Part of our Investment Strategies guide

Asset Allocation Meaning

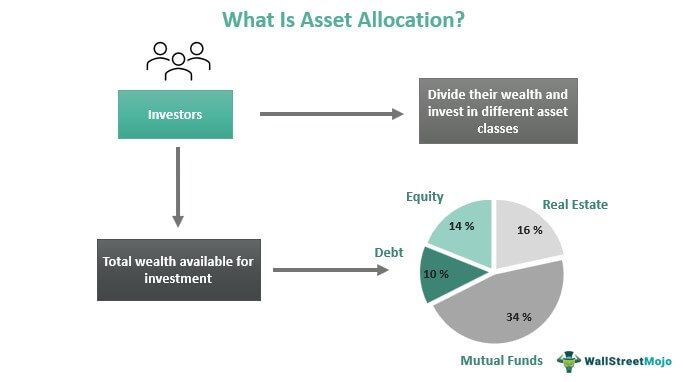

Asset allocation refers to dividing the total wealth of investors into various proportions and using them for making investments in different asset classes. This lets investors have diverse portfolios to maintain a balance between losses and profits. In addition, it helps minimize investment risks by covering a loss from one investment with the gains acquired from another.

Asset allocation applies to all asset classes, but the major ones include stocks, bonds, and cash. The distribution of wealth or the proportions allocated to different classes of assets depends on individual investors’ financial stability and ability to bear risks.

- Asset allocation is the distribution of wealth in various asset classes like debt, equity, mutual funds, real estate, etc., for achieving long-term financial goals.

- The allocation of resources for assets highly depends on the individuals’ risk appetite and the returns expected.

- It is the first step of portfolio management, which helps financial advisors determine the type and tenure of assets to invest in.

- Some widely used asset allocation models include 100% bond allocation, 100% stock allocation, income allocation, balanced allocation, growth allocation, etc.

How Does Asset Allocation Work?

Asset allocation, as the name suggests, deals with allocating different assets, helping investors divide their wealth and build diverse portfolios. Financial advisors recommend investors have diverse portfolios, given the market volatility. In addition, the strategy allows them to minimize risks. For example, if they incur a loss from the investment made in equity, the profits reaped from other investments would make it easier for them to deal with the loss. In short, even if losses occur, it reduces the effect on the traders.

The extent to which the wealth could be used for investment is an investor’s decision. Financial stability and an investor’s risk appetite are the two factors that drive the asset allocation decision.

One of the major decisions an investor needs to make is the distribution of wealth between stocks and bonds. It has been found that the stock or bond allocations show results over long periods. Vanguard studied data from 1926 to 2018 and observed the risks and returns associated with a 100% bond and 100% stock portfolios.

The investment management company figured out how the average annual return for the former was 5.3%, with 32.6% being the best return in 1982. Plus, it also mentioned the fall of 8.1% in 1969. Hence, it concluded how the bond portfolio took a long span to diminish in value. It observed a similar scenario for the 100% stock portfolio as well.

Models

Besides the above-mentioned basic asset allocation models, i.e., 100% stock portfolio and 100% bond portfolio, investors also have income, balanced, and growth portfolios to allocate their resources in. While the income model comprises allocating 70-100% of the wealth in bonds, a balanced portfolio involves 40-60% investment in stocks, with the growth portfolio requiring 70-100% wealth engagement in stocks.

No asset allocation is good or bad, right or wrong. Instead, investors’ financial condition, ability to deal with risks, expected return, and financial goals determine which model would suit them. For example, investors looking for long-term benefits must consider investing in and building their growth portfolio above other options.

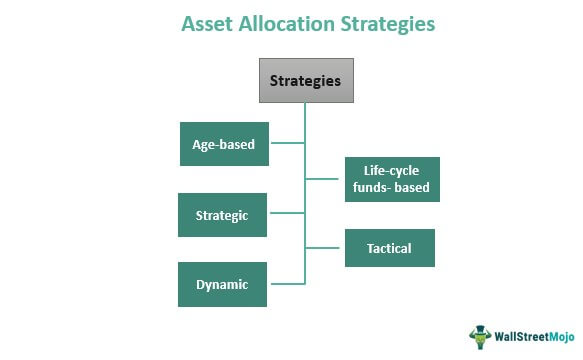

Strategies

When allocating assets, there are multiple strategies that financial advisors and investors adopt to ensure the investments made are fruitful. Some of the major asset allocation strategies include:

#1 – Age-Based

As the name implies, the age-based strategy considers the investors’ age. The financial advisors find out the portion of funds to invest in equity mutual funds by subtracting the investor’s age from 100. The rest of the wealth could be invested in other asset classes. For example, if one is 40-year-old, 80% of the fund is recommended for equity funds, while the rest is for different asset classes.

#2 – Lifecycle Funds

The next on the list is lifecycle funds. In this case, the advisors consider the investor’s age, their investment objectives, and risk appetite, like any other asset class investment. But especially, the investor’s age helps them determine the amount to invest in assets that would enable them to get the maximum returns on investment.

