Part of our Accounting Concepts guide

Tax Loss Carry Forward Definition

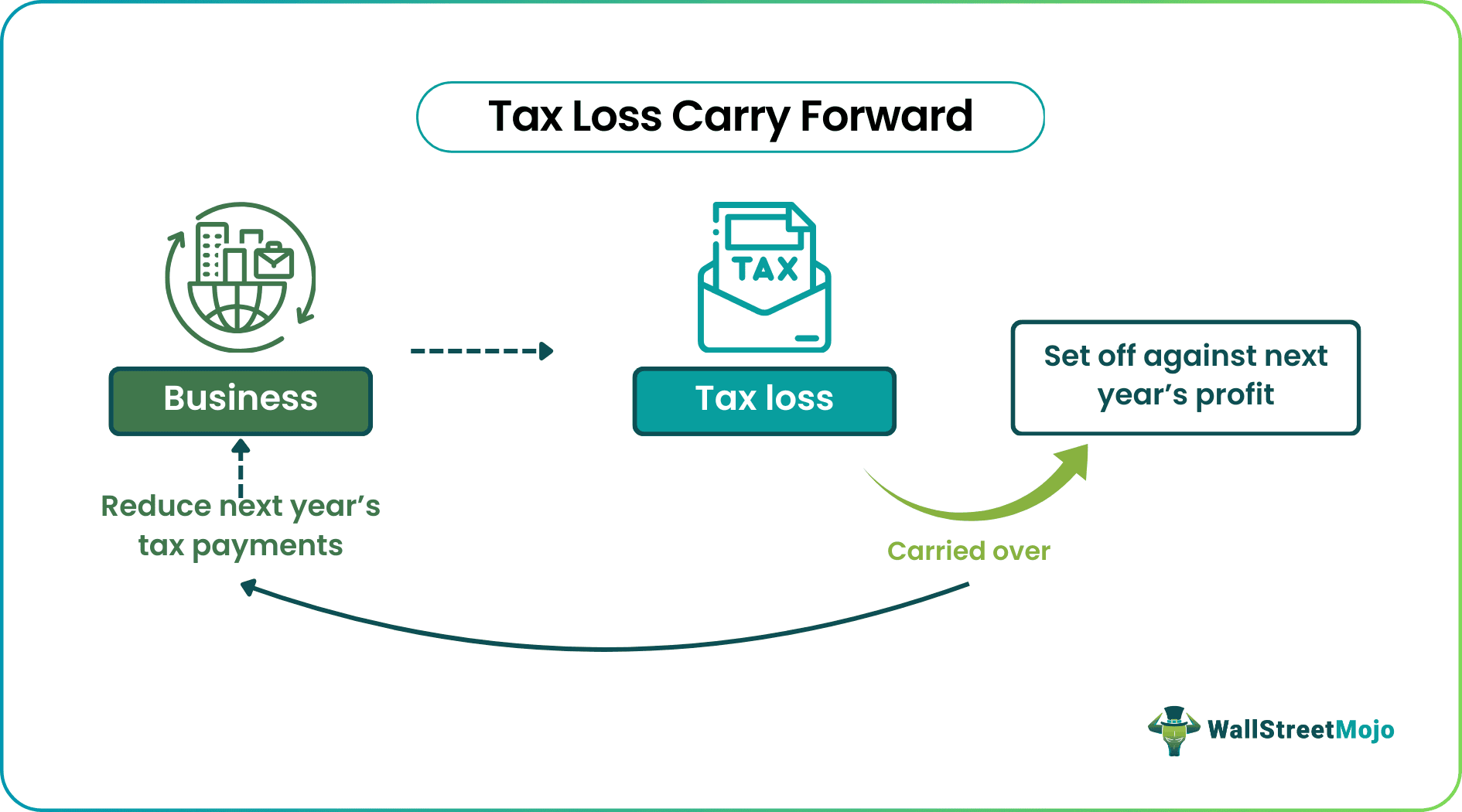

Tax Loss Carry Forward is a provision that permits an individual to take forward or carry over the tax loss to the next year to set off the future profit. Any taxpayer, be it an individual or a company, can claim it to lower the tax payments in the future.

