Part of our Careers in Accounting guide

What Is Accounting Test?

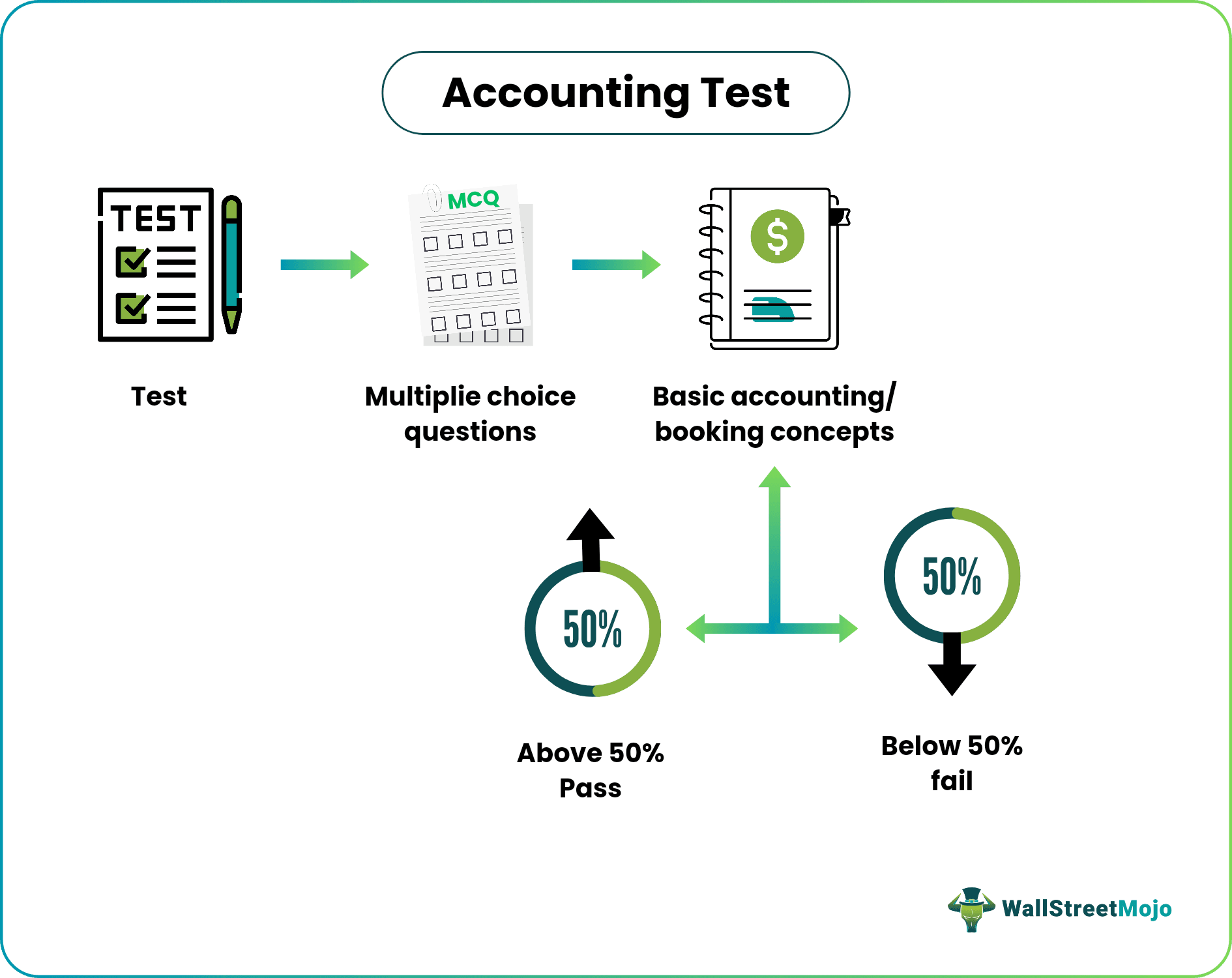

The accounting test analyzes the candidate’s ability to maintain the proper book of accounts, i.e., bookkeeping, and includes some very basic accounting questions in the form of Multiple Choice Questions (MCQ). The candidates are expected to answer by picking the correct option from the given four options in the questions.

The qualification marks are 50% of the total correct answers given. Suppose any candidate manages to clear 50% or more shall be considered fit for the next level. Accounting depends on practice, and then only this subject can be understood easily by any candidate. Therefore, an accounting Test is made to check the basic knowledge of the subject the candidates want to pursue their careers.

Accounting Test Explained

A practice accounting test is a method of assessing the knowledge level of a candidate regarding accounting and bookkeeping skills. Such tests usually have a set of multiple-choice questions related to accounting to test the knowledge regarding essential accounting principles and some basic concepts.

