What Is Active Return?

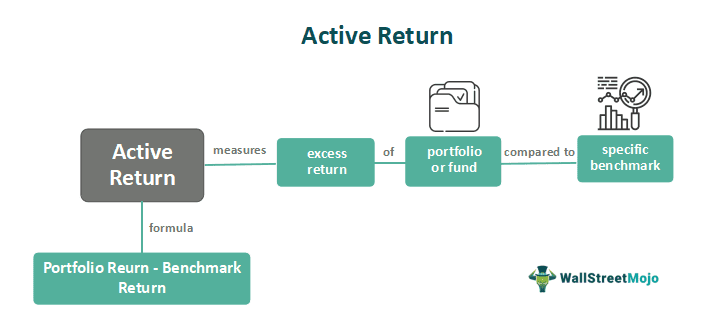

Active return is a financial metric that measures the excess return generated by an investment portfolio or fund compared to a specified benchmark. The purpose of active return is to evaluate the skill and performance of portfolio managers in generating returns above the market.

Active return helps investors assess whether the manager’s active investment strategies, such as stock selection, asset allocation, and market timing, add value to their investments. It is important because it provides insight into the effectiveness of a portfolio manager‘s approach. It reflects the portfolio manager’s ability to outperform the market and is calculated by subtracting the benchmark return from the portfolio’s actual return.

Key Takeaways

- Active return is a metric used to evaluate the performance of investment portfolios or funds relative to a specified benchmark. It provides insights into the portfolio manager’s ability to generate excess returns above the market.

- Positive return suggests that the portfolio manager has demonstrated skill in selecting investments, timing the market, or employing active investment strategies.

- If the portfolio consistently generates positive active returns, it may justify the higher fees associated with active management.

- Active return analysis helps investors make informed decisions about allocating their funds to specific portfolio managers.

Active Return Explained

Active return is a measure used to evaluate the performance of an investment portfolio or fund relative to a benchmark. It assesses the ability of a portfolio manager to generate returns above or below the market.

To understand active return, let us take a look at its components:

- Portfolio Return: It represents the actual return earned by the investment portfolio over a specific period. This return is based on the performance of the individual investments within the portfolio.

- Benchmark Return: It refers to the return generated by a designated benchmark index representing the market or a specific asset class. The benchmark serves as a reference point for evaluating the portfolio’s performance.

Formula

The formula for calculating active return is:

Active return = Portfolio Return – Benchmark Return

Here, the portfolio return represents the actual return earned by the investment portfolio or fund over a specific period, while the benchmark return is the return generated by a designated benchmark index during the same period.

To calculate it, subtracting the benchmark return from the portfolio return allows you to measure the excess or shortfall of returns compared to the benchmark. A positive return indicates that the portfolio has outperformed the benchmark, while a negative return suggests underperformance. The calculation can be adjusted to consider risk factors and other performance indicators, depending on investors’ and portfolio managers’ specific requirements and preferences.

Examples

Let us look at the examples to understand the concept better

Example #1

Consider a hypothetical scenario where a professional fund manager manages an investment portfolio. Over one year, the portfolio generates a return of 12%. Simultaneously, a relevant benchmark index, such as the S&P 500, generates a return of 10%.

To calculate the active return, subtract the benchmark return from the portfolio return:

Active Return = Portfolio Return – Benchmark Return Active Return

= 12% – 10% = 2%

In this instance, the active return is 2%. Thus, it indicates that the portfolio has outperformed the benchmark by two percentage points. This suggests that the fund manager’s investment decisions, such as stock selection or sector allocation, have added value and contributed to the excess return.

Example #2

As per an article by Morningstar, stock managers can improve active returns. It suggests that active large-cap managers who made numerous trades over a 10-year period did not benefit investors significantly. Also, the actual returns of these funds were nearly identical to what they would have been if no trades had been made at all. Furthermore, the fund’s performance was even worse after adjusting for risk. Their finding highlights that the frequent trading conducted by these managers did not contribute positively to investment returns and raises questions about the value they provide, particularly considering the associated fees.

Also, the context conveyed is that managers who promise to deliver such returns often charge substantial service fees. However, the article suggests that these fees may not be justified given the lack of substantial outperformance observed in the performance of these funds. Instead, the article proposes an alternative strategy to deliver better results.

Active Return vs Alpha

Let us have a look at the differences between active return and alpha:

| Metric | Active Return | Alpha |

|---|---|---|

| Definition | The excess return of a portfolio | Risk-adjusted outperformance |

| Calculation | Portfolio Return – Benchmark Return | Actual Return – (Risk-Free Rate + Beta * (Benchmark Return – Risk-Free Rate)) |

| Purpose | Evaluates the portfolio manager’s ability to outperform the benchmark | Measures manager’s skill in generating excess returns after adjusting for risk |

| Performance Assessment | Positive active return suggests potential skill in beating the benchmark | A positive alpha indicates the manager’s ability to outperform after adjusting for risk |

| Limitations | Doesn’t consider risk-adjusted performance | May not capture manager’s skill in all market conditions |

| Calculation Adjustments | Can be adjusted for risk factors or performance indicators | Incorporates systematic risk through beta calculation |

Active Return vs Active Risk

Let us look at the differences between active return and active risk:

| Metric | Active Return | Active Risk |

|---|---|---|

| Definition | The excess return of a portfolio | Volatility or risk of underperforming the benchmark |

| Calculation | Portfolio Return – Benchmark Return | The standard deviation of active returns |

| Importance | Indicates value added by active investment decisions | Assesses the level of risk taken to achieve active returns |

| Interpretation | Positive return indicates outperformance | Lower active risk suggests a more consistent performance |

| Performance Assessment | Higher return signifies better performance | Lower active risk suggests better risk management |

Active Return vs Excess Return

Let us look at the differences between active and excess return:

| Metric | Active Return | Excess Return |

|---|---|---|

| Definition | The excess return of a portfolio compared to a benchmark | The return earned above a specified benchmark or risk-free rate |

| Calculation | Portfolio Return – Benchmark Return | Portfolio Return – Benchmark Return or Risk-Free Rate |

| Purpose | Evaluates the portfolio manager’s ability to outperform the benchmark | Measures the additional return achieved beyond a reference point |

| Time Frame | Typically measured over a specific period | Can be measured over any time frame |

| Performance Assessment | Positive active return suggests potential skill in beating the benchmark | Positive excess return indicates superior performance |

| Risk Consideration | Active return doesn’t account for risk adjustments | Excess return can be risk-adjusted or compared to risk-free investments |

Frequently Asked Questions (FAQs)

1.How is active return different from passive return?

These terms differ in terms of investment strategies. Active represents the excess return achieved by actively managed portfolios that involve active investment decisions such as stock selection, market timing, and asset allocation. Passive return, on the other hand, is associated with passive investment strategies, typically tracking a benchmark index.

2.Can an active return be negative, and what does it indicate?

Yes, it can be negative, indicating underperformance compared to the benchmark. A negative return suggests that the investment portfolio or fund has failed to outperform the market. It may indicate that the active management decisions made by the portfolio manager, such as stock selection or market timing, have not been successful.

3.How can active return be adjusted for risk factors?

It can be adjusted for risk factors by considering risk-adjusted performance measures. One commonly used measure is alpha, which considers the portfolio’s systematic risk (beta). Alpha reflects the excess return the portfolio generates after adjusting for the risk associated with the benchmark.

Recommended Articles

This has been a guide to what is Active Return. Here, we explain its formula, compare it with alpha, active risk, and excess return, and examples. You can learn more about it from the following articles –