded interest earned would be $17,417.43 – $( 375 * 40 ) = $2,417.43.

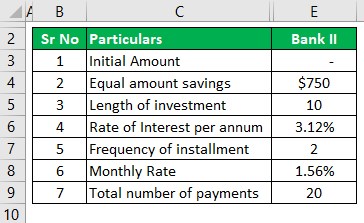

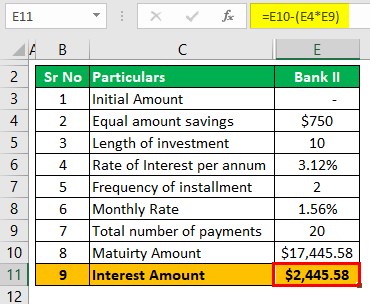

BANK II

- I = Initial amount will be zero

- r = Rate of interest, which is 3.12%, and Semi-annually it will be 3.12%/2, which is 1.56%.

- N = Frequency which is Semi-annually here, hence it will be 2

- n = number of years the Simple Savings to be made, which is 10 years here.

- i = It is the regular amount to be invested, which is 1500/2, that is $750

Now, we can use the below formula to calculate the maturity amount.

- = 0 * ( 1 + 1.56% )10*2 + 750 * (( 1 + 1.56%)10*2 – 1) / 1.56%

- = $17,445.58

Maturity value will be $17,445.58

Compounded interest earned would be $17,445.58 – ($ 750 * 20 ) = $2,445.58.

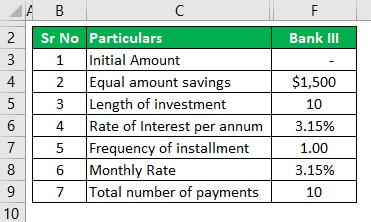

BANK III

- I = Initial amount will be zero

- r = Rate of interest, which is 3.15%, and Annually it will be 3.15% / 1, which is 3.15%

- N = Frequency which is Annually here, hence it will be 1

- n = number of years the Simple Savings to be made, which is 10 years here.

- i = It the regular amount to be invested, which is 1500 / 1 that s $1,500

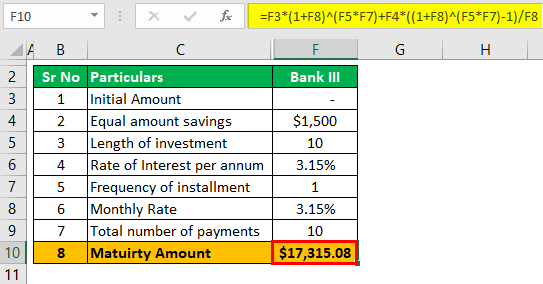

Now, we can use the below formula to calculate the maturity amount.

- = 0 * ( 1 + 3.15% )10*1 + 1500 * (( 1 + 3.15%)10*1 – 1) / 3.15%

- = $17,315.08

Maturity amount will be $17,315.08

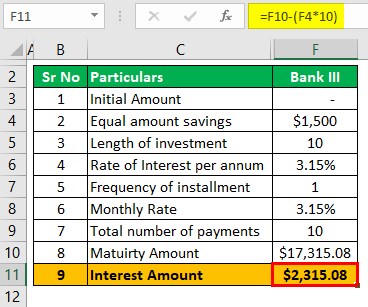

Compounded interest earned would be $17,315.08 – ($1500 *10 ) = $2,315.08.

The highest amount earned is in Bank II, and hence he should open an account with Bank II.

Advantages and Disadvantages

There is a set of benefits and limitations of using the simple savings calculators. Some of them have been mentioned below. Let us have a quick look at them:

Benefits

- It makes calculating the savings estimates for future.

- It helps compare investments to help individuals assess returns of different investment and make a wiser choice for maximum returns.

- There is no limitation to the period until which one can save. An individual can save for only a couple of years to fulfil their family vacation requirements or they may continue investing for 30 long years to serve long-term financial needs.

Limitations

- The calculator offers an estimate of the amount one might receive on maturity.

- One wrong input for the elements would lead to huge discrepancy in results.

Recommended Articles

This has been a guide to what is Simple Savings Calculator. Here, we explain its formula, how to calculate it, examples, advantages and disadvantages. You may also take a look at the following useful articles –