#3 – Strategic

Thirdly, financial advisors have a strategic asset allocation strategy to use. It is also known as constant-weight allocation, which revolves around the buy-and-hold policy. As per the financial market rule, the original asset allocation mix of 5% should not change. Thus, if one stock loses value, the investors are encouraged to buy more of them not to disturb the proportionate mix. Plus, if the value of those stocks increases in the future, selling them at a higher price would always reap profits.

#4 – Tactical

The fourth on the list is the tactical asset allocation. This strategy encourages short-term investment decisions. Users adopt and implement it where the strategic allocation of assets seems to fail. Hence, these are not into boosting long-term investments like the constant-weight allocation strategy.

#5 – Dynamic

Last but not least is the dynamic allocation of assets, which is one of the most widely used strategies nowadays. It allows investors to compare their highs and lows and accordingly decide where to increase the investment proportion and where to reduce it. As it makes various available options to switch to, investors can change their options to maximize profits and reduce losses.

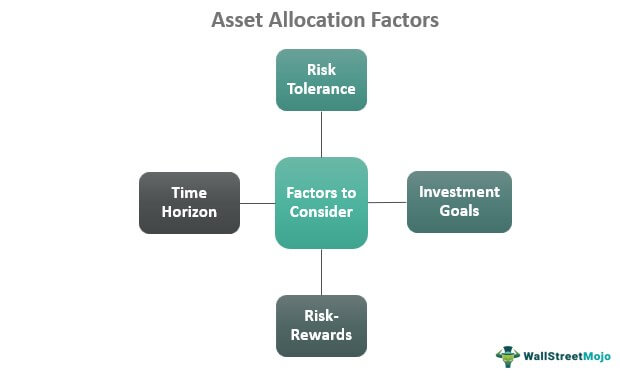

Factors

While allocating funds, multiple factors need consideration. Among all, the most important is the time horizon. Time plays a key role. Besides the age of the investors, there are other number factors that one must take into account. These include the number of months, years, or decades one desires to invest in an asset to achieve their financial goal. Though investors putting in money for the longer term are ready to take risks and invest in a volatile market, those with short-term goals avoid making riskier investments. In some cases, asset tracing may also be required to track the origin and movement of investments, especially when reallocating or reviewing portfolios.

As stated above, the investor’s risk tolerance ability is yet another factor that determines how the resources are allocated. Moreover, risks and rewards seem entangled when investors put in their wealth to allocate assets. While one of their investment might incur a loss, another has the chance of reaping huge profits. Hence, the returns remain balanced.

The last one that guides asset allocation is the financial or investment goals one aims to achieve. Every investor has a number in mind when it comes to expected returns. Sharing the expectations helps financial advisors allocate assets accordingly.

Example

Let us consider the following detailed asset allocation example to understand the concept well:

Stella, a 45-year-old corporate employee, plans to retire at 60 without any entitlement to pensions. She has a monthly income of $50,000 and multiple plans, including securing a significant monthly income for life after retirement. Given her plans, she connects with a financial advisor and decides to allocate assets.

Currently, she acquires wealth worth $2 million. The advisor recommends that she should opt for some risky assets, which would be fruitful after 15 years. The consultant ensures that the investor will get a sufficient amount to lead her retirement life. Thus, the concerned person recommends a few short-term equity investment options that would mature in the next five years to fulfill her travel plans.

Thus, she selects a few short-term to achieve her travel plans and adventure trips and some for long-term financial goals to secure her post-retirement phase.

Importance

Allocation of assets is the first step of portfolio management. However, until investors decide on the asset classes to invest in, the portfolio manager will not be able to suggest where to invest and for how long.

One of the best things about allocating the assets is that the investors can choose the asset classes to invest in as per their financial condition, expected returns, and ability to bear risks. As a result, they don’t feel trapped in the deal they invest in as they choose deals per their financial capabilities.

Next on the list is the interrelationship between asset allocation and diversification. The diverse portfolio keeps the investors balanced. When an investor distributes its wealth for investing in different asset classes, the gain from one deal helps cover the loss incurred from another. Thus, the distribution helps keep a balance between profits and losses for investors. As a result, they can play safe with asset allocation.

Frequently Asked Questions (FAQs)

What is asset allocation in investing?

Asset allocation in investing deals with the distribution of the total wealth of the investors into investing in different asset classes. These asset classes include stocks, bonds, real estate currencies, derivatives, fixed income, currencies, cryptocurrencies, cash, etc.

What is constant-weight allocation?

It is another name for strategic allocation of assets that runs on the buy-and-hold-policy. In this case, if one stock loses value, the investors are encouraged to buy more of them so that the original 5% mix does not get disturbed. Moreover, if the value of those stock increase in the future, selling them would be fruitful.

What are asset allocation funds?

It is defined as the funds allocated to fixed income security and equities based on the financial goal of investors. In the case of mutual funds, there is a target amount to be invested in the fixed income assets and equities.

Recommended Articles

This is a guide to what is Asset Allocation and its meaning. Here, we explain its mechanism along with the models, strategies, factors, and examples. You can learn more from the following articles –