Such job interview accounting test not only give candidates an opportunity to understand their knowledge level and choose their field of study according to it but it also helps company recruiters understand the knowledge level of applicants using the job interview accounting test for an accounting job and select them for a specific profile. Therefore such tests are very useful.

Accounting Test Questions With Answers

Let us look at some sample questions and answers of practice accounting test to understand the concept.

Question #1 – Depreciation of any machinery is implied from the date.

- The machinery is ready to be put to use.

- When the machinery was purchased.

- The machinery was installed.

- Any of the options mentioned above.

Answer: The machinery is ready to be put to use.

Question #2 – Among these four, which one is not a subsidiary book.

- Purchase books.

- Cash Book.

- Bill of Receivables Book.

- Sales Book.

Answer: Cash Book.

Question #3 – Financial Statement is a part of which of the following.

- Bookkeeping

- Cash Flow

- Accounting

- All of the above

Answer: Accounting.

Question #4 – The Value of any asset after deducting depreciation from the historical Cost is defined as.

- Market Value

- Net Realizable Value

- Book Value

- Face Value

Answer: Book Value.

Question #5 – Apex Co. Ltd has machinery worth $10000 Written down Value and $1500 as its Cost on 31.03.19. The machinery was sold to a client, and the amount of $100 was transferred to the Capital Reserve account. Calculate the sale price of the machinery.

- $11000

- $5000

- $16000

- $26000

Answer: $16000.

Question #6 – Pick up a correct Journal entry for the loan taken from the bank.

- Bank Account Debit and Cash Account credit.

- Cash Account Debit and Loan Account credit.

- Bank account Debit and Loan account credit.

- Loan Account Debit and Bank account credit.

Answer: Bank account Debit and Loan account credit.

Question #7 – What type of error is this if credit sales are wrongly passed through the purchase book?

- Error of Omission

- Error of Commission

- Error of Principle

- None of the above.

Answer: Error of Commission.

Question #8 – Pick up a correct journal entry for machinery purchased.

- Bank account Debit and Asset account credit.

- Cash account Debit and Machinery account credit.

- Machinery account Debit and Sales account credit.

- Machinery account Debit and Bank account credit.

Answer: Machinery account Debit and Bank account credit.

Question #9 –

Steven places an order to Peter for the supply of a certain product that was not yet manufactured. Upon receiving the order, Peter went to the market and purchased all the raw materials required, hired some employees to get the things done, completed the order, and delivered the goods to Steven. Now here, the question arises that the sale is presumed to be recorded at which event.

- Delivery of good

- Purchase of raw material

- Receipt of good

- Production of goods

Answer: Delivery of good.

Question #10 – Sales of $1500 to Mr. Xavier were posted to his account at $1400. To rectify the mistake of $100, the same should be done by doing what to Xavier’s account.

- Debited

- Credited

- Ignored

- Either Debit or Credit.

Answer: Debited.

Question #11 – For machinery, if the depreciation rate is the same, the depreciation amount under the Straight Line Method Vis-a vis Written Down Value method will be.

- Equal in all the years

- Equal in the first year but lower in the subsequent years.

- Equal in the first year but higher in the subsequent years.

- Lower in the first year but equal in the subsequent year.

Answer: Equal in the first year but higher in the subsequent years.

Question #12 – Account Receivable is.

- Nominal account

- Real account

- Personal account

- None of the above.

Answer: Real account.

Question #13 – The Cost of machinery is $135000, and its residual value is $5000; the useful life of the machinery is said to be ten years. The company used the Straight Line Method depreciation method for the first five years. Later on, after discussing with the management, the company decided to take its useful life further for another eight years. Therefore, calculate the depreciation amount for the 6th year.

- 8000

- 8125

- 8200

- None of the above.

Answer: 8125

Question #14 – Purchase of machinery for cash.

- Increases the total cash.

- Decreases the total asset.

- Remains total asset unchanged

- Decreases total liability.

Answer: Remains total assets unchanged.

Question #15 – Sale of a building credited to the Sales account. Please pick the correct error for the same.

- Error of Omission

- Error of Commission

- Error of Principle

- None of the above.

Answer: Error of Principle.

Recommended Articles

This has been a guide to what is Accounting Test. We explain it with some sample questions and answers related to basics of accounting. You can learn more about it from the following articles –

- Accounting Terminology

- Bookkeeper Interview Questions

- Financial Planning and Analysis Interview Questions

- Accounting Interview Questions

Recommended Articles

Continue with these closely related articles from the same guide.