Part of our General Ledger guide

What is Debit Balance?

A debit balance is an amount that states that the total amount of debit entries in a general ledger is more than the total amount of the credit entries.

It is different from debit entry. A debit entry is made to record a transaction in the general ledger, e.g., when we purchase an asset, we debit the asset account recording the purchase and credit bank account showing an outflow of money. At the same time, a debit balance is a net amount (Debit minus Credit) in a general ledger after recording all the transactions.

Examples

It is generally found in the assets and expenses ledgers; a few examples are stated below,

- Fixed assets A/c’s – When a fixed asset is purchased, it will be recorded as a debit transaction, and later credit entries are made for charging depreciation to the asset. It will leave a net debit balance in the fixed asset account.

- Expense A/c’s – The expense and loss accounts like rent, salary, repair, and maintenance, interest expense, electricity, etc., will always carry a debit balance.

- Investments – Similar to fixed assets, investment purchased will have a debit entry, and later debit balance will be reflected in the investment account.

Debit vs. Credit Balance

In accounting general ledger we can find two types of balances. To find out what balance a ledger reflects, we need to calculate which side of the ledger has a higher balance, i.e., if the debit total is greater than the credit, the ledger has a Debit balance. Similarly, if the credit total is higher than the debit total, it will have a credit balance.

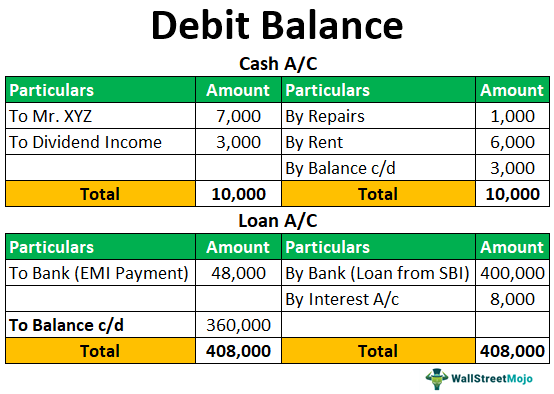

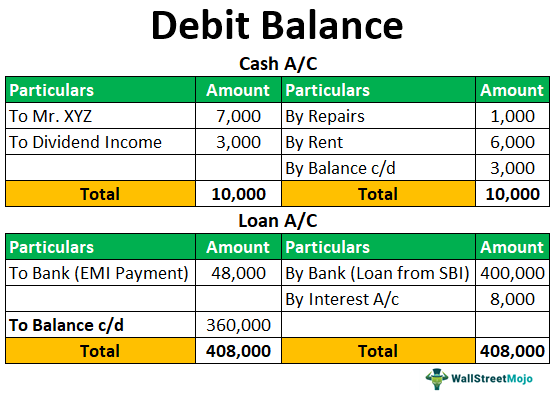

To understand in a better way, we can consider the following illustration,

Cash A/c

| Particulars | Amount | Particulars | Amount |

|---|---|---|---|

| To Mr. XYZ | 7,000 | By Repairs | 1,000 |

| To Dividend Income | 3,000 | By Rent | 6,000 |

| By Balance c/d | 3,000 | ||

| Total | 10,000 | Total | 10,000 |

Here we can see that the debit total is more than the credit total, i.e., the inflow of cash is more than the outflow; therefore, the cash account gives a debit balance of 3,000.

Loan A/c

| Particulars | Amount | Particulars | Amount |

|---|---|---|---|

| To Bank (EMI Payment) | 48,000 | By Bank (Loan from SBI) | 400,000 |

| By Interest A/C | 8,000 | ||

| To Balance c/d | 360,000 | ||

| Total | 408,000 | Total | 408,000 |

Conclusion

Here we can understand that after repayment of the installment of the loan, the credit total is higher than the debit total; therefore, the loan a/c gives a credit of Rs. 360,000.

From the above explanation, we can understand that these balances are commonly used terms in accounting. While reading and understanding financial statements, therefore, it is important to understand the term’s meaning, which can be concluded, i.e.,

if Debit total > Credit Total = Debit Balance and

if Credit total > Debit Total = Credit Balance.

Recommended Articles

This article has been a guide to what debit balance is and its definition. Here we discuss examples of debit balances along with their difference from a credit balance. You can learn more about financing from the following articles –