Part of our Accounting Concepts guide

What Are Sales Taxes Payable?

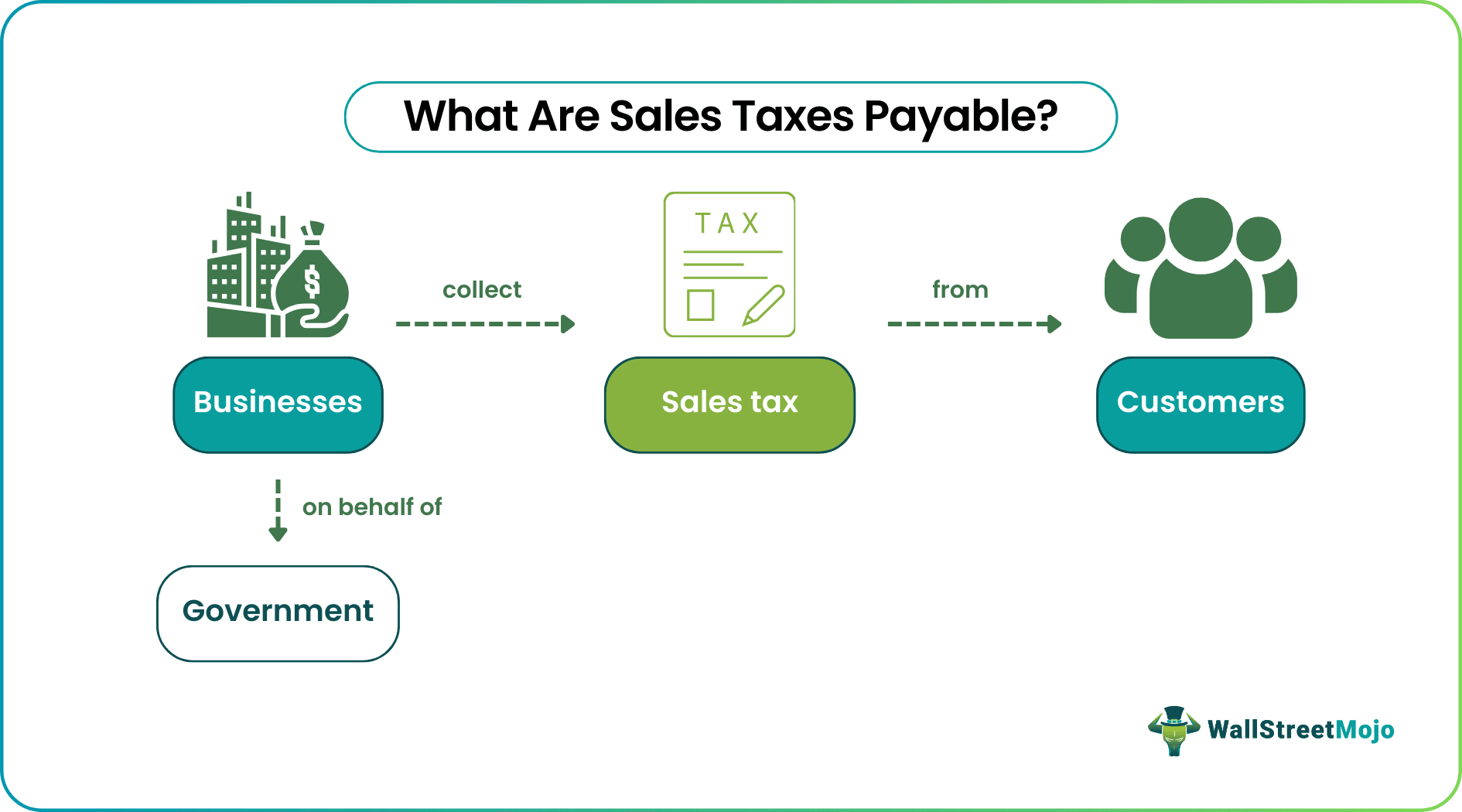

Sales taxes payable refers to the liability account created when an entity collects sales taxes on behalf of the government and stores the aggregate amount of taxes before paying to the concerned taxes authority. In other words, the entity acts as the custodian of the sales taxes collected from customers and is obligated to remit the same to the government at regular intervals of time.

