Part of our Accounts Payable & Receivable guide

Debit Note Meaning

A debit note is a confirmation document sent by a buyer for returning purchased goods or services to a seller. If all or a percentage of goods have defects, buyers send this memo. A note is also sent when the buyer is overcharged for the goods.

This document is crucial for business-to-business transactions. Sometimes sellers also send such a note stating the buyer’s debt obligations. Both the parties issue documents to rectify incorrect values in the invoice. Usually, debit notes are issued when goods are purchased on credit.

- A debit note is a document released by a buyer for returning goods bought on credit. Debit notes are also called debit memos.

- In addition, it is used for various other purposes like a rectification of a wrong invoice, change in order quantity, change in taxes, etc.

- The document becomes valid only upon acceptance.

- Notes sent by buyers contain crucial details—the reason for return, quantity, price, and the number of goods returned.

Explanation

A debit note is also known as a debit memo. So, buyers send debit memos to sellers if they return the goods or service. It is, therefore, an official, articulated form of a purchase return. Buyers inform the seller that they are returning the goods and mention their reasons. Further, when buyers receive debit memos, they approve them and then send back a credit note.

Alternatively, sellers also send debit memos to buyers—informing the buyer of pending debt obligations.

Now, let us understand the reasons for issuing debit memos. A buyer issues a debit memo to initiate purchase return for goods procured on credit when:

- The goods delivered by the supplier are not up to the mark—defective, damaged, or inappropriate in size, shape, or quantity;

- The supplier fails to deliver the goods or services on time;

- Goods or services are overbilled—calculation errors;

- Higher taxes are applied on goods or services;

- The buyer no longer wants to make the purchase.

A seller also issues a debit memo under the following circumstances:

- When seller requires adjustments in the invoice;

- When the seller changes (increases) the billing amount;

- When the buyer Increases the order quantity;

- To remind the buyer of their current debt obligations.

Debit Note Video

Features

To understand what exactly a debit note is, we will look at some of its most significant features:

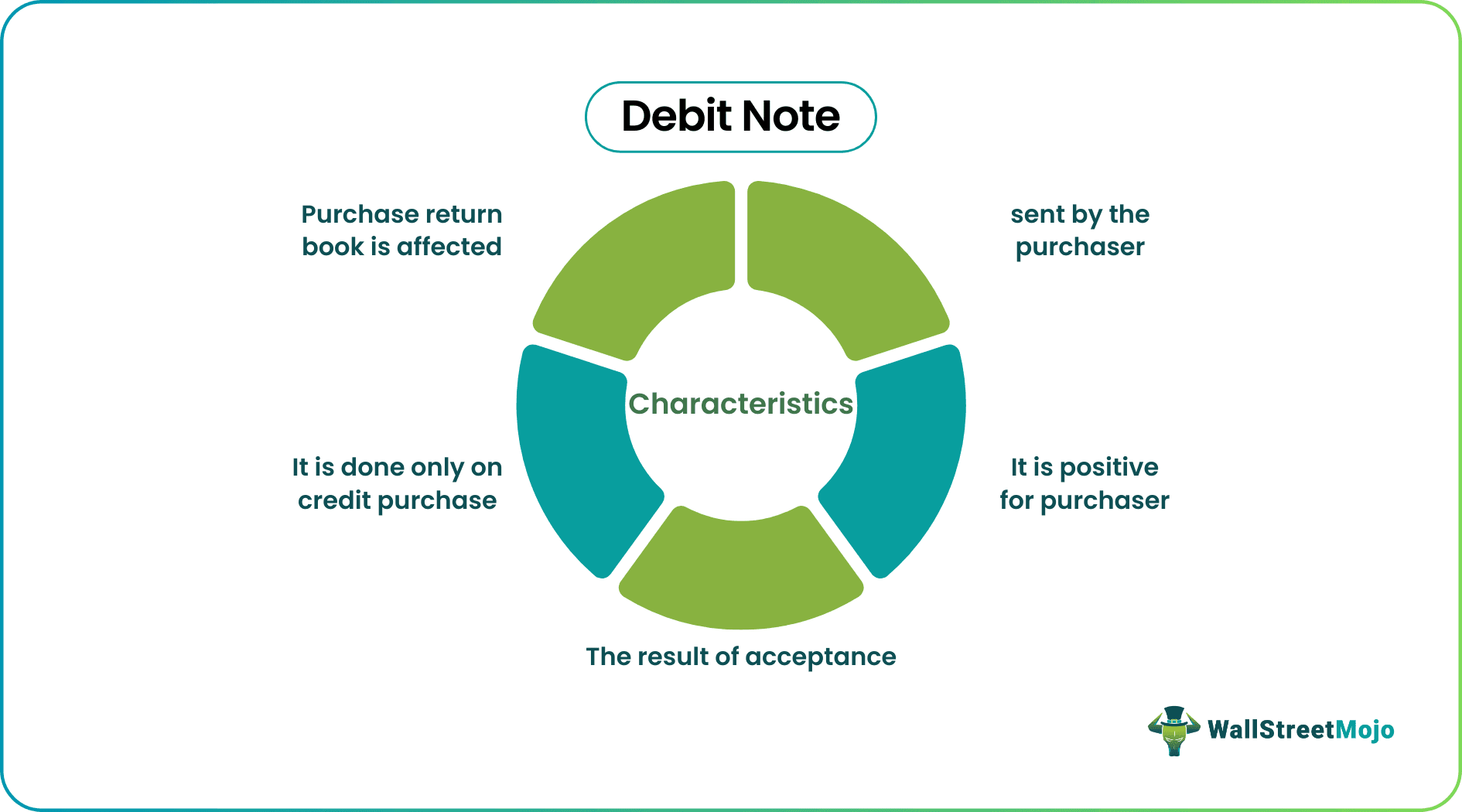

- Issued on Credit Purchase: When goods or services are purchased on credit, a debit memo accompanies.