A business or an individual shall claim the tax loss carried forward to reduce any tax payments in the future. Every country has its own set of rules and regulations that govern the set-off and carry forward the net operating losses for the taxpayers, whether individual or business.

How Does Tax Loss Carry Forward Work?

The tax loss carry forward is a rule that allows a business or an individual to take the tax loss carry forward limit to the next year and set it off against the future profit.

The following points must be noted before carrying forward the tax loss.One should complete the tax return that applies to the type of business.

Determine whether the tax deductions exceed the taxable income and if there is a net operating loss that should not be complicated to compute for the taxpayer.

Also, certain laws require that tax returns be filed within the due date to claim and carry forward losses for the future, do make a note of the same.

There could be various heads of income, and there are laws that treat them differently, and so as their tax losses carry forward, the taxpayer should make a note of the same.

These rules and regulations for individual and corporate tax loss carry forward are not simple, and they would require careful consideration of every provision, maybe the help of local tax attorneys. E.g. in the United States of America (USA), every state has its own set of rules and regulations governing the tax code. Thirty states and DC conform to the federal tax code of allowing twenty years of Net Operating Loss to be carried forward. At the same time, Illinois allows twelve years of carry forward, whereas Kansas and Vermont allow ten years of loss carry forward.

Last but not least, the taxpayer should keep excellent tax records of the claims he makes in the tax returns.

Types

Let us look at the types of individual and corporate tax loss carry forward.

#1 – Business

They can utilize these loss carry forward provisions against NOL, which stands for net operating loss, capital losses that are more than the capital gains, and certain gains earned from the exchange or sale of stock of the qualified small business.

#2 – Individual Taxpayers

They may use these such provisions for various circumstances, and that information can be extracted from the IRS and their respective taxing authority of the state. For example, if a taxpayer makes excess contributions to a 529 plan of the state, the taxpayer can’t deduct the amount he has deposited in excess. Still, the taxpayer shall be able to carry that tax loss carry forward limit to future years.

Examples

Let us look at some corporate and individual tax loss carry forward examples.

Questa power company, a profit-making company in the town, has been recently affected by the prices of coal due to its huge demand and less supply. Below is the snapshot of the recent monthly income statement and tax payment.

Using the information below, we will calculate the amount of tax loss that the company can carry forward and what is remaining in the balance that must be utilized.

Solution:

Until February, the company was making profits and paying tax at the rate of 30%, but after March, the company didn’t pay any tax till June as they were incurring losses below.

We can see that from March onwards, the loss was initiated, and the same is getting carried forward until the company starts making a profit, which happens only in June.

Till May month, the company accumulated a loss of $21,000. However, the same was offset partially by the gain of $5,000. So now, the remaining loss to be absorbed in the future is $16,000.

Example #2

One of the famous examples could be President Donald Trump of the US and who is also a businessman. In the year of 2016, while electing the president of the US, the New York Times, a renowned publisher, released the tax return of Donald Trump for the year 1995, in which a loss of $916 mn was reported that happened in the year 1995, which was carryforward to offset in the future years against the next income.

The realized capital losses arrived from the investments that Trump made in airline business ventures, casinos, and the Manhattan property. The same publisher reported that this loss of $916 million would allow Mr. Trump to escape federal tax of approximately $50mn up to eighteen taxable years.

Thus the above examples clearly explain the corporate and individual tax loss carry forward situations.

Pros

The tax loss carry forward rules have some advantages as follows.

- Tax loss carryforwards are beneficial as they create future tax relief for the business or the companies; hence, they are very valuable for them.

- These losses can be generally carried for seven years per the laws, which again provides relief to companies. When they make a profit, they won’t be required to pay tax immediately, which ultimately removes pressure from them for cash outflow, and working capital will be managed properly.

- In some cases, the companies acquire another company solely for tax-loss carryforward purposes.

Cons

There is no major disadvantage of tax loss carry forward rules. The only thing is it can make the business or the company look like a loss-making company.

Recommended Articles

This article has been a guide to what is Tax Loss Carry Forward. We explain it with example, how it works, its various types, pros and cons. Here we also discuss its advantages and disadvantages along with some examples. You can learn more about financing from the following articles –