The sales taxes payable accounts are divided into different sections, given the demand for such taxes to be paid by customers to different authorities. There is a local account to store tax information related to customers paying taxes to local authorities and similarly, there are state account and country account for the tax amount to be received by the respective bodies.

Sales Tax Payable Explained

Sales taxes payable is a short-term liability account as the amount gets remitted over a period. Sales taxes refer to the taxes collected by government tax authorities on selling certain goods and services. Typically, firms, companies, and individuals collect sales taxes from customers when they sell goods or services. Later, they must remit the aggregate amount periodically to the appropriate tax authority. In short, the companies that collect taxes from individual customers become the custodian of the sales tax until they are paid further to the concerned authorities.

The time lag between the collection of sales taxes and remittance of the same results in creating a sales tax payable account, which is then recognized as a liability in the books of the concerned firms, companies, and individuals.

As the companies selling the goods and services to customers store the taxes from customers on behalf of the authorities, they are prone to regular scrutiny. Hence, the government appoints auditors to the businesses to check their calculation of sales taxes and see if it complies with all the rules. If found inappropriate, the authorities can charge a fine or penalty for the same. Given this complexity and the risk of penalties, many businesses turn to specialized software solutions to automate their sales tax compliance processes, often evaluating software like Avalara to find the best fit for their operational needs.

How To Record?

Sales Tax Payable is recognized as a liability that has to be usually paid within one year from the collection. So, it is categorized under current or short-term liabilities. Therefore, the outstanding amount is reported under the current liabilities section of the balance sheet. Sometimes, it is combined with the payable trade account.

It is fairly simple. To record credit sales in a sales journal, create a separate column for capturing it for each credit sale. Ensure that the aggregate of this column is recorded in the sales taxes payable account maintained in the general ledger at a regular interval of time.

Likewise, create a separate column for sales returns to record a reduction in sales taxes payable liability due to sales returns. Ensure that the aggregate of this column is debited to the sales taxes payable account in the general ledger at a regular interval of time.

Revenue vs Sales Explained in Video

Journal Entries

→ Explore all 30 Journal Entries articles

The journal entries for sales taxes payable are classified into two broad categories, which are as follows:

- At the time of collection of sales taxes from customers

- At the time of payment of sales taxes to the appropriate taxes authority

At the time of collection of sales taxes from customers – When a firm collects sales taxes after sales of certain goods or services, the following journal entry is made –

As a result of the above transaction, the cash balance (or trade receivable account for credit sale) rises, and sales and sales taxes payable also increase.

At the time of payment of sales taxes to the appropriate taxes authority – When a firm remits the aggregate amount of the sales taxes to the concerned taxes authority, the journal entry is made in the following way –

As a result of the above transaction, the outstanding amount of sales taxes payable on the liability side reduces by the same amount as the cash balance on the asset side.

Examples

Let us consider the following instances to see how to compute sales tax payable:

Example #1

Let us take the example of ASD Inc. to illustrate the concept of a collection of sales taxes payable. The company executes only two sales during the second week of February 2020, which are as follows:

- 03, 2020: Cash sale of $10,000, which is subject to sales taxes of 4.5%.

- 05, 2020: Credit sale of $8,000, which is subject to sales taxes of 6.0%.

ASD Inc. operates in a state where it must remit the collected sales taxes to the appropriate taxes authority at the end of every week. However, as mentioned above, the company didn’t remit the sales at the end of the week. Prepare the journal entries for the two sales executed by the company in the first week of February 2020.

The journal entries for recording the sales executed during the first week of February 2020 are as follows –

Example #2

Let us take the same example of ASD Inc. to illustrate the concept of remittance of such tax payable. The company remits the sales taxes collected in the first week of February 2020 to the appropriate taxes authority on March 05, 2020. Prepare the journal entry for the remittance of the sales taxes payable in March 2020.

The journal entry for recording the remittance in March 2020 is as follows –

Recommended Articles

This has been a guide to what are Sales Taxes Payable. Here, we explain the concept along with how to record it, its examples, and journal entries. You may learn more about accounting from the following articles –