- Issued by Buyer or Seller: Buyers send this document to a seller, listing out details of the purchase return. Vendors also issue this document when invoices contain mistakes.

- Requires Acceptance: The document becomes valid only when the sellers accept the debit memos—sellers make necessary changes in their books of accounts.

- States the reason: in the debit memo, the buyer clearly mentions the reason for returning the goods.

- Shown in Purchase Return Book: This note reduces the buyer’s credit purchase amount and increases the purchase return figures. In accounting entries, the purchases are debited, and purchase returns are credited.

- Reduces Buyer’s Debt Obligation: From the buyer’s perspective, the debit memo is a positive amount that will curtail their liability towards the seller.

Debit Note Format

A debit memo comprises the following details:

- Company name (Issuer);

- Issuer’s address, zip code, phone number, and web address;

- Date of creating the debit memo;

- Order number for which it is issued;

- Date of placing the order;

- Order terms and conditions;

- Customer Id—as stated in the invoice;

- Company name (Buyer);

- Buyer’s address, zip code, phone number, and email id;

- Name of contact person (Buyer);

- Invoice details—item name (goods or services), item description, the reason for debit, quantity, price, and total amount;

- Approval details— date, name and designation, and signature of the issuer’s representative.

Debit Note Accounting

Now, let us find out the accounting entries in the books of buyers and sellers. When a buyer purchases goods on credit and then returns them, the following entries are made:

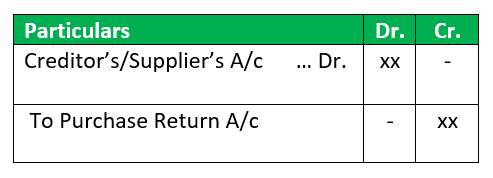

In the buyer’s books of accounts:

Earlier, the buyer had debited the Purchase A/c and credited the Supplier’s A/c. Therefore, upon return of some or all of the goods, the supplier will debit the Supplier’s A/c (reduction in the debt obligation) and credit the Purchase Return A/c.

The adjusting entry would be as follows:

When the goods are received at the seller’s end, their books of accounts show the following:

To understand the above entry, we need to have a look at the following adjusting entry:

As there is a reduction in the credit sales due to the return of sold goods, the Sales A/c is debited. Also, the Sales Return A/c is credited. Similarly, in the above accounting entry, the Sales Return A/c is debited, and the Debtors A/c is credited owing to a decrease in receivables for the seller.

Debit Note Example

Let us assume that MNC Ltd has bought goods worth $40,000 from S&S Traders. Upon delivery, MNC Ltd found out that 2% of the total goods purchased are defective. The company issues a debit memo stating the same. What would be the journal entry in MNC’s books of accounts?

Solution:

Let us start with the calculation of purchase return:

Purchase Return = 2% of Total Purchase Value

Purchase Return = 2% of $40000 = $800

Journal Entries:

In the books of MNC Ltd (buyer):

| Particulars | Dr. | Cr. |

| Purchase A/c …. Dr To S&S Traders A/c | 40000 – | – 40000 |

| Particulars | Dr. | Cr. |

| Purchase Return A/c …. Dr To Purchase A/c | 800 – | – 800 |

| S&S Traders A/c …. Dr To Purchase Return A/c | 800 – | – 800 |

In the books of S&S Traders (seller):

| Particulars | Dr. | Cr. |

| MNC Ltd A/c …. Dr To Sales A/c | 40000 – | – 40000 |

| Particulars | Dr. | Cr. |

| Sales A/c …. Dr To Sales Return A/c | 800 – | – 800 |

| Sales Return A/c …. Dr To MNC Ltd A/c | 800 – | – 800 |

Frequently Asked Questions (FAQs)

What are Debit Notes?

A debit memo is a document that a buyer issues to the seller in case of a purchase return. Alternatively, sellers send a memo to buyers when they want to rectify an understated invoice.

Are debit notes and invoices the same?

A debit note is a written declaration of a purchase return issued by the buyer and sent to the seller. In addition, the document mentions the reasons for returning. On the contrary, an invoice is an itemized bill issued by a seller and sent to a buyer—upon completion of a sales transaction.

When is a debit note issued?

A buyer releases a debit memo for return or cancellation of goods or services owing to:

• Delivery of defective, damaged, or wrong goods;

• Overbilling of goods or services;

• Excess taxes applied on goods or services;

• Non-delivery of goods or services on time;

• Supplier’s incompliance to the buyer’s terms and conditions.

A seller issues a memo for:

• Revising the billing amount;

• Notify the buyer’s present debt obligation;

• Change in the order quantity.

Recommended Articles

This article has been a guide to what is Debit Note and its Meaning. Here we explain debit note, its accounting entries, features, format, and examples. You can also learn about basic accounting from the